Weekly Insight 20/01

US

US

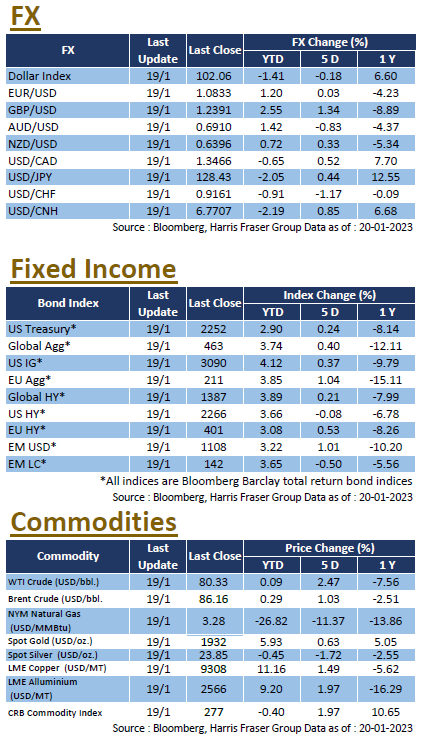

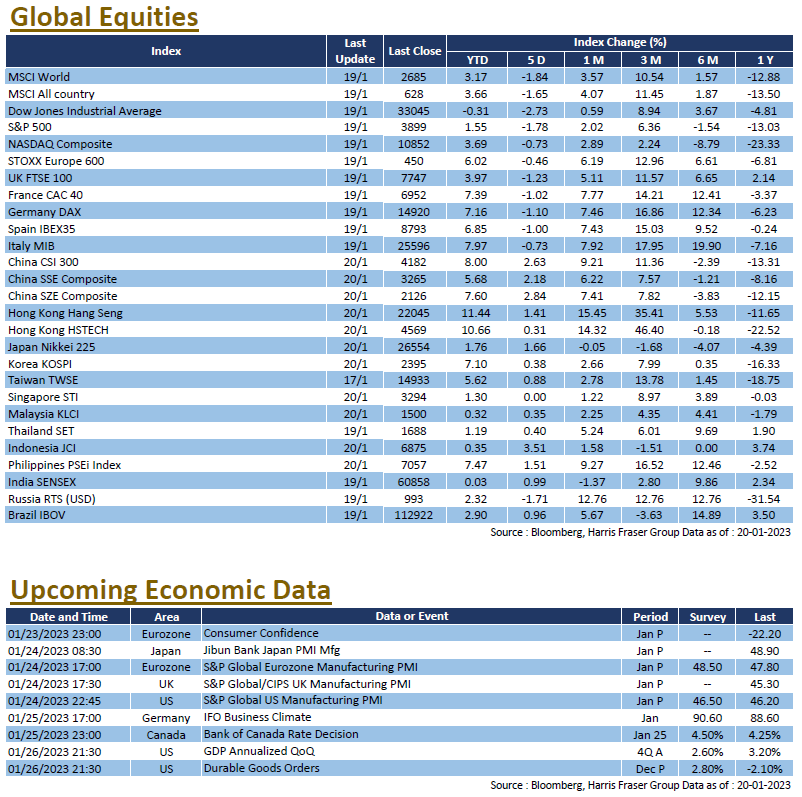

The US markets slipped as concerns over the economy reignited, over the past 5 days ending Thursday, the 3 major equity indices were down 0.73-2.73%. Fed officials continued to convey the message that inflation remains the top priority of the Fed, Fed Vice Chair Lael Brainard stated that inflation remains high despite the recent easing, such that rates would stay restrictive to ensure inflation returns to the longer term target of 2%. New York Fed President John Williams said the Fed has more work to do to bring down inflation, while Boston Fed President Susan Collins suggests that rate should go above 5% and stay at the level for some time. At the time of writing, the 2Y treasury yields were hovering around 4.15%, while 10Y treasuries are trading around the 3.4% level.

On economic data, PPI data came in lower than market expected, with the headline PPI falling 0.5% MoM in December. Industrial production and core retail sales figures also recorded MoM contractions, possibly suggesting a slowdown in the economy. However, the labour market remained tight, with initial and continuing claims coming in lower than market expected. In other news, the US debt limit fiasco continued, the debt limit was reached on Thursday, and the Treasury Department resorted to alternative sources of funds to avoid running out of cash. Next week, the US will be releasing more economic data, including the Markit manufacturing and services PMIs for January, durable goods orders for December, personal income in December, PCE data for Q4, as well as the revised GDP figures for 2022 Q4. The usual labour market data of initial and continuing jobless claims will also be released.

Europe

Europe

European equities fell on Thursday, bringing the UK, French, and German indices to a 0.34-0.92% loss over the past 5 days ending Thursday. The ECB released the minutes for the December meeting, which showed that many officials preferred a 75 bps hike. Members also projected that inflation has become more persistent, and expect core inflation to edge higher in 2023. ECB President Christine Lagarde said inflation is too high, and the ECB will continue to ensure inflation returns to 2%. The message is also echoed by Bank of France President Francois Villeroy de Galhau and Dutch Central Bank President Klaas Knot, who expect more than a single 50 bps hike this year. On the economy, German ZEW economic sentiment surged to 16.9 in January, which is a lot better than the expected -15.0 and December’s -23.3. UK CPI in December was 10.5%, in line with market expectations. Next week, both the Eurozone and the UK will release the January PMI figures, the Eurozone will release the consumer confidence index for January, and Germany will release the IFO business climate index for January.

China

China

The Chinese equity market continued to perform, the CSI 300 index posted a 2.63% over the week ahead of the long New Year holidays, the Hang Seng index also gained 1.41% over the period. Fixed asset investment, industrial production, and retail sales all came in better than market expected, China released their Q4 GDP, which was 2.9% YoY, much better than the expected 1.8%. The big turnaround in the policy lifted market expectations, with most provinces targeting an economic growth of at least 5% this year. On the other hand, the National Statistics Bureau reported that the population recorded the first drop since 1961, which could spell uncertainty for the future of the property market. US Treasury Secretary Janet Yellen met China Vice Premier Liu He in Zurich, pledging to avoid further worsening in Sino-US relations, it was also reported that Yellen will visit China at a later date. Next week, the China market enters a weeklong New Year holiday, no new economic data will be released, and markets will likely pay attention to travel and consumption related data after the holidays.