Weekly Insight February 26

US

US

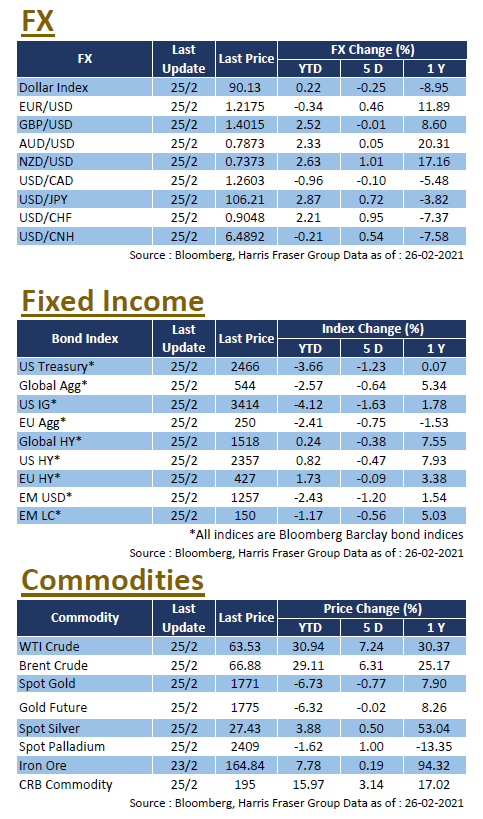

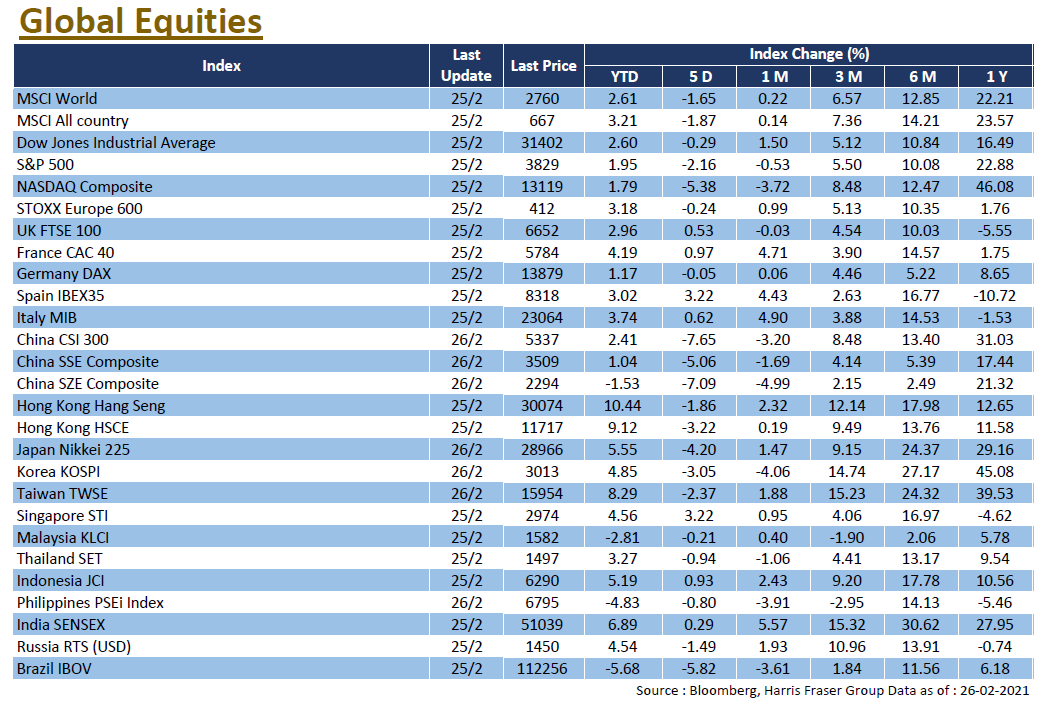

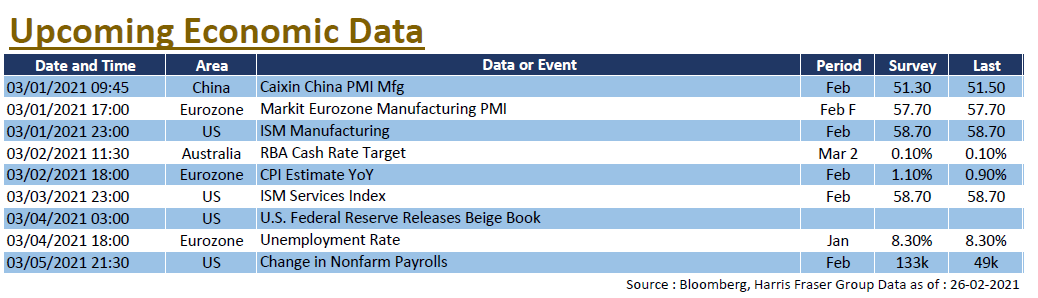

Long dated US bonds saw a heavy sell-off, with the US 10-year bond yield rising above 1.61% during the day. The market is worried about the possibility of an overheated economy and a sharp rise in inflation, which could possibly lead to the Fed tightening. US stocks fell sharply, with pressure on high valuation technology stocks, the NASDAQ index fell 5.38% over the past 5 days ending Thursday, while the S&P 500 and the Dow fell 2.16% and 0.29% respectively over the same period. US Federal Reserve Chairman Jerome Powell said there was no need to worry about inflation and the economy overheating, reiterating that the current economy still needs monetary easing. Other Fed officials also said publicly that the rise in US bond yields was a sign of market optimism about the economic outlook, stressing that there is no plan to tighten monetary policy at the moment. On the economic front, US 2020 Q4 GDP was revised to a 4.1% growth YoY, slightly below market expectations of 4.2%, while the core personal consumption expenditure (PCE) price index rose by 1.4% QoQ over the same period, in line with expectations. Next week, the ISM manufacturing and services indexes, employment data, and the latest Fed Beige Book will be released.

Europe

Europe

Against the backdrop of a correction in global equities, European equities fared better, with the UK and French equities gaining 0.53% and 0.57% over the past 5 days ending Thursday, while German equities edged down 0.05% over the same period. In view of the recent rise in yields on long-term government bonds, ECB President Christine Lagarde said the authorities are closely monitoring the trend in interest rates to determine whether the current financial environment is appropriate for the economy in the face of the epidemic. Bank of France Governor Mr François Villeroy de Galhau, also a member of the ECB Governing Council, said that the Eurozone economy faces no risk of overheating nor of rising inflation. Next week, the Eurozone will announce the unemployment rate for January and the Consumer Price Index (CPI) for February, which is expected to accelerate to 1.1% YoY.

China

China

The rise in US long end bond yields triggered a market correction in global equities. Mainland China also tightened up market capital, which saw net withdrawals for the third consecutive week, putting pressure on Hong Kong and Chinese stocks. The CSI 300 Index fell 7.65% over the week, whilst the Hang Seng Index fell over 5%. Emerging market currencies and equity markets came under pressure as there are concerns over rising US bond yields leading to capital outflows from emerging markets, with the USD/CNH briefly touching the 6.5 level. The People's Bank of China conducted a RMB20 billion 7-day reverse repo operation on Friday, but the market still recorded a net withdrawal of RMB20 billion for the week. Next week, China will release the Caixin Manufacturing and Services Purchasing Managers' Index for February. The market will be watching the Two Sessions closely, which is scheduled for 5 March.