Weekly Insight 10/03

US

US

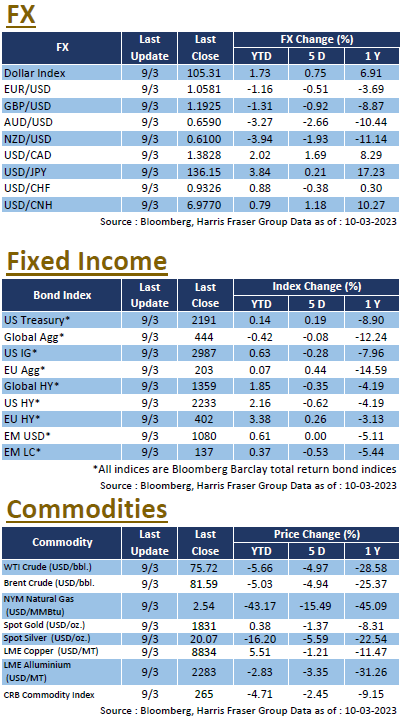

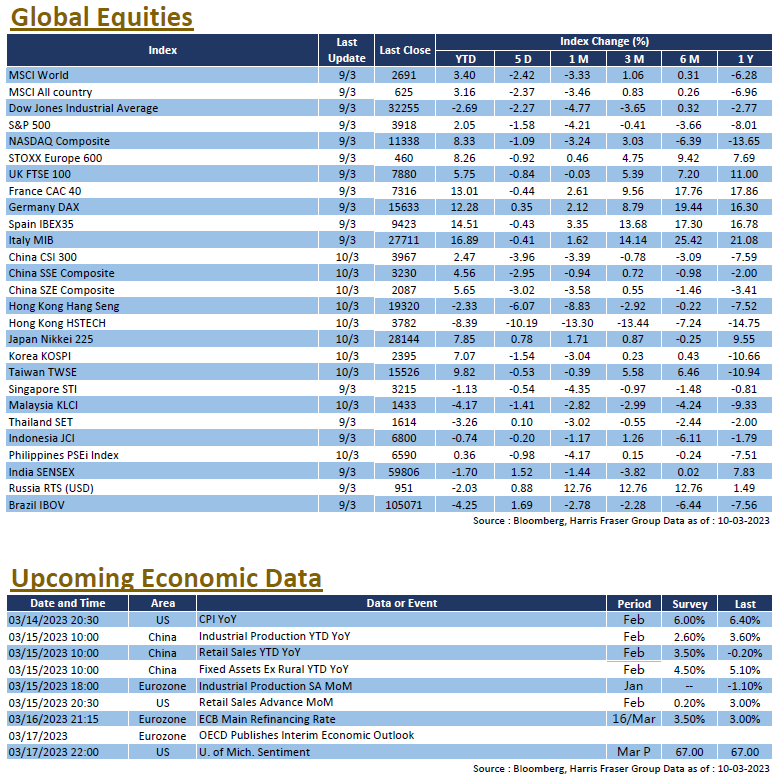

Rate hike jitters continued to affect market sentiment, anticipation of further monetary tightening ahead pressured markets, with the 3 major equity indices losing 1.09-2.27% over the past 5 days ending Thursday. US Fed President Jerome Powell testified in front of Congress during the week, suggesting that the Fed sees higher interest rates for longer than previously thought. Markets reacted to the comment, according to interest rate futures, markets are now pricing in a higher probability for a 50 bps hike in the March FOMC meeting, and raised terminal rate expectations for the year to 5.625%. President Joe Biden presented the 6.8 trillion Budget proposal, which included more taxes, aiming to reduce government deficit by 3 trillion over the coming years. The administration also expects inflation to fall to 4.3% by year end, and unemployment to hit 4.3%, GDP growth is also expected to slow to 0.6% YoY for the year.

As for the economy, ADP nonfarm employment was 242K in February, higher than both market expectations and the January figure. On the other hand, Challenger reports showed that job cuts grew by 410.1% YoY in February, initial and continuing jobless claims also came in higher than market expected, initial jobless claims in particular were at the highest level since last December, which could be a sign that the labour market is easing. Next week, the US will be publishing more economic data, including the February data on the all-important CPI, leading index, NFIB business optimism, as well as the University of Michigan Sentiment index for March. Sectorial data on retail sales, industrial production, and housing starts will also be published alongside the regular labour market data on initial and continuing jobless claims.

Europe

Europe

Contrary to the US markets, European equities had mixed performance over the week, the UK FTSE fell 0.81% over the past 5 days ending Thursday, while the French CAC and German DAX gained 0.43-1.99% over the same period. The Dutch government followed the US on China restrictions, announcing export controls on advanced microchip technology, which includes ASML made machines, Sino-European relations will remain a market focus. As for economic data, the final Eurozone GDP figures for Q4 2022 were downward revised to 0.0% QoQ from the earlier 0.1% growth, while Eurozone retail sales data in January contracted 2.3% YoY, which missed market expectations of a 1.8% fall. German factory orders grew 1.0% in January, higher than the expected 0.9% contraction; industrial production grew at 3.5% MoM, which also beat market estimates. Next week is a relatively quiet week on European data, with the only notable release on European industrial production data in January. Eyes will be on the ECB monetary meeting, with a 50 bps hike largely in the books, the OECD is also expected to publish the Interim Economic Outlook.

China

China

Hong Kong and China markets continued the weak form since the end of January, partially due to the weaker sentiment. Over the week, the CSI 300 index is down 3.96%, while the Hang Seng Index is 6.07% lower. The Two Sessions were held over the week, Premier Li Keqiang mentioned in his government work report that China’s GDP is expected to grow by around 5% this year. On the other hand, President Xi was unanimously elected President and Chairman of the Central Military Commission, and Han Zheng returned to the center stage as the new Vice-President. As for the economy, exports fell 6.8% YoY in February, which was better than the expected 9.4% fall. Inflation data on the other hand came in lower than expected, February CPI in particular was 1.0% YoY, much lower than the market expected 1.9%; the PPI in February fell 1.4% YoY, also lower than both market expectations and the January figure. Next week, China will be publishing the February data on industrial production, retail sales, as well as fixed assets and property investments.