Weekly Insight April 23

US

US

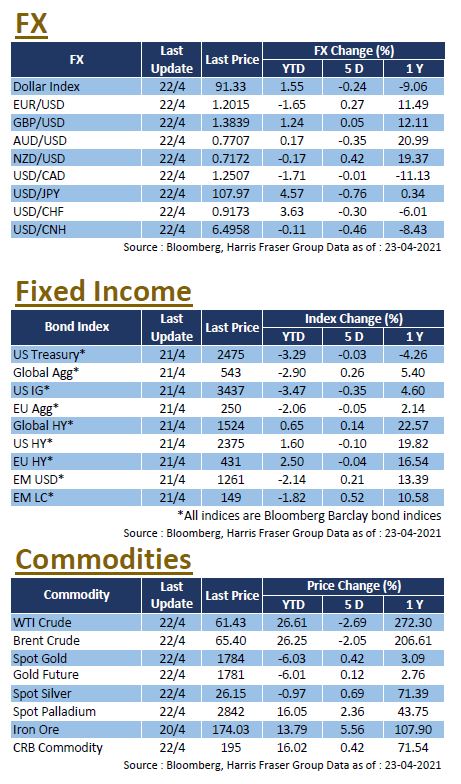

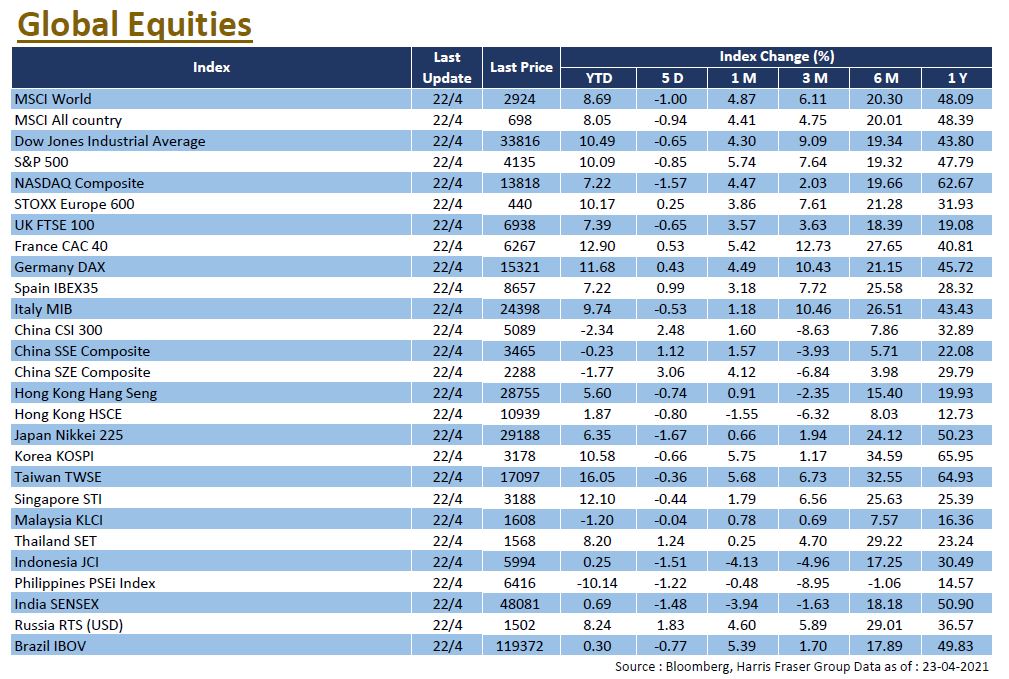

The US stock market came under pressure at its all-time high as the epidemic worsened around the world, coupled with news of a proposed hike in capital gains tax, the three major equity indices fell between 0.65% and 1.57% over the past five days ending Thursday. The World Health Organisation (WHO) said the number of daily new cases is on the rise in all regions except Europe, and India in particular has set a new global record of more than 310,000 new cases per day, while places such as Tokyo may also enter a state of emergency. The US stock market reacted negatively to reports that Biden would raise capital gains tax to a maximum of 43.4% on the wealthy, sparking fears that participants might sell assets in advance. Meanwhile, in response to Biden's $2.3 trillion infrastructure plan, Senate Republicans proposed a $568 billion alternative on Thursday that focused on more traditional infrastructure projects and omitted the Democratic proposal for a hike in corporate profits tax.

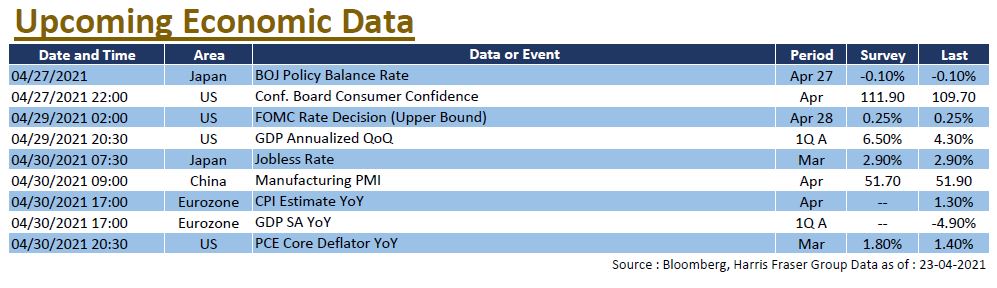

Recent economic figures and corporate earnings were positive, initial jobless claims in the US fell to a record low since the start of the epidemic. As of Thursday, over 75% of reporting S&P 500 index constituents beat market expectations. It is also worth noting that the Bitcoin has plunged recently, falling below the US$48,000 level at the time of writing. Next week, the US Fed will hold the interest rate meeting, and the preliminary GDP for 2021 Q1 will be released. The market is expecting an annualised growth of 6.5% QoQ.

Europe

Europe

European markets fell in line with global equity markets, the UK, German, and French indexes were down between 0.31% and 1.16% over the past 5 days ending Thursday. The ECB kept interest rates unchanged and pledged to maintain its 1.85 trillion euro PEPP unchanged at least until March 2022. ECB President Christine Lagarde said that the bank would not keep pace with the Fed, and the central bank is not considering phasing out the PEPP at this time. Eurozone economic data improved, with the Eurozone consumer confidence indicator rising to -8.1 in April, beating market expectations. Next week, Europe will release the preliminary 2021 Q1 GDP and the April inflation data.

China

China

Chinese equities performed relatively well this week, with the CSI 300 Index rising 3.41% for the week. Hong Kong markets also rebounded on Friday, the Hang Seng Index ended the week in green, logging a gain of 0.38%. It was reported that the People's Bank of China (PBoC) was considering a third-party buyout of Huarong's $100 billion assets, bringing clarity to the "Huarong debacle" that had plagued the Chinese offshore bond markets, meanwhile Huarong International also announced a turnaround in its first quarter results. Separately, Anta Sports and Meituan, two companies that announced share placements earlier, also rebounded for the second consecutive day, easing market concerns. Next week, China will release official manufacturing and non-manufacturing PMI data for April.