Weekly Insight October 14

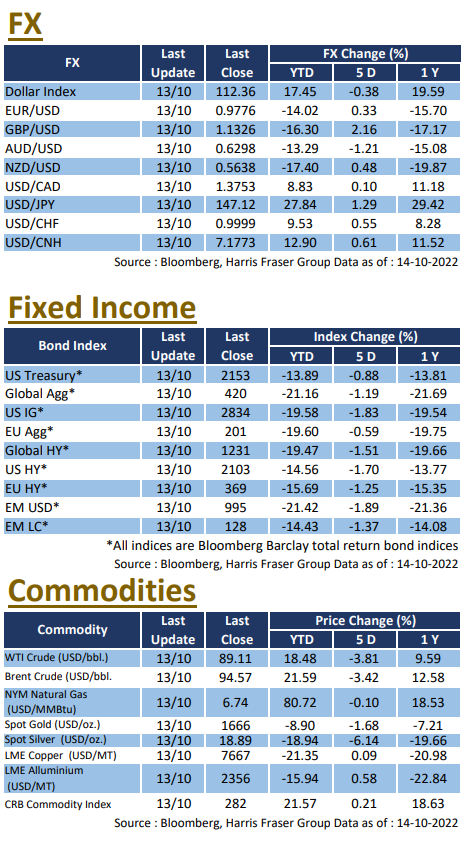

Despite latest inflation data coming in higher than expected, US equities still rebounded on Thursday, driven by technicals. Over the past 5 days ending Thursday, the Dow was up 0.37%, while the S&P 500 and NASDAQ were down 1.99% and 3.83% respectively. The US Fed release their September interest rate meeting notes on Wednesday, it showed that officials still considered inflation to be too high. There are plans to hike rates further, and the rates will stay at the restrictive level until inflation does return to 2%, the noted also indicated that members project the terminal rate to be around 4.6%. Cleveland Fed President Loretta Mester suggested that existing rate hikes have yet to have its impact on inflation, and more restrictive policy is needed to rein in inflation. Fed Governor Michelle Bowman echoed the generic view of Fed members, supporting more rate hikes in order to get inflation down. The communication from Fed strengthens the idea that a Fed pivot is unlikely in the short term.

As for economic, the most important CPI data in September figure was 8.2% YoY, which is higher than the expected 8.1%. The figure equates to a 0.4% growth MoM, which was higher than the market consensus of 0.2%. Stripping off the impacts of energy and food costs, the core CPI in September also stayed strong at 6.6% YoY, which is higher than both market expectations and the previous value. Inflationary pressures seems to remain elevated. Labour markets data however showed slight easing, as both initial and continuing jobless claims are higher than market expectations and their previous values. It remains to be seen if this trend would continue. Next week, US will release its September figures for industrial production, building permits, as well as existing home sales, alongside the Fed Beige Book. The earnings season will also be in focus, with big names including Johnson & Johnson and Tesla expected to provide further guidance.

European equities slid as hopes of a central bank pivot were dashed, although markets rebounded on Thursday in line with global markets. Over the past 5 days ending Thursday, the UK, French, and German equity indices were down 0.96-2.1%. After the earlier rout in the gilts market, the Bank of England Governor Andrew Bailey warned markets that the Bank’s bond buying is only a temporary measure, and further purchases will end on Friday, news shook both the bond and currency markets in the UK. ECB President Christine Lagarde reiterated that rate hikes will continue, and the Council is looking at quantitative tightening, she also argued that the Euro Area is not in a recession right now. As for the economy, the Sentix investor confidence for October worsened to -38.3, lower than both the forecasted -34.7 and previous value of -31.8, it is also the lowest figure since July 2020. The UK GDP on the other hand fell 0.3% QoQ, which is slightly worse than the expected 0.2% fall. Next week, the UK will release its CPI and retail sales data for September, and Germany will be releasing the ZEW Economic Sentiment Index for October.

China

China

China A-Share markets resumed trading after the National Day holidays, but trading activity was thin in the eve of the 20th National Congress of the Chinese Communist Party. China A-Shares and Hong Kong equities diverged in performance, the CSI 300 index gained 0.99% over the week, while Hang Seng Index fell 6.5%, hitting a new low since the start of the year on Thursday. Chinese authorities had been mentioning Dynamic Zero again before the National Congress takes place, policy pivot on COVID is seemingly less likely in the short term. As for economic data, Chinese Total Aggregate Financing in September was 3,530 billion, far exceeding expectations of 2,725 billion and August’s 2,430 billion. Caixin Services PMI for September on the other hand returned to the contraction zone at 49.3, far below forecasts of 54.5 and the previous value of 55.0. Next week, China will be releasing its Q3 GDP data, as well as September data on exports, retail sales, industrial production, and fixed asset investment. The 20th National Congress will also be held over the week, investors will be looking for further policy guidance from the conference.