Weekly Insight 03/03

US

US

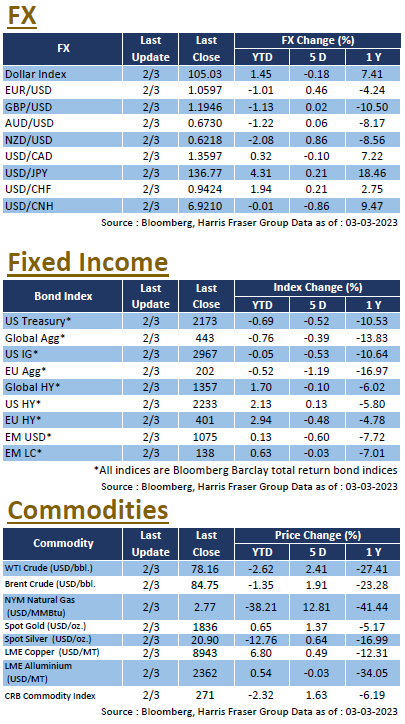

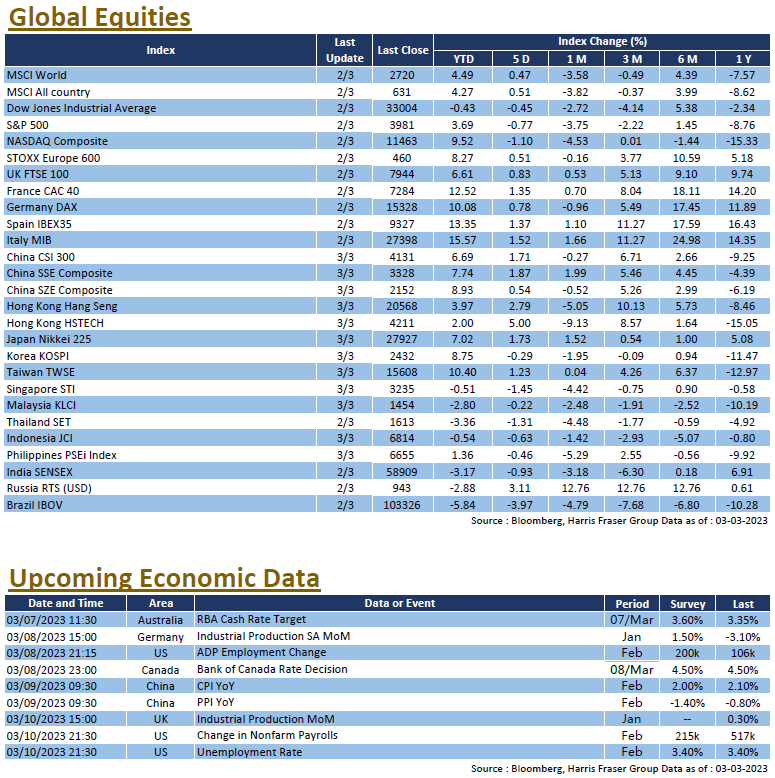

Positive economic data drove the expectations of further monetary tightening higher throughout the week, hitting market sentiment and compressed valuations. Over the past 5 days ending Thursday, the 3 major equity indices lost 0.45-1.1%. In response to the hotter data, several Fed speakers including Boston Fed President Susan Collins and Governor Christopher Waller suggested that more tightening could be needed to get inflation under control, Atlanta Fed President Raphael Bostic on the other hand agreed that data suggests that the Fed Fund Rates could be required to go higher, but he still prefers a 25 bps hike in the next FOMC meeting. The yield curve across the board shifted higher, even 30Y treasury yields breached the 4% mark during the week.

As for the economy, ISM manufacturing PMI for February came in at 47.7, which was slightly lower than market expected, Conference Board consumer confidence index for February was 102.9, which was significantly lower than the market expected 108.5 and January’s 106. Core durable goods orders in January grew 0.7% MoM, which was higher than both the market expected 0.1% and December’s 0.4% fall. The labour market on the other hand remains tight, as both the latest initial and continuing claims came in lower than market estimates and the previous figure, potentially intensifying core inflationary pressures. Next week, more US labour market data will be released. Apart from the usual initial and continuing jobless claims, the February data on ADP employment change, nonfarm payrolls, as well as the unemployment rate will be released.

Europe

Europe

European equities had a mixed week, over the past 5 days ending Thursday, the UK FTSE edged 0.46% higher, while the French CAC and German DAX lost 0.45% and 0.96%. The ECB released their minutes of the February meeting, which showed that members aren’t too concerned about overly restrictive monetary policy at the moment, and the next point of contention will be to whether hike 25 or 50 bps in the May meeting. As for the economy, inflation data was the center of focus in the week, where the Eurozone CPI was 8.5% YoY in February. While the figure was slightly lower than January’s 8.6%, it is higher than the market expected 8.2%, and equates to a 0.8% gain MoM. The core CPI raised further eyebrows with the 5.6% YoY figure, which is yet another new record high. Next week, the Europe will release their final GDP figures for Q4 2022 and retail sales data in January, German will release their factory orders and industrial production data for January, and the UK will release their industrial production data for January.

China

China

Hong Kong and China equities posted a slight rebound this week, market sentiment were lukewarm as the National People’s Congress is just around the corner. Over the week, the CSI 300 index gained 1.71%, while the Hang Seng Index gained 2.79%. PBOC Governor Yi Gang suggested that the current interest rate is appropriate at the press conference, and sees less room to cut bank reserve requirements, while Deputy Governor Pang Gongsheng reiterated the notion that housing is for living not speculation, the PBOC emphasized that stability remains the primary goal of the Bank. As for the economy, all PMIs came in higher than market expected in February, with Caixin Manufacturing PMI in particular also returned to the expansion zone. Next week, China will be releasing their exports data for February, alongside the CPI and PPI data for February, they are also poised to release the latest aggregate financing and money supply M2 figures for February. The National People’s Congress will also commence on Sunday.