Weekly Insight Aug 7

US

US

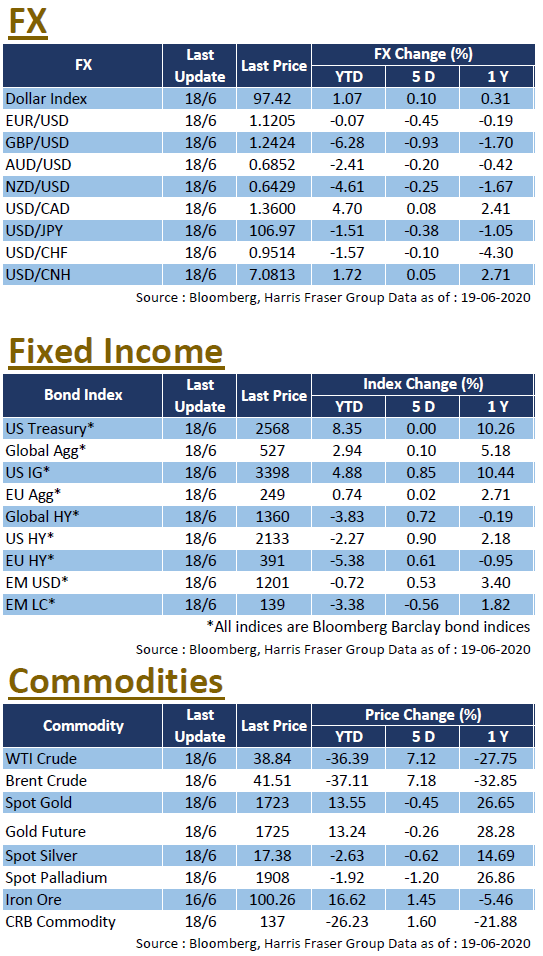

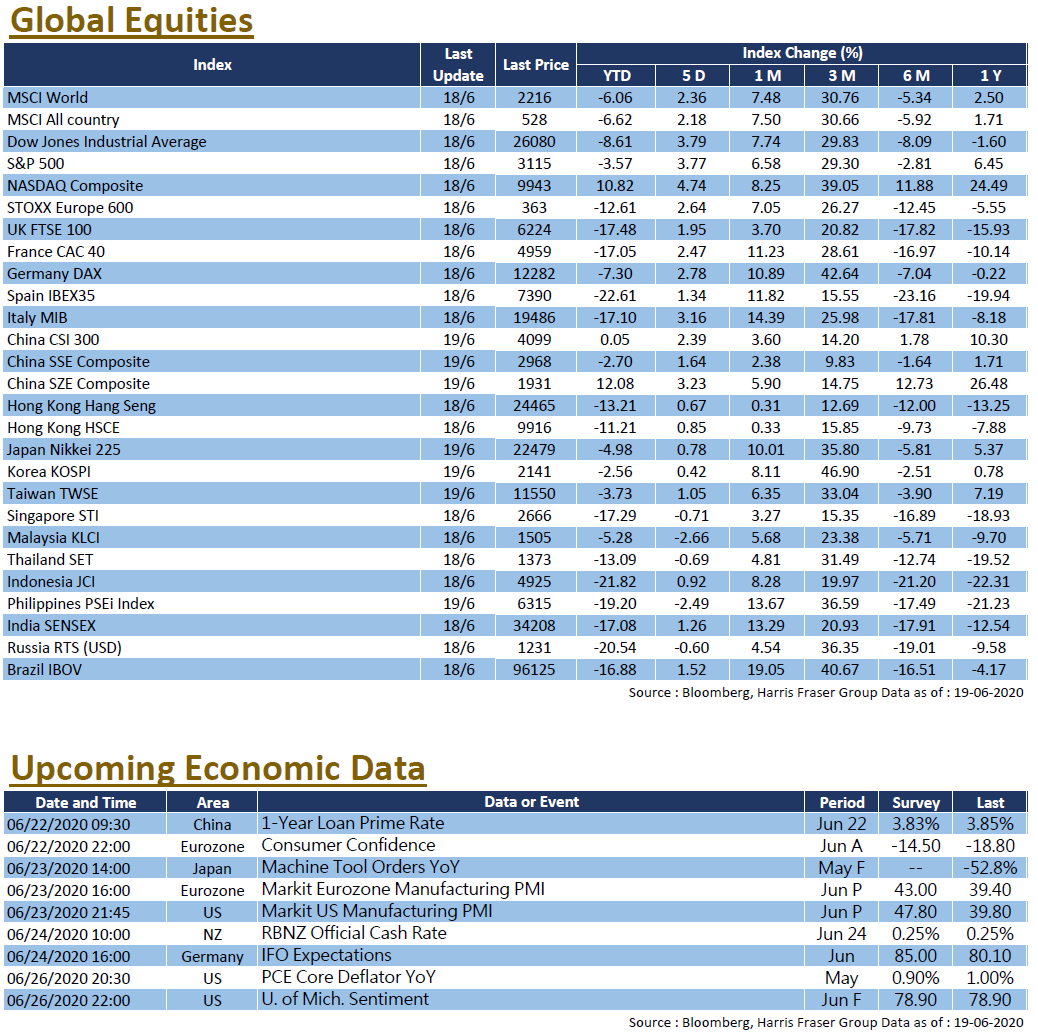

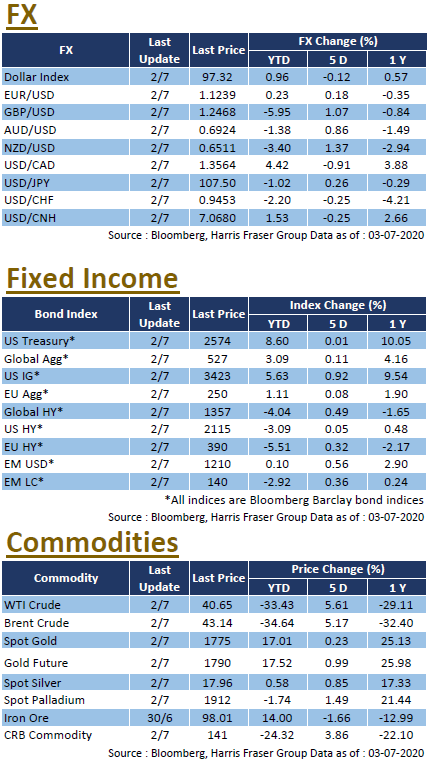

The latest earnings season in the US is coming to an end. Among the 440 S&P 500 companies that have reported, around 84% of them beat market expectations. Over the past trading 5 days ending Thursday, the Dow and the S&P 500 were in the green for 5 consecutive trading days, gaining 4.08% and 3.17% respectively over the period; the Nasdaq even rose for 7 consecutive trading days and hit a new record high. Although the US Republicans and Democrats are still divided over certain key issues in the new stimulus bill, the overall negotiations still made progress. Together with US ISM manufacturing index improving and beating market expectations, the stock markets rallied. US Fed Vice Chairman Richard Clarida said that the Congress stimulus bills will help the US economy rebound in the second half of the year. It is worth mentioning that the US dollar index stayed weak, hitting a low of 92.52 on Thursday, the lowest level since May 2018; the price of gold continued to rise. At the time of writing, the spot gold price crossed $2,070 per ounce, continuing to set new record highs. The United States will release data on CPI and retail sales next week.

Europe

Europe

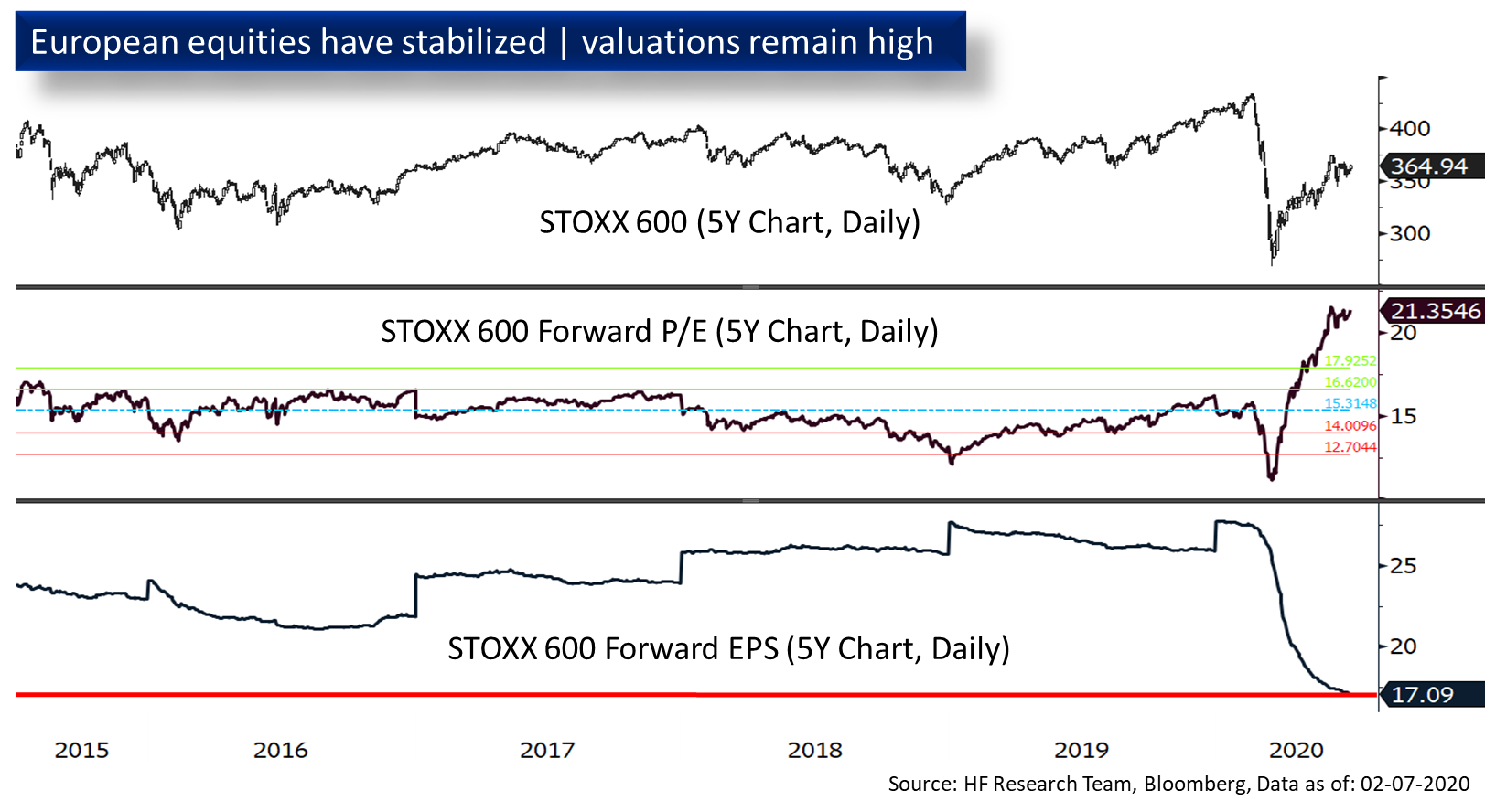

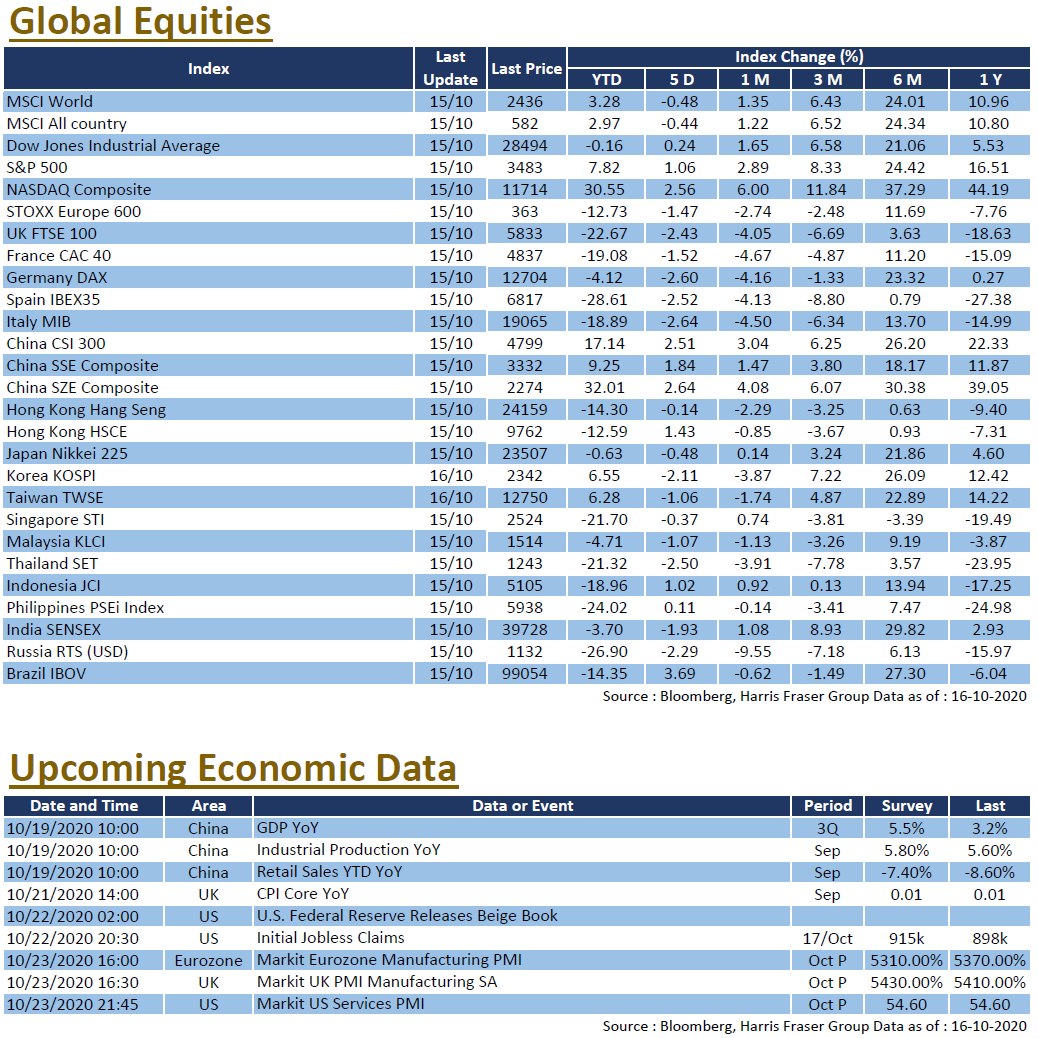

European equities followed the global markets and went up. The UK, French, and German equity indexes rose between 1.73% and 2.19% over the past 5 trading days ending Thursday. The latest quarterly earnings season in Europe is also coming to an end. Among the 342 STOXX 600 companies that have reported, about 63% beat market estimates, which is slightly lower than the 84% of the S&P 500. In particular, companies such as BMW recorded quarterly losses, while Commerzbank and Allianz also recorded steep falls in net profits. The Bank of England will hold the interest rate meeting next week, the market is looking for be any hints on possible interest rate cuts.

China

China

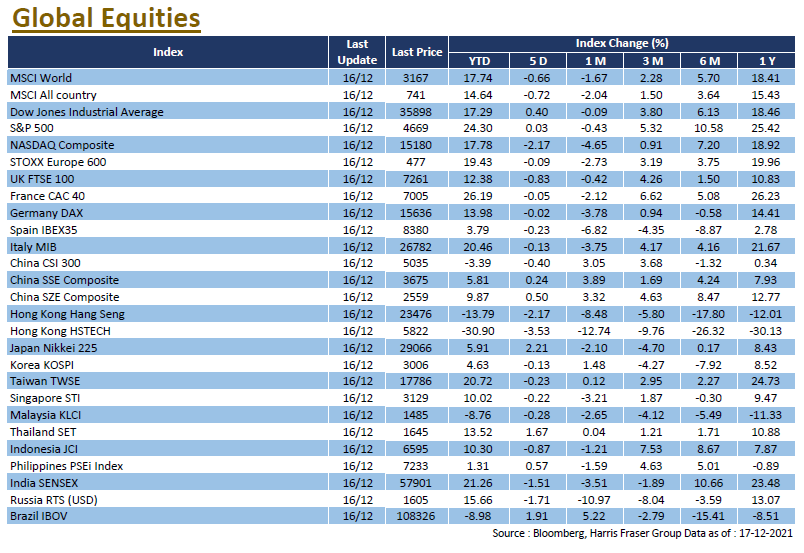

China and Hong Kong stock markets lagged behind Western markets. The CSI 300 Index only rose 0.27% over the week, while the Hang Seng Index fell 0.26%. US President Donald Trump signed an executive order prohibiting US companies and individuals from doing business with TikTok's parent company and WeChat. The news triggered market concerns over related sectors, relevant shares also saw sharp drops. China's export data in July improved, rising by 7.2% YoY in dollar terms, while market expected a decline of 0.6%. Next week, China will announce July data on fixed investment, industrial production, retail, and CPI.

US

US Europe

Europe China

China