Into the last month of the year, emerging markets edged lower in line with global markets. Over the month of December, the FTSE ASEAN 40 lost 0.30% over the month, ending the year with a 2.36% gain, while the MSCI emerging markets index lost 1.64% in December, ending 2022 with a 22.37% loss, in line with the losses in the China market.

Given the global economic slowdown and chances of recession, there are multiple sources of headwinds for EM economies, including high inflation, weak currency, tight monetary and financing conditions, as well as weaker external demand. Furthermore, the weak balance sheets and the risks of inflation rules out strong fiscal stimuli, higher financing costs weakens investment sentiment, drawing capital away from EM economies, further impacting longer term economic growth. According to World Bank, EM economic growth is expected to decelerate to 2.7% in 2023, far lower than the long term average.

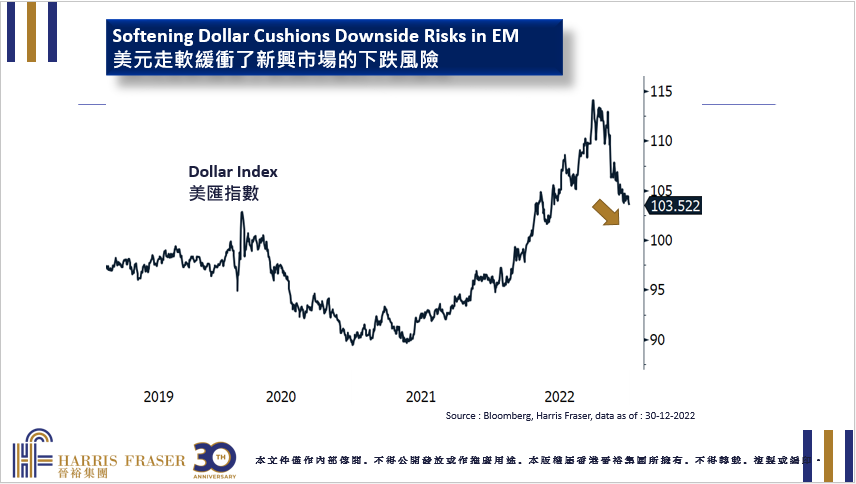

For ex-China EM economies, Latin America led by Brazil will likely experience higher volatility ahead as uncertainty mounts following Lula’s win, both politically and financially. Asian markets on the other hand would suffer due to the fall in external demand, but with China’s recovery and the reopening across the region, the renewed demand could possibly offset some impact on the economy. Emerging Europe would likely underperform, as there is still no signs of resolution on the Ukrainian conflict. All in all, while market is skewed to the downside, given that short term softness in the US Dollar is expected, this could possibly limit the risk in EM equities, one could consider a small allocation to Asian EM if opportunity arises.