Weekly Insight May 14

US

US

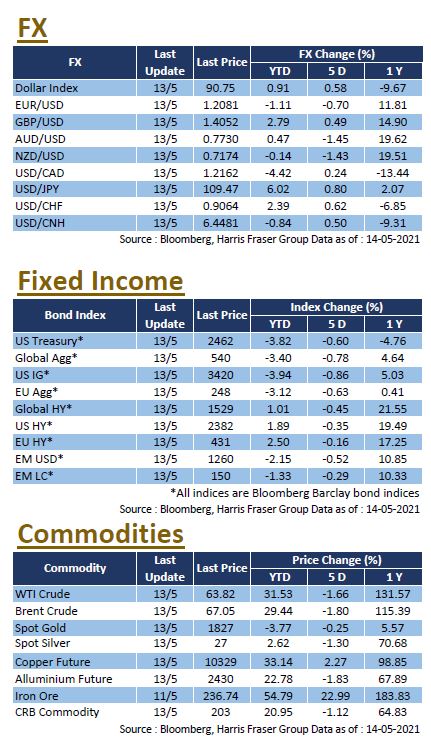

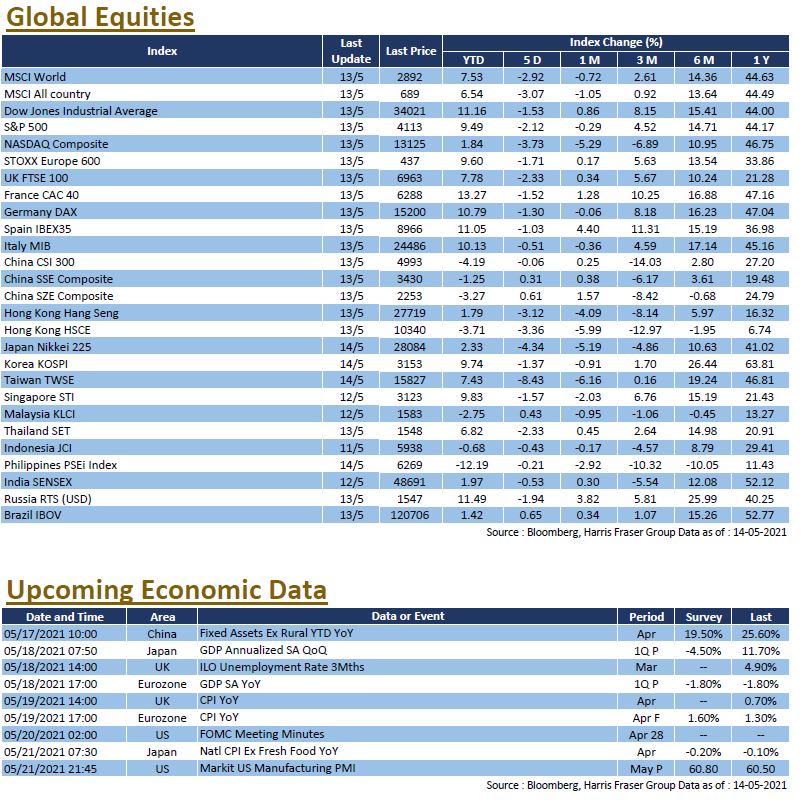

Rising global demand but a supply shortage has led to a surge in commodity prices, and data suggesting an acceleration in inflation has sparked fears of interest rate hikes. The US CPI rose by 4.2% YoY in April, well above market expectations of 3.6% and the previous value of 2.6%, which was also the largest increase in more than a decade; the US PPI also rose more than expected in April; coupled with the projected inflation in the next five years at its highest level since 2006, the headline figures triggered fears of inflation and interest rate hikes, leading to a sharp fall in technology stocks and a shift from growth to value stocks. Over the five past days ending Thursday, the NASDAQ was the worst performer, falling 3.73%, while the Dow and S&P 500 also fell 1.53% and 2.12% respectively over the same period. On the other hand, the latest initial jobless claims in the US hit a record low since the epidemic, several Fed officials believe the economic outlook is bright but risks remain, and are currently discussing whether it is too early to cut back on accommodative measures. Next week, the US will release the Markit Manufacturing PMI data for May and the Fed will also release the minutes of its April meeting.

Europe

Europe

European shares followed global equities lower, with the UK, French, and German equity indexes falling by 2.33%, 1.52%, and 1.30% respectively over the past five days ending Thursday, mainly due to the unexpectedly sharp rise in US inflation data. On the data front, Germany's ZEW Economic Sentiment Index surged to 84.4 in May, the highest level since records began in 2004. The European Union said it expected the epidemic to subside amid the encouraging progress of the COVID vaccination programme, and therefore revised its economic growth forecast higher to 4.2% and 4.4% respectively for 2021 and 2022. As for the central bank policy, an ECB official said that the suggestions that the central bank should withdraw its special bond buying programme early was "pure speculation". Next week, the Eurozone will announce the GDP growth 2021 Q1 and the final CPI for April.

China

China

China equities improved this week, with the CSI 300 Index rising by 2.36% on Friday, tallying a 2.29% rise for the week, while Hong Kong stocks were bogged down by the weakness in external markets, sending the HSI down 2.04% over the week. China's regulation of platform businesses continued as 10 transportation platforms, including Didi and Meituan, were summoned by authorities, resulting in pressure on the relevant sectors. In addition, inflation concerns in the US also weighed on the performance of the Chinese technology sector and the MSCI China Index. Next week, China is expected to release the April fixed investment, industrial production, and retail sales data, the latest LPR will also be announced.