Weekly Insight May 21

US

US

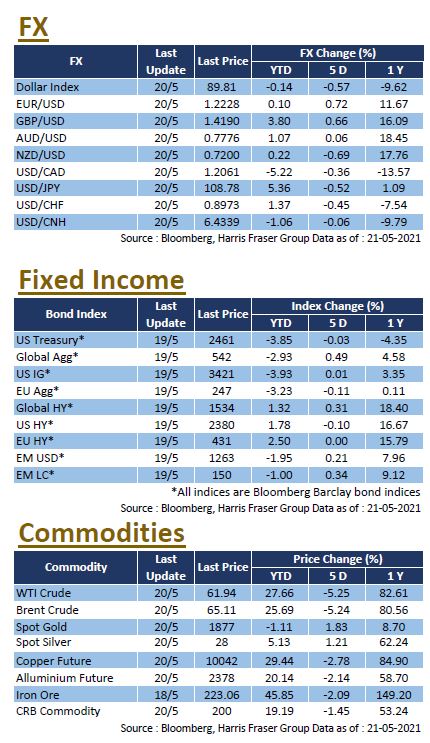

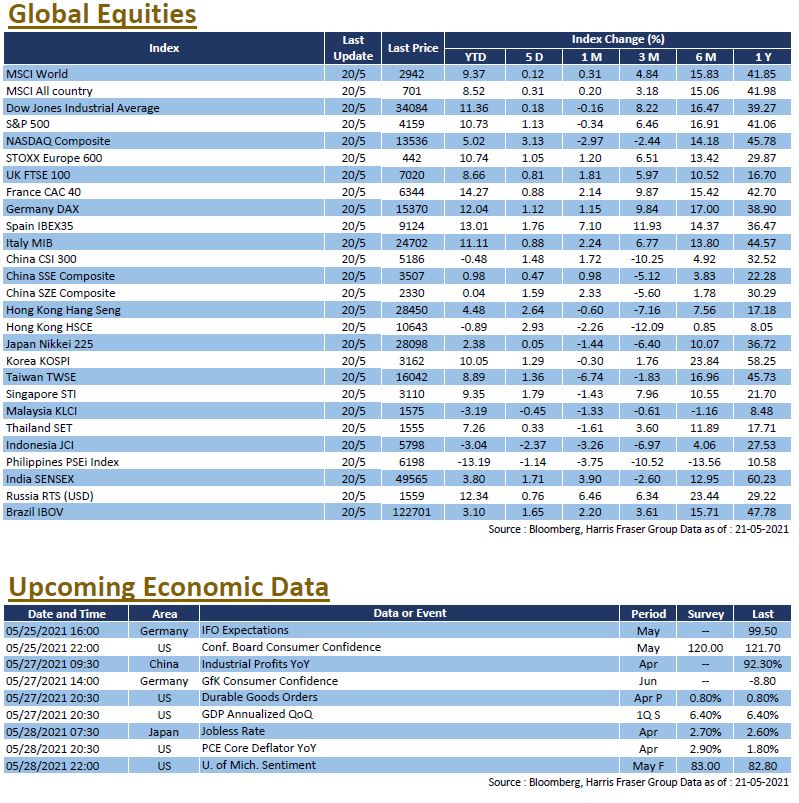

As inflation fears lightened, commodities retreated and yields stabilised, high growth sectors such as tech stocks bounced back. The NASDAQ gained 3.13% over the past 5 days ending Thursday, while the Dow & S&P 500 Index gained 0.18-1.13% over the same period. The Fed released their April meeting minutes, officials were quoted saying tapering will be considered if the economy shows rapid progress. More importantly, they acknowledged the current inflation, but dismissed it as a transitory phenomenon, expecting it to ease eventually. The reduced inflationary expectations further supported high growth stocks, as valuations stabilise under less rate hike pressures. In other news, the wide Crypto market crashed during the week in a spectacular fashion, losing more than 40% in value at one point. While there doesn’t seem to be a sole reason to blame behind the crash, a slew of negative factors, including Elon Musk’s twitter, all which contributed to the sustained selloff. Next week, the US will release several key economic data, including consumer confidence, University of Michigan Sentiment, durable goods orders, and PCE core deflator. The revised 2021 Q1 GDP will also be released, where the market expects the figure to stay unchanged from the previous reading.

Europe

Europe

Europe equities followed global markets higher, equity indices in the UK, France, and Germany gained 0.81-1.12% over the week. On the epidemic front, Europe continues to do a good job on controlling the viral spread, and vaccinations continued its rollout on schedule, major economies have hit the 30% population mark as of date. With the situation under relative control, the European leaders have announced to reopen the region to travellers from third countries, if the travellers are vaccinated and coming from epidemiologically safe third countries, this sparks optimism that businesses could see a further boost with the influx of tourist money. The ECB on the other hand voiced concerns over the increasing debt load in the European service sectors, which could possibly pose as a problem if governments lift their stimulus in the future. The bank is also monitoring the bond market closely as the recent climb in sovereign debt yields have raised eyebrows. Next week, Germany will announce figures for IFO Business Climate and Gfk consumer confidence.

China

China

Chinese equities stabilised over the week, the CSI 300 Index gained 0.46%. Whereas for Hong Kong, despite Tencent’s subpar earnings report, the Hang Seng Index rose 2.64%, led by the rebound in new economy sectors,. The Chinese banking regulator announced penalties on 5 financial institutions over improper business practices, which shows the Chinese determination on reforming the financial sector. In other news, it was reported that the Chinese authorities will not provide full-fledged support to the troubled Huarong, sending the bond prices of longer dated bonds down for both the onshore and offshore markets. Next week, China will announce the latest figures on industrial profits.