Weekly Insight June 17

US

US

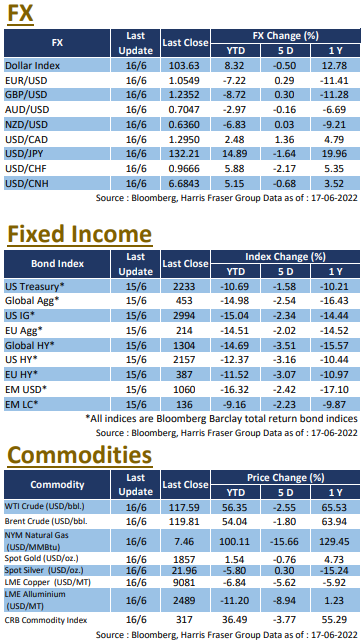

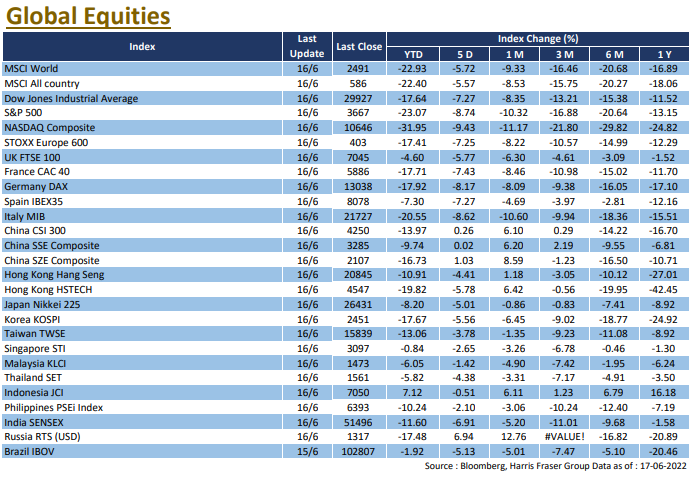

Although the US Federal Reserve's 75 bps rate hike was in line with market expectations and allowed the US market to rebound slightly on the same day, market fears of recession continued to grow and US equities plunged again on the following day, with the Dow falling below the 30,000 level and the Nasdaq falling over 4.7% in a single day. Since year start till 16th June, the S&P 500 and NASDAQ have fallen by 23.1% and 32.0% respectively, both entering technical bear market territory. On the day the hike was announced, Chairman Jerome Powell said large rate hikes would not be the norm, and that a rate hike of only 50 or 75 bps is expected in the next meeting. According to the Fed dot plot, members expect the median federal funds rate to be 3.375% by the end of this year, rising further to 3.75% by the end of 2023, before returning to a moderate 3.375% by the end of 2024, and the median long-term rate is still at a neutral 2.5%. The dot plot showed a sharp increase in members' expectations for interest rates at the end of this year compared to their forecasts in March, with the median of 3.375% in June compared to 1.875% back in March.

With expectations of further rate hikes, bond yields were up across the board, the two-year US Treasury yield rose to 3.45% before the Fed meeting, and the 10-year hit 3.49%. In addition, the 30-year US mortgage rate rose sharply to 5.78%, the largest one-week jump since 1987. Current interest rate futures data suggest that there is still a chance that rates will rise by 75bps at the July meeting, with rates set to rise to around 3.5% by the end of the year. Some economic data were weak, with retail sales falling in May for the first time in five months and New York State manufacturing PMI unexpectedly contracting for the second month in a row. Next week, US manufacturing and services PMI data for June will be released.

Europe

Europe

Ahead of the Fed's rate meeting on Wednesday, the European Central Bank (ECB) called an emergency meeting to address the spike in Eurozone bond rates. European equities slightly recovered on the day, but the down trend remains, with UK, French and German stocks falling between 5.77% and 8.17% over the past five days ending Thursday. The ECB said at its emergency meeting that it would create a new tool to counter the recent sell-off in European debt markets, and that it would use the flexibility to reinvest funds from the PEPP to mitigate the fragmentation risk in the region and avoid a potential debt crisis. Just as the US Fed rated hikes aggressively, the Swiss central bank also raised interest rates by 0.5% for the first time in almost 15 years in response to upward pressure on prices. Next week, the Eurozone will release its PMI and consumer confidence data for June.

China

China

Hong Kong stocks were more affected by external news this week. The market was particularly concerned over whether the US Federal Reserve would tighten monetary policy significantly after the unexpectedly high inflation data in the US, which caused Hong Kong stocks to fall; China A-shares were better off, with the CSI 300 index rising 1.65% over the week. It was reported that the leaders of the US and China might talk on the phone soon, raising expectations that both sides might propose tariff cuts. In addition, the Russian Stock Exchange announced that from 20th June, local brokers will be able to trade 12 Hong Kong listed shares, which will further increase to 200 and 1,000 by the end of 2022 and 2023 respectively. Next week, China will announce the latest Loan Prime Rate quote (LPR).