Weekly Insight June 24

US

US

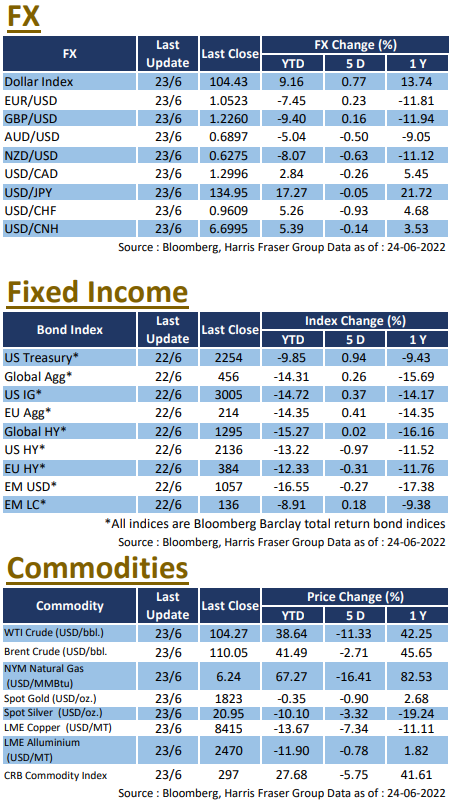

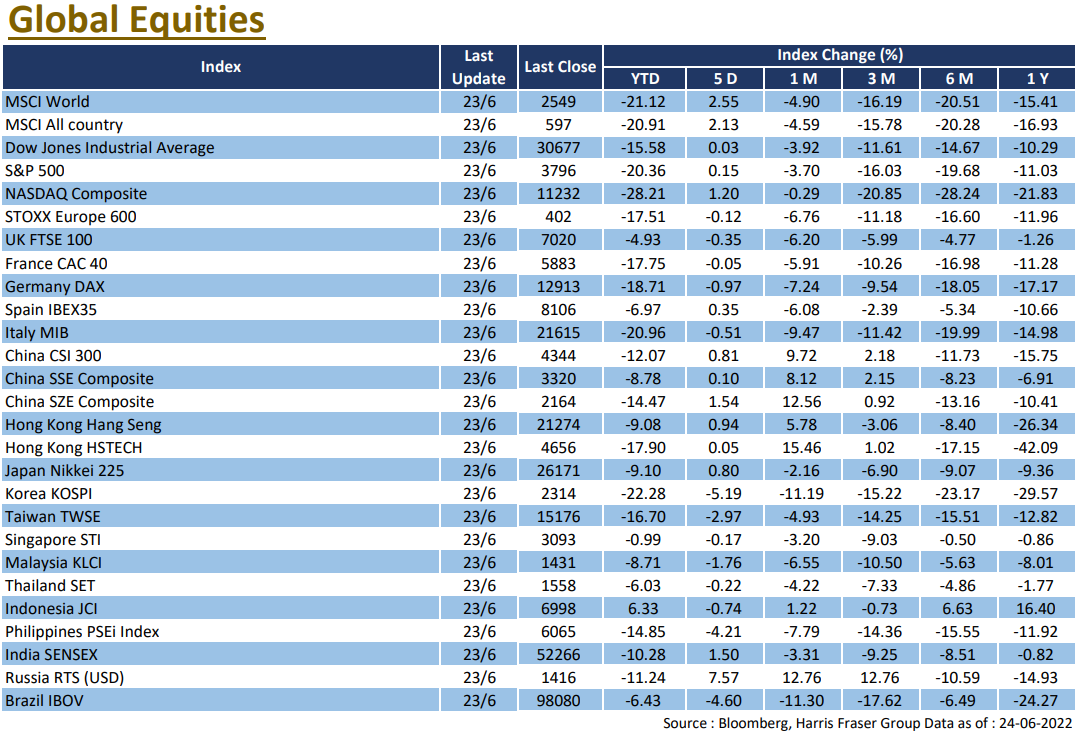

Stocks stabilised slightly after Fed Chairman Jerome Powell argued at the Congress testimony that recession is not ‘inevitable’, with the Dow and S&P edging up 0.03% and 0.15% and the NASDAQ up 1.2% over the past five days ending Thursday. At the Congress testimony, Powell acknowledged that recession was a possibility and that achieving a 'soft landing' would be challenging, but that the Fed's commitment to reducing inflation is 'unconditional'. Fed Governor Bowman said he would support a 75 bps rate hike in July, followed by several 50 bps hikes. Interest rate futures data suggest that a 75 bps hike is likely at the July meeting, and that rates will reach 3.5% by the end of the year. The market remains concerned over inflation trends and the Fed's comments.

In addition, the market is concerned about whether the US will slip into recession. Recent economic data from the US has been lacklustre, with the preliminary manufacturing PMI at 52.4 for June, down from the previous month's final reading of 57 and below the expected reading of 56. In addition, the rise in US interest rates, with the 30-year mortgage rate at its highest level since 2008, will have a negative impact on the housing market. Market participants are conservative on the economic outlook, with the CEO of Deutsche Bank and economists at Citi predicting a 50% chance of a global recession. Next week, the ISM Manufacturing Index and Consumer Confidence Index will be released in the US.

Europe

Europe

After a period of correction, European equities were range bound in the short term, with UK and French equities flat over the past five days ending Thursday while the German DAX was down 1.63%. In the face of inflationary pressures, ECB President Christine Lagarde said she expects a 25 bps rate hike in July, followed by further hikes in September, and noted that financial risks in the region have risen significantly over the course of the year. ECB Governing Council member Olli Rehn said the sharp rise in prices gave a strong case for a rate hike next month. Another member of the Governing Council, Peter Kažimír, said negative interest rates must become a thing of the past by the end of September. German and French manufacturing PMIs both fell in June. Next week, the Eurozone will announce the CPI for June and the unemployment rate for May, with the market expecting the CPI to rise further to 8.3% YoY.

China

China

The improving external sentiment led to a stronger performance of the Hong Kong and Chinese stock markets, with the CSI 300 Index up 1.99% and the Hang Seng Index up 3.06% over the week, outperforming external equity markets as a whole. News of the easing epidemic and the implementation of supportive policies continued to support Hong Kong and China's equity markets. In a Central Committee meeting chaired by President Xi Jinping, the healthy growth of payments and financial technology was approved. Market expects more regulatory relief for technology companies such as Ant Group. Next week, China will release official and Caixin manufacturing PMI data for June.