Weekly Insight August 5

US

US

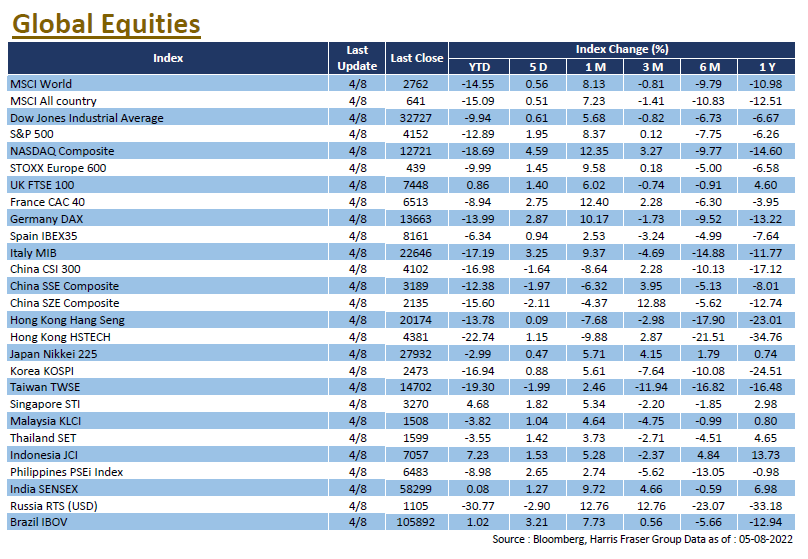

While Asian stock markets were shaken by US House Speaker Nancy Pelosi's visit to Taiwan, US stocks managed to maintain their momentum, with the tech heavy NASDAQ seeing a bigger rebound, up 4.59% over the past 5 days ending Thursday, while the S&P 500 and Dow rose 1.95% and 0.61% over the same period. Several Fed officials have recently made hawkish comments, reiterating that maintaining price stability is their top priority. The Cleveland Fed President reiterated the Administration's determination to curb inflation by raising interest rates, while the San Francisco Fed President also said that a 50 bps hike is most likely at the September meeting.

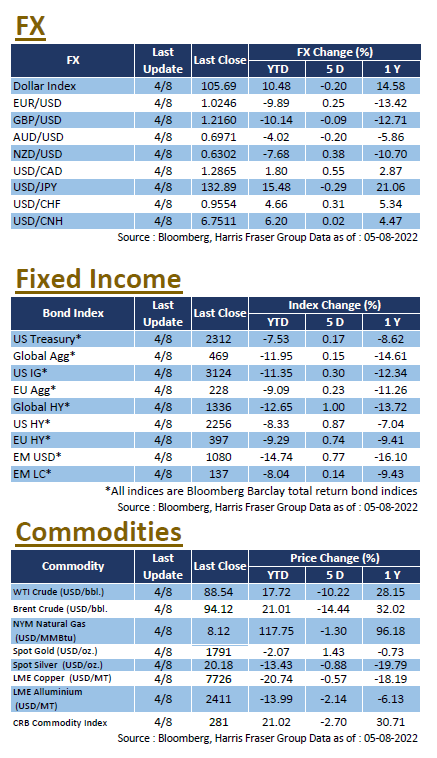

Recent data from the US was mixed, with the ISM Manufacturing Index falling to a two-year low of 52.8 in July, mainly due to a contraction in orders and an increase in inventories, while the ISM Services Index unexpectedly rose to a three-month high of 56.7 in July, ahead of market expectations of 53.5. The number of job openings in the US fell to a nine-month low of 10.698 million in June, slightly below market expectations of 11 million, indicating a slight moderation in labour demand. Next week, the University of Michigan market sentiment for August and the CPI for July will be released, with the market expecting the annual CPI rate to slow to 8.8% from 9.1% in June.

Europe

Europe

European equities followed US markets, with the UK, French, and German equities rising between 0.33% and 1.32% over the past 5 days ending Thursday. The Bank of England raised its policy rate by 50 bps to 1.75% after the interest rate meeting, which was the largest hike since 1995. The central bank warned that the UK could face more than a year of recession under the pressure of soaring inflation. On the data front, the Eurozone's preliminary Harmonised Index of Consumer Prices (HICP) rose by a record 8.9% YoY in July, adding to concerns over inflationary pressures; retail sales in the Eurozone fell by 3.7% YoY in June, exceeding the expected drop of 1.7%. Next week, the Eurozone industrial production for June and the Sentix Investor Confidence Index for August will be released.

China

China

Tensions over the Taiwan Strait triggered a sharp fall across Asian stock markets, affecting both China A-shares and Hong Kong stocks, though both recovered lost ground later on. The CSI 300 Index was slightly down 0.32% over the week, while the Hang Seng Index edged up 0.23%, investors remained on the lookout for the latest developments. On the earnings front, Alibaba's second quarter revenue fell for the first time on record, but the drop was smaller than expected. In addition, the People's Bank of China (PBOC) held the working meeting for the second half of the year, which called for maintaining adequate liquidity, stable and moderate growth in monetary and credit terms, and prudent resolution of risks in key areas. Next week, China will announce the PPI and CPI for July.