Weekly Insight September 30

US

US

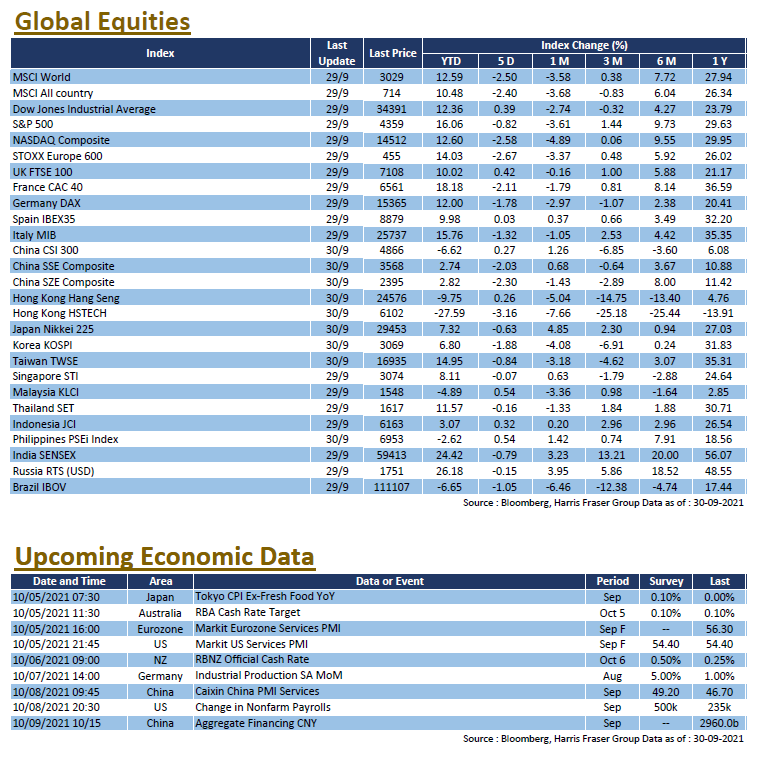

The US equity markets logged in one of the larger single-day declines on Tuesday, as sentiment was hit amid market uncertainties. Over the past 5 days ending Wednesday, the NASDAQ took the largest hit, losing 2.58%, the S&P 500 lost 0.82%, while the Dow managed to hold a 0.39% gain. On the economic front, core durable goods orders missed market estimates, coming in 0.2% versus the 0.5% consensus. Conference Board Consumer Confidence Index also fared worse, as the reading of 109.3 for September is both lower than the estimate and the August figure. Fed Chairman Jerome Powell still insisted the view that inflation should ease eventually, but admits that the current pressures could stay well into 2022.

Treasury Secretary Janet Yellen told the Congress that the Treasury will run out of cash by 18th October if the debt ceiling is not addressed, potentially risking the first US default and causing systematic risk to the global financial system. The House have passed a bill to suspend the US debt ceiling, but it is expected to fail in the Senate. It remains to be seen how the Democrats will try to avoid the possibility of default. Next week, the US will release important data including the ISM non-manufacturing and Markit Services PMIs, non-farm payrolls, and unemployment rate.

Europe

Europe

European equities had mixed performance, UK equities edged 0.35% higher over the past 5 days ending Wednesday, while French and German indices lost 0.91-1.15% over the same period. On the economic front, Eurozone unemployment rate in August was 7.5%, meeting market expectations. European Central Bank (ECB) President Christine Lagarde admitted that there are factors that could potentially lead to higher inflation, but the risks remain limited at the moment. ECB Governing Council Member Mário Centeno reiterated the ECB view that the current inflation level is only temporary, emphasising the need to keep favourable financial conditions until the economy is clearly out of the crisis. Next week, Europe will release the Services PMI and retail sales figures for Eurozone, Germany will also release Industrial Production Data for August.

China

China

With the national day week holidays ahead, the Chinese and Hong Kong stock markets lacked clear direction. The CSI 300 Index was 0.35% higher over the short week, while the Hang Seng Index also managed a 1.59% gain. An abrupt announcement of electricity curbs came out of China during the week, citing electricity shortage in several provinces, hitting industrial hubs in Guangdong and other north eastern provinces, concerns over the potentially lower Chinese industrial production led to a fall in shipping and materials sectors. The Evergrande incident continues to drag on, as the company missed the second offshore bond interest payment. The Group has arranged an around 10 billion CNY stake in Shengjing Bank, but more work is still needed before the Group can meet all outstanding liabilities. Next week, China will release Caixin Services PMI.