Weekly Insight 13/01

US

US

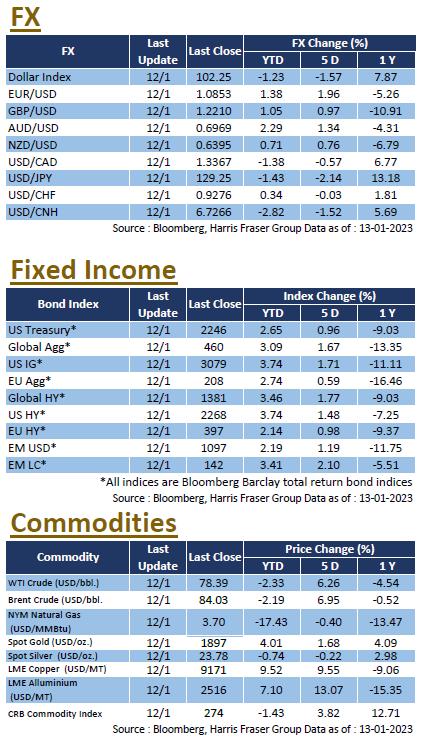

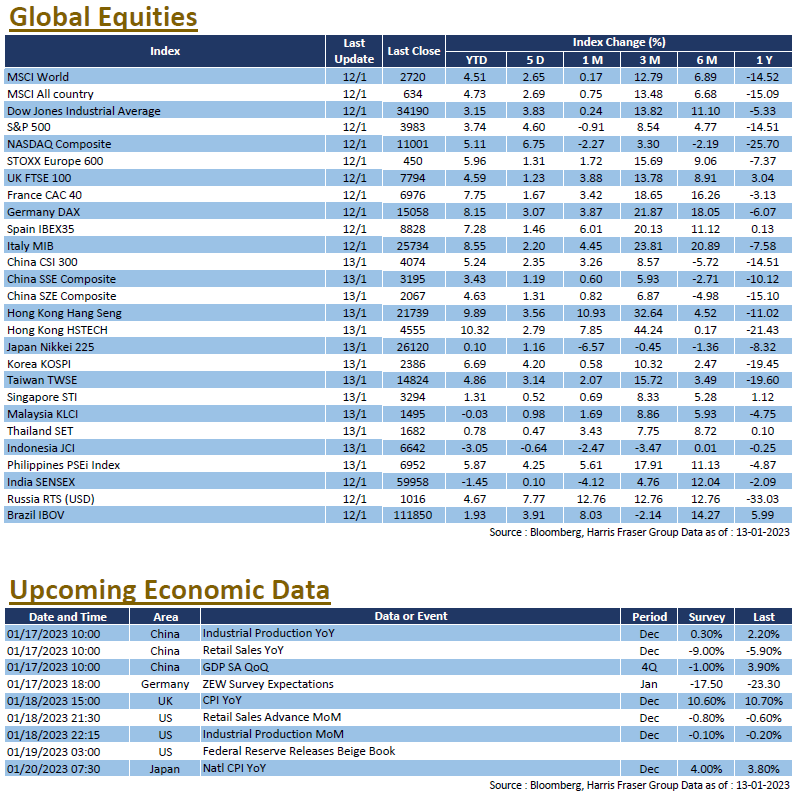

US markets shrugged off the weak performance at the start of the year, and rebounded on the back of more dovish expectations. Over the past 5 days ending Thursday, the 3 major equity indices gained 3.83-6.75%. Fed speakers varied in their message over the week, Philadelphia Fed President Patrick Harker suggested that 25 bps hikes will be ‘appropriate going forward’, but should remain restrictive enough to bring inflation lower. St. Louis Fed President James Bullard on the other hand calls for rates to be raised until 5% is reached as soon as possible. At the time of writing, markets are still pricing in a 25 bps hike in the February meeting, and expect rates to peak in May, 10 year treasury yields also closed in to the 3.4% range.

On the economic front, the CPI in December was 6.5% YoY, falling from the 7.1% in November, and was in line with expectations, the fall of 0.1% MoM was also the first MoM contraction since June 2020, with the 9.4% fall in gas prices being a major contributor, shelter costs remain elevated. The tightness of the labour market is also a big concern, with continuing and initial jobless claims coming in lower than expected. Next week, the US will release PPI figures and industrial production for December, as well as property sector data including building permits, housing starts, and existing home sales in December. The usual labour market data of initial and continuing jobless claims will be closely monitored, and the Fed will release the latest Beige Book.

Europe

Europe

European markets continued the strong performance at the start of the year, the UK, French, and German indices gained 2.10-4.31% over the past 5 days ending Thursday. The ECB released the latest economic bulletin, members expect that recession could happen between Q4 2022 to 2023 Q1, more rate hikes are needed, and price pressures will persist. In a separate occasion, ECB Governing Council member Isabel Schnabel said rates will need to turn restrictive, while Bank of Greece Governor Yannis Stournaras said that there is no wage-price spiral, and medium to long term inflation expectations remain anchored. As for the economy, the UK GDP surprisingly grew 0.1% MoM in November. German industrial production in November grew 0.2% MoM, surpassing expectations of a 0.1% growth. Eurozone unemployment remained unchanged at 6.5% in November, in line with expectations. Next week, Germany will release the ZEW survey data on expectations and current conditions for January, while the UK will be releasing the CPI and retail sales data for December.

China

China

China and Hong Kong markets continued to perform despite lackluster economic data. Over the week, the CSI 300 index was 2.35% higher, while the Hang Seng Index gained 3.56%. After several countries including South Korea and Japan increased inbound restrictions against Chinese travelers, China retaliated by suspending visa issuances. It was reported that China will offer a record quota for local government debt, with further plans to increase the budget deficit to support economic growth. On the economic front, CPI grew 1.8% YoY in December, meeting expectations, while PPI further fell by 0.7% YoY, missing expectations of a 0.1% fall. Next week, China will be releasing a lot of sectorial data for December, including industrial production YoY, retail sales YoY, and fixed assets investments YTD YoY. The GDP figures for 2022 Q4 will also be published, alongside the latest 1 year and 5 year Loan Prime Rates (LPR) will also be released, where markets expect the rates to remain unchanged.