Chinese A-share markets were able to post a positive month even as global equity markets were in a sea of red. Over the month of September, the CSI 300 index was up by 1.26% (1.51% in US$ terms), the Shanghai Composite edged 0.68% higher (0.93% in US$ terms); Hong Kong markets on the other hand followed global markets and lost 5.04% (5.13% in US$ terms).

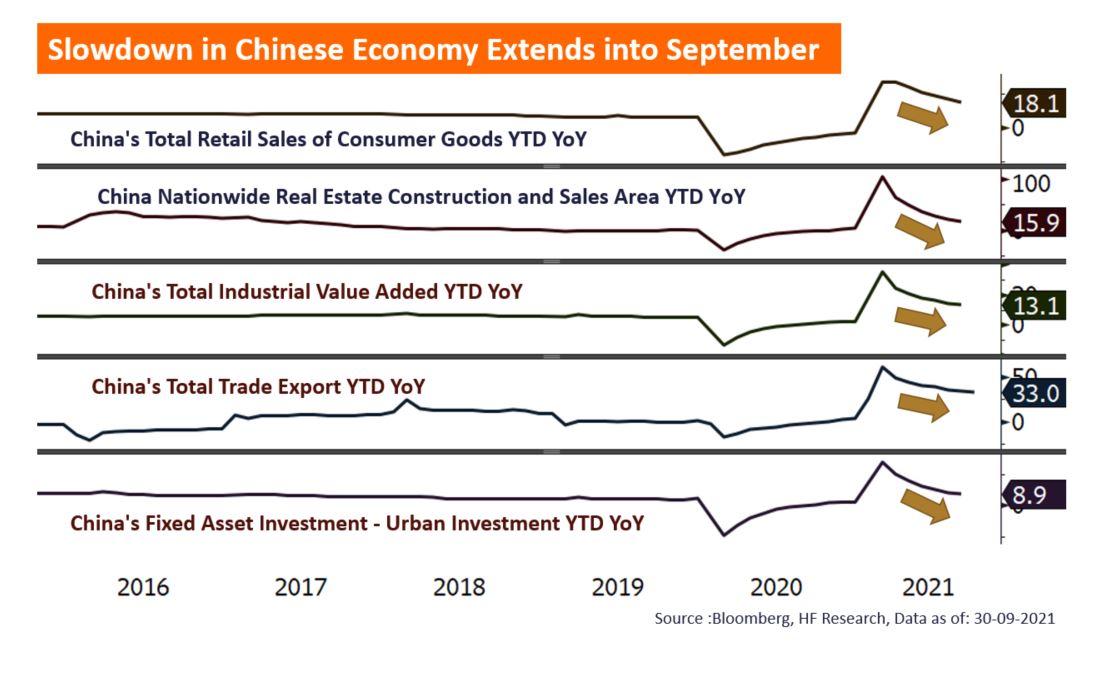

With the pandemic under control in China, economic activities had gradually resumed, which was reflected by the improving economic data, such as the PMIs’ recovery to or close to the expansion level. With the vaccination rates reaching herd immunity levels, and the government adopting effective countermeasures, it was expected that the country can recover and return to pre-pandemic levels. However, unexpected disruptions to the economic activities due to the abrupt power curbs raised concerns over the economy outlook in China.

More so, market uncertainties arising from the ongoing debt crisis continue to impact market sentiment. More Mainland developers defaulted on their debt obligations over the month, the debt-ridden Evergrande group is also on the verge of doing so. With liquidity conditions in China being on tight end, if confidence in the property market further weakens, this could lead to a snowballing problem. Henceforth, as uncertainties in the Chinese market outlook remain, this could hurt market sentiment. We would stay neutral on the market in the short term, only staying selectively positive on segments that are structurally integral to the country.