Weekly Insight 24/03

US

US

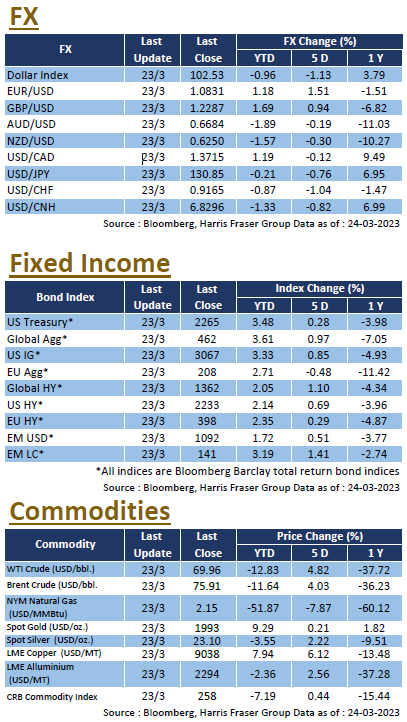

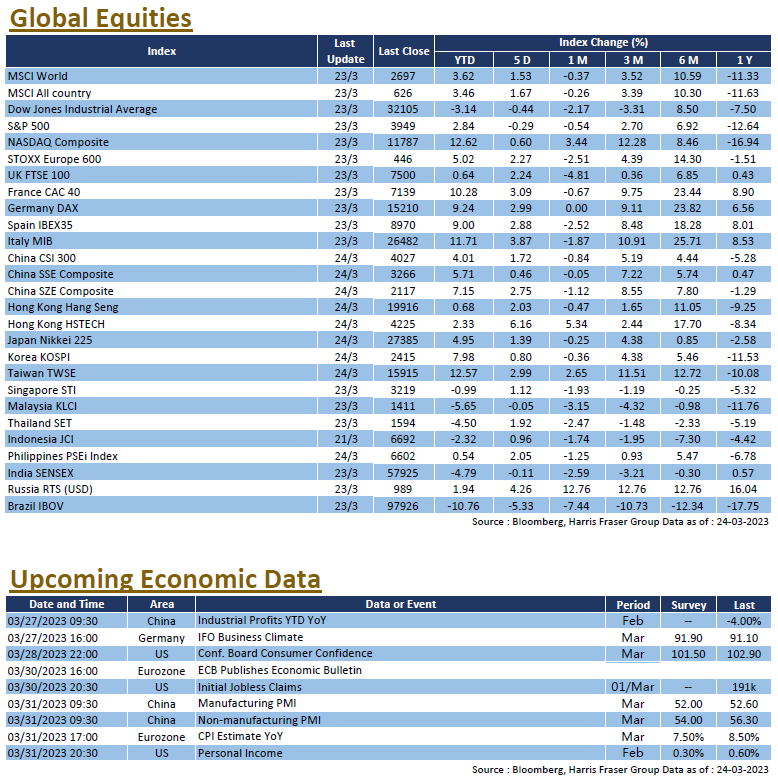

US equities had a mixed week amidst the recent volatility and uncertainty surrounding the banking crisis, the S&P 500 and Dow were down 0.29% and 0.44% over the past 5 days ending Thursday, while the NASDAQ gained 0.60% on the back of easing rate hike expectations. Financials remained under pressure, Treasury Secretary Janet Yellen reassured markets that further actions could be taken to support banks, following her earlier statement that the Treasury is no planning to provide blanket support to all bank deposits. The Fed announced a 25 bps hike during the week as widely expected, but softened the tone on future rate hikes, suggesting that rate hikes might be near its end, depending on future economic data. Fed President Jerome Powell reiterated that rate cuts are not in the Fed’s base case for the year, interest rate futures however ignored Powell and continued to price in 3 rate cuts before the end of the year. The latest Dot Plot also suggested a more divergent Fed, with close to half of the members estimating year end rates to go higher than 5.1%, rate cuts are also expected to arrive in 2024.

As for the economy, housing market data were mixed, new home sales in February were 640K, lower than the expected 650K, existing home sales on the other hand was 4.58M, beating market expectations of 4.19M by a far margin, building permits of 1.55M were also higher than the estimated 1.524M. The labour market data is equally mixed, with initial jobless claims of 191K coming in lower than expected, while continuing claims of 1,694K were higher than market consensus. Next week, the US will publish the Conference Board consumer confidence index for March, PCE data for February, alongside housing market data including mortgage applications and pending home sales. The latest labour market data on initial and continuing jobless claims will also be released.

Europe

Europe

Credit Suisse was deemed unviable and was taken over by UBS through a government brokered deal, market regained footing later in the week as contagion risk seemed under control. Over the past 5 days ending Thursday, the UK, French, and German indices gained 1.21-1.63%. The CS takeover deal saw AT1 bondholder value completely wiped out, which roiled the European AT1 CoCo market. The Bank of England hiked rates for another 25 bps, citing that inflation ‘surprised significantly on the upside’ and the economy was stronger than expected, the bank also suggested that future rate hikes could be warranted if price pressures prove to be persistent. As for the economy, Eurozone consumer confidence of -19.2 in March missed market expectations and was lower than the February figure. German ZEW survey expectations and sentiment both missed market estimates and were lower than the previous figure. Next week, Next week, Europe will publish the latest CPI and economic confidence data for March, Germany will release the IFO business climate and expectations for March, and the UK will publish the finalised GDP data for 2022 Q4. The ECB will also release the latest edition of the Economic Bulletin.

China

China

Hong Kong and China equities stabilised over the week, equity gains were led by the recovery in the tech sector. Over the week, the CSI 300 index gained 1.72%, the Hang Seng Index is 2.03% up, while the Hang Seng Tech Index was 6.16% higher. President Xi met Russian President Vladimir Putin during his state visit to Russia, both sides pledged closer ties, while China calls for a ceasefire in Ukraine, but the details were not well received by the Ukrainian side. More leader across the global have scheduled visits to China in the coming few weeks, including Spain, Brazil, and France, the Ukraine situation is expected to be a main point of discussion. In Hong Kong, Evergrande, the epicenter of the China property sector crisis, have announced the details of the debt restructuring plan, investors will receive new notes or a combinations of debt and other instruments. China announced no changes to the LPR as widely expected, but yet cut RRR by 0.25% from 27th March onwards to release further liquidity back into the market. Next week, China will release the NBS manufacturing and non-manufacturing PMIs for March, as well as the industrial profits data in February.