Weekly Insight July 22

US

US

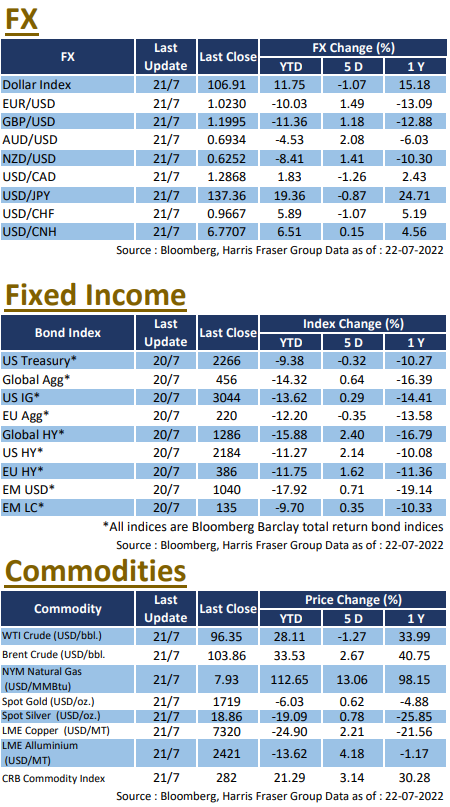

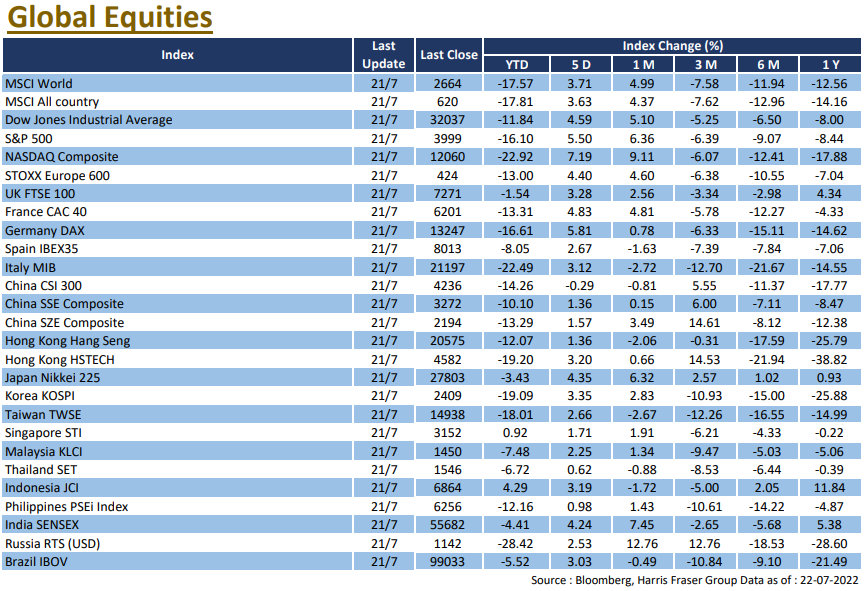

Despite the disappointing results of some of the financials reporting earlier, US stocks continued the rebound, with the three major indices rising between 4.59% and 7.19% over the past five days ending Thursday. US President Joe Biden was reported to have contracted COVID, but he will continue to carry out his duties as President. The market paid great attention to the earnings season, where 71.9% of the 96 reporting S&P constituents beat market expectations. The energy sector had the lowest percentage of earnings beats among all sectors at 33%. According to Bloomberg data, among the 96 reporting companies, the average earnings were down 5.9% YoY.

Large banks were the first to report earnings, apart from Morgan Stanley and JPMorgan Chase, both which reported YoY earnings drops, Bank of America and Goldman Sachs also reported the same. Goldman Sachs' investment banking business reported a decline, and the bank will slow down hiring in an effort to control expenses. Sources said that investment banking in Europe and the US might see a new wave of layoffs unless trading activity rises sharply in September. Despite the banking sector's disappointing results, Tesla reported better-than-expected second-quarter earnings and kept its annual production growth target of 50% unchanged, it also announced that it had converted around three quarters of its bitcoin to fiat currency. Focus next week will be on quarterly results from several Big Tech companies, alongside the release of US Q2 GDP, as well as the Fed's interest rate meeting.

Europe

Europe

The ECB's surprise 50 bps rate hike and heightened political uncertainty in Italy did not deter European stocks from following the rebound in US stocks, as the UK, French, and German stock indices rebounded 1.56% to 2.97% over the past five days ending Thursday. The ECB unexpectedly raised interest rates by 50 bps in one go and introduced a new anti-fragmentation tool called the Transmission Protection Instrument (TPI). ECB President Christine Lagarde said that the absence of forward guidance would give the ECB more policy flexibility, and that countries in the region would have to comply with EU debt rules to use the tool. On the other hand, Italian Prime Minister Mario Draghi officially resigned and the country's snap election will be held on September 25. Next week, the Eurozone will release important data including the Q2 GDP and CPI for July.

China

China

The Hong Kong and Chinese stock markets stabilised this week, with the Hang Seng Index up 1.53% and the CSI 300 Index flat for the week. China's economic outlook was under pressure as the number of new cases confirmed remained high. Premier Li Keqiang said that preserving employment and stabilising prices were key, and that deviations in economic growth would be acceptable, reiterating his cautious stance on large-scale stimulus packages. In addition, the China Banking Regulatory Commission (CBRC) said it would support local authorities in "guaranteeing the delivery of properties" to maintain stable and orderly real estate financing. Next week, China will release industrial profits data.