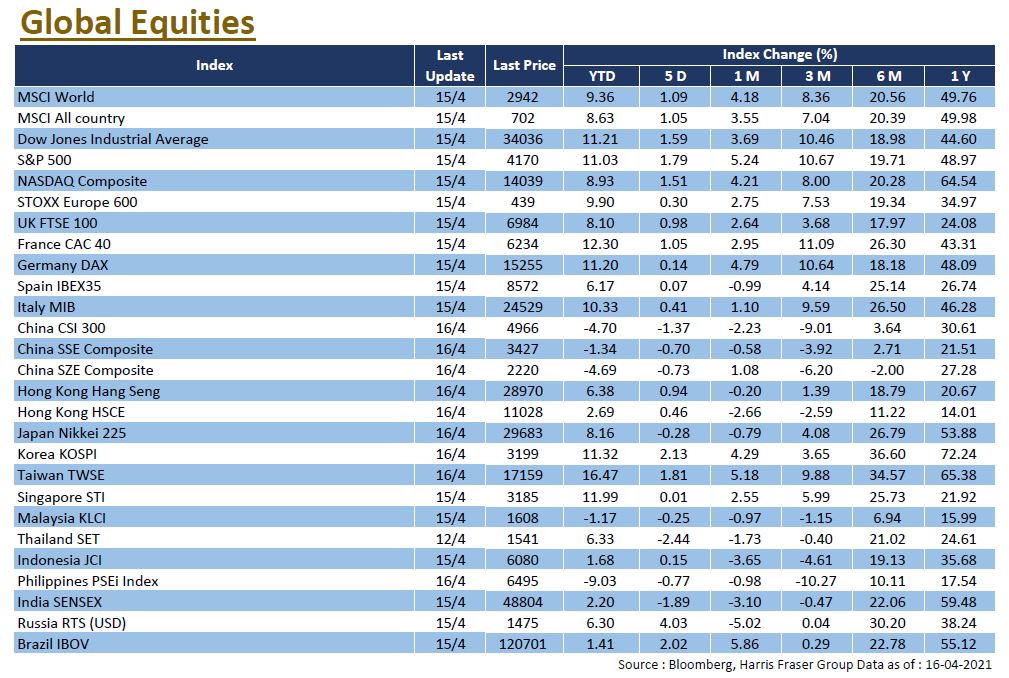

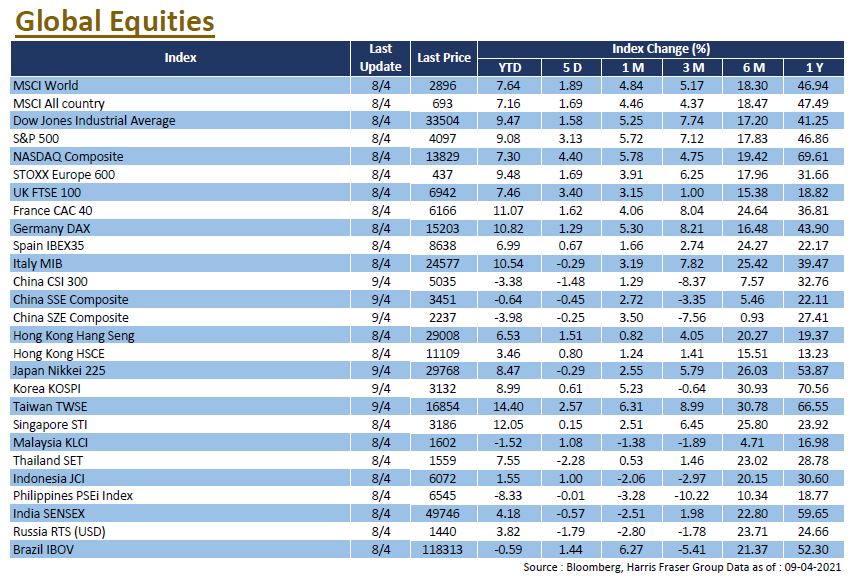

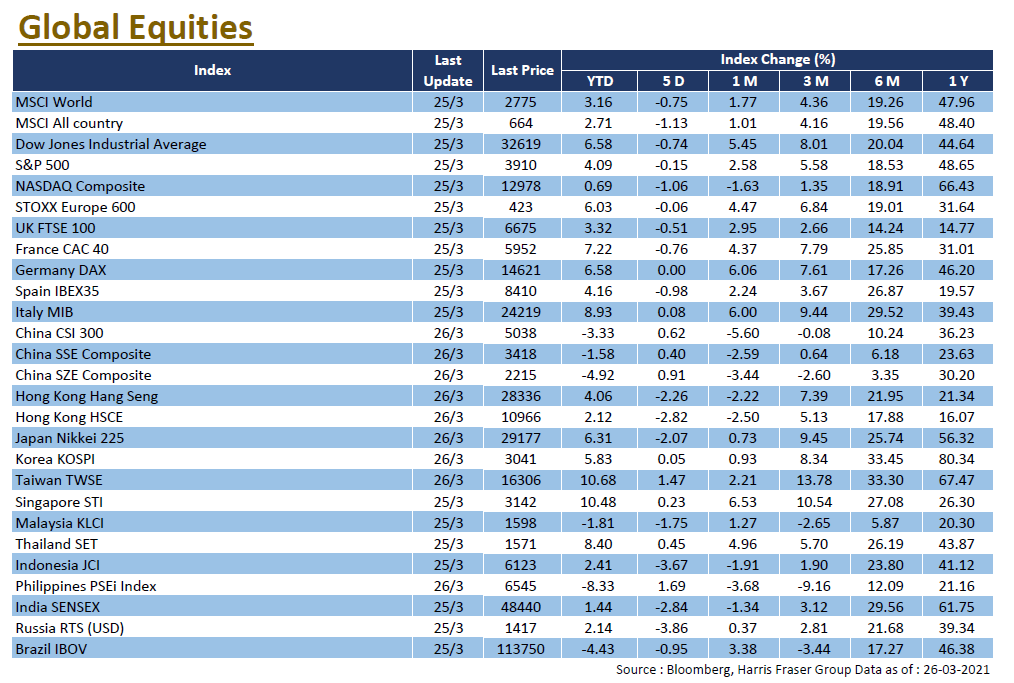

While the 2021 Chinese economy is poised to post the strongest growth in recent years, equity markets have faltered and continued the weak form. The slide in equities were a likely result of a myriad of factors, though the reduced liquidity could possibly be the primary cause. The CSI 300 was down 5.40% (6.55% in US$ terms), while the Shanghai Composite lost 1.91% (3.10% in US$ terms), the Hong Kong Hang Seng Index also fell 2.08% (2.30% in US$ terms).

Chinese economic data remained strong as we expected, PMIs stayed in expansion zone across the board, while industrial profits posted record YoY gains due to the low base effect. Outlook on the Chinese economy remains strong, numerous forecasts put China as one of the top performers in 2021 growth, even the conservative outlook on the ‘Two sessions’ set the figure at higher than 6%, which should be positive for the Chinese corporate earnings.

However, the continued clampdown on the liquidity and speculation in the market had negative impacts on the market as valuation multiples were compressed. Moreover, regulatory authorities are considering having more oversight over some of the largest tech companies in China, which led to fears in the market regarding their growth outlook, sending the indexes down despite the positive economic outlook. That said, the main driver for the market slide was due to valuation contraction, which should likely have a temporary effect on the equity performance only. In short, the growth potential in the economy should still favour equities in the mid to long-term, we remain positive on the Chinese market for the year.

US

US Europe

Europe China

China