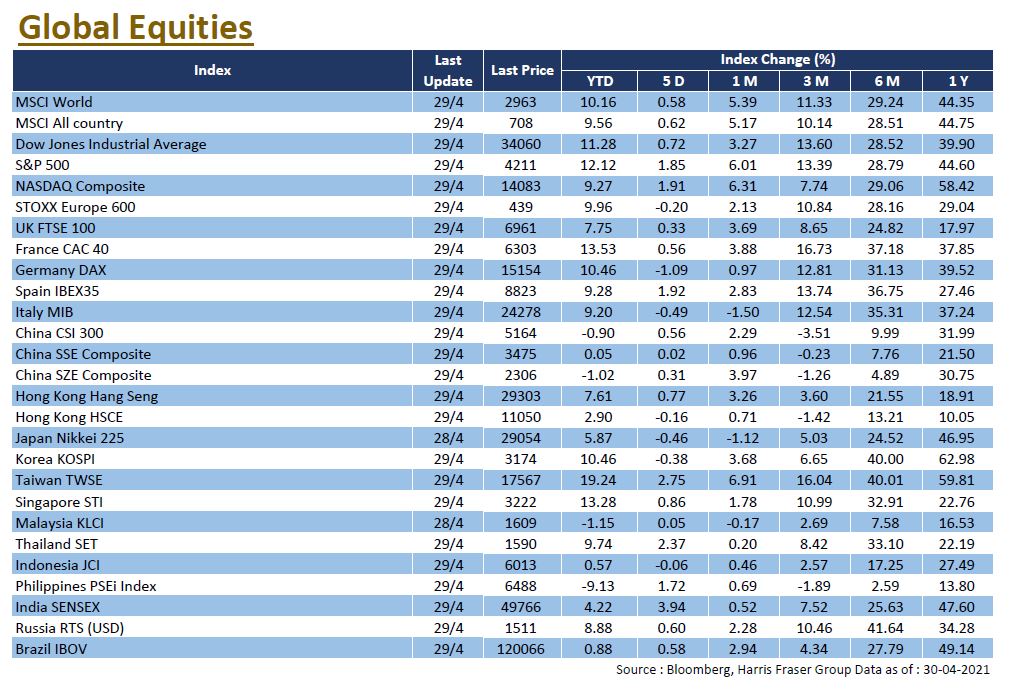

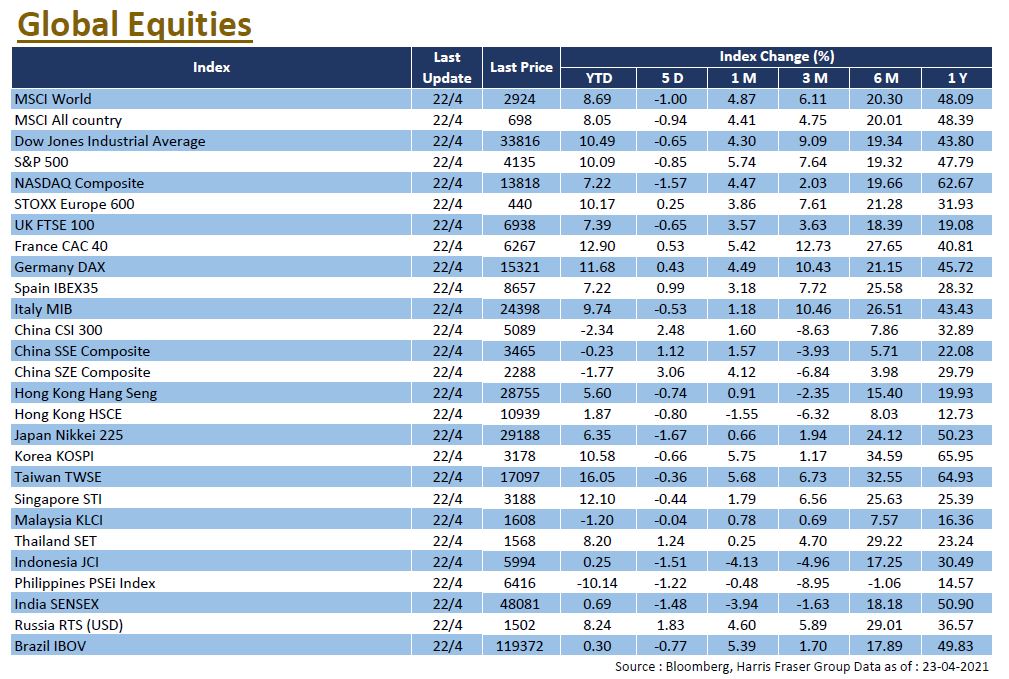

The recovery story continues, the US market maintained its upward momentum and returned positive for the month. Big Tech bounced back further after the dip at last month end, outperforming cyclicals as represented by the Dow, strong corporate earnings for 2021 Q1 further boosted the performances of the biggest pandemic winners. Over the month, S&P 500, Dow, and the NASDAQ gained 5.24%, 2.71%, and 5.40% respectively.

The US economic fundamentals remained strong ever since the pandemic low, which is further boosted by the robust vaccine deployment. Currently, with the pandemic past its peak in the US, local governments have relaxed restrictions accordingly, business environment is returning back to normal in a majority of States. Under the overall economic recovery, we keep our views on US equities unchanged, with the emphasis on small caps for the recovery play.

Looking forward, risks in the market could have a negative drag on market performance. As the supply gap will likely persist in the short term, inflation is likely here to stay. This could have impact on the future fiscal and monetary policy, where the current easy monetary policy could possibly end earlier in order to limit the inflationary impact. Another thing to look out for is the pending tax reform that could impact the market in 2 major ways, the raise in capital gains tax could trigger a selloff to reduce the taxes payable, while the raise in corporate taxes and implementing minimum tax could impair corporate earnings. While we stay positive on the US market, there could still be more volatility to come depending how these turn out.

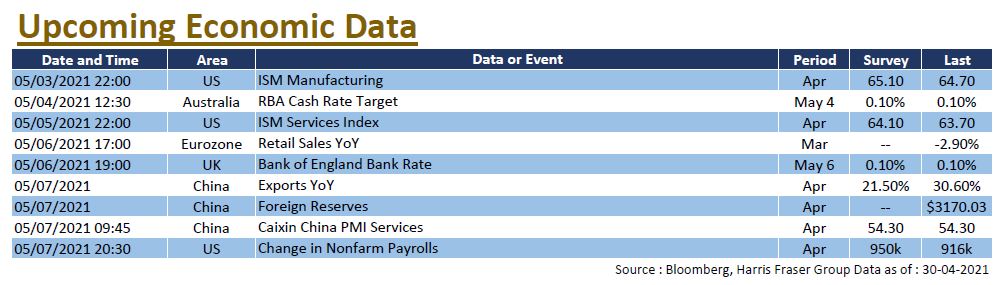

US

US Europe

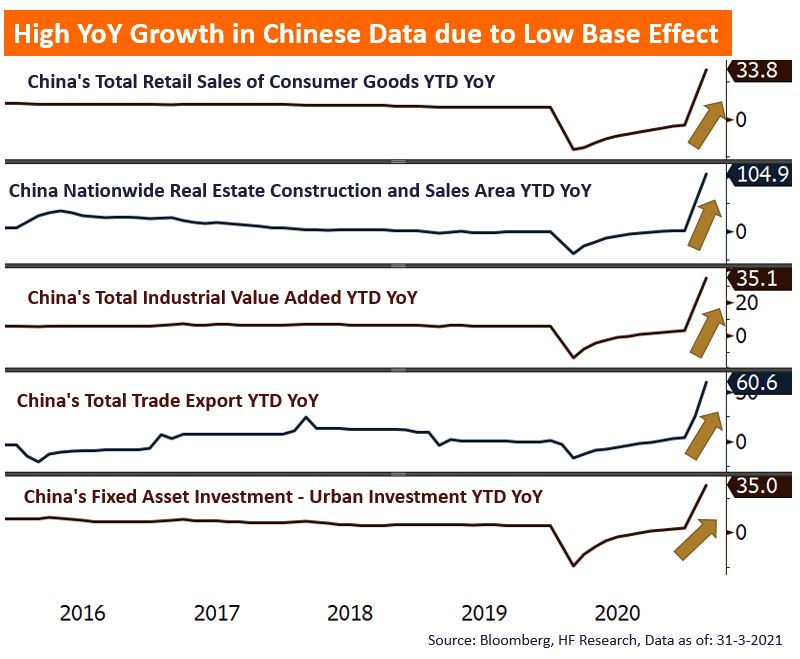

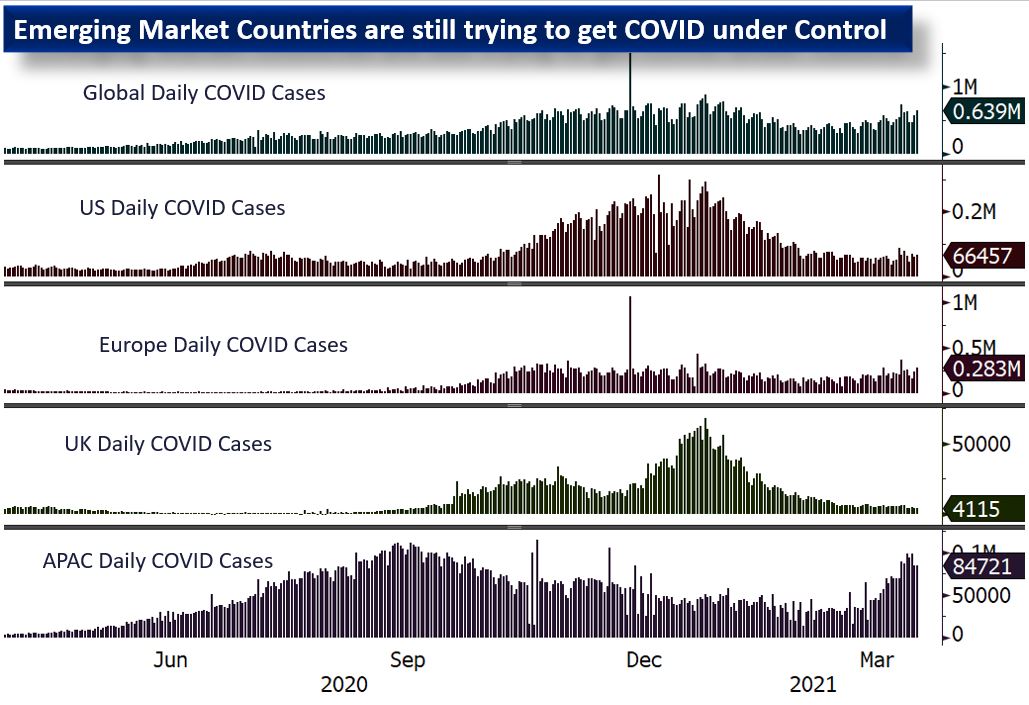

Europe China

China

{kind=link}

{kind=link}

{kind=link}

{kind=link}