Weekly Insight October 22

US

US

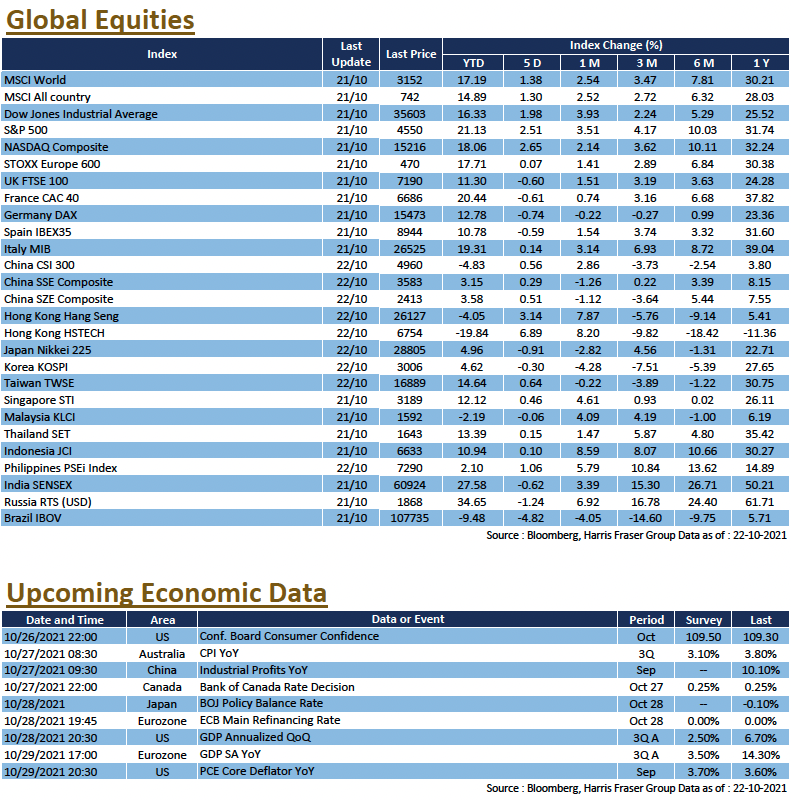

Strong Q3 earnings in the US boosted market confidence, as the S&P 500 hit a new all-time high. The three major US stock indices continued their strong form over the past five days ending Thursday, posting gains of 1.98% - 2.65%. Of the 109 reporting S&P 500 companies, more than 80% reported earnings beats; In particular, among the 31 reporting financial institutions, 87% beat earnings estimates, driving the S&P 500 Banks index up 6.7% MTD.

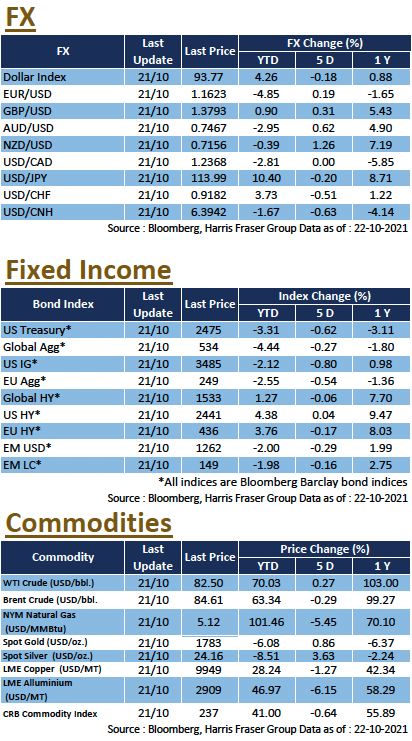

Global energy supply shortages persist, it was reported that OPEC+ missed output targets again last month, and Russia has not increased natural gas supply to Europe. Data showed that US Cushing crude inventory recorded the largest fall since February this year, while gasoline stockpiles also fell to a two-year low. The WTI crude futures price peaked at US$84.25 per barrel. The S&P 500 Energy index rose 10.0% month-to-date, driven by higher oil prices. In addition, copper prices surged as physical copper stocks on the LME fell to their lowest level in over 40 years.

High energy prices kept inflationary expectations elevated, increasing tapering pressure on the Fed. According to Bloomberg interest rate futures, market expects the Fed to raise interest rates twice by the end of 2022. US Fed governor Christopher Waller pointed out that the Fed may need to accelerate its monetary tightening if inflation remains too high. The US 10-year Treasury yield, which is an indicator of interest rate policy expectations, hit 1.7%. Next week, the US will release important data including the preliminary Q3 GDP and the core PCE for September.

Europe

Europe

European equities are in a weaker form compared to the US, with the UK, French, and German indices posting losses between 0.60% and 0.74% over the past five days ending Thursday. Europe's latest quarterly earnings were not as stellar as those of the US, with only 57% of the 97 reporting STOXX 600 constituents beating market estimates, which is far below the US figure of over 80%. In addition, the European Central Bank (ECB) policy is troubled by rising inflation, ECB Governing Council member and Bank of Slovenia Governor Bostjan Vasle said that inflation in the Eurozone may exceed expectations, and the Bank should end the PEPP after March 2022. Next week, The Eurozone will announce its preliminary GDP for the third quarter, and the ECB will also hold an interest rate meeting.

China

China

China A-shares were stable, with the CSI 300 Index rising 0.56% this week. In Hong Kong, the HSI rose above its 50-day moving average, and was up 3.14% over the week, as sentiment improved in recent weeks, with technology equities leading the market rebound. The market is still focused on the Chinese debt crisis. While it was reported that the asset disposal agreement between Evergrande and Hopson Development fell through, it was later revealed that Evergrande had remitted the interest on the USD bonds before the deadline, narrowly avoiding a default. In the commodity futures market, China's Development and Reform Commission said it was studying specific measures to intervene in coal prices, sending domestic coal futures plunging, and dragged down coal-related names. Next week, China will release figures on the September industrial profits.