Weekly Insight 06/04

US

US

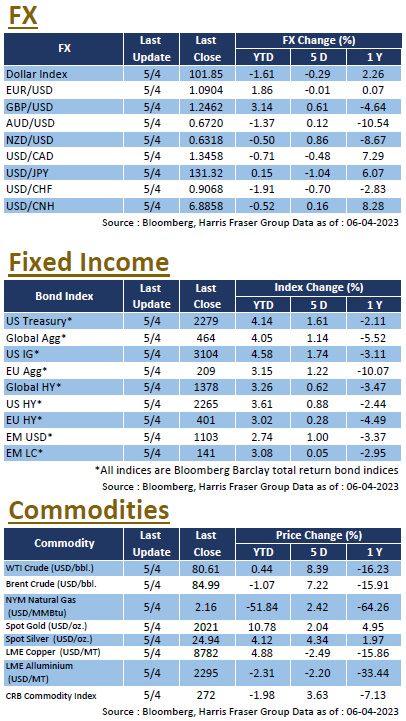

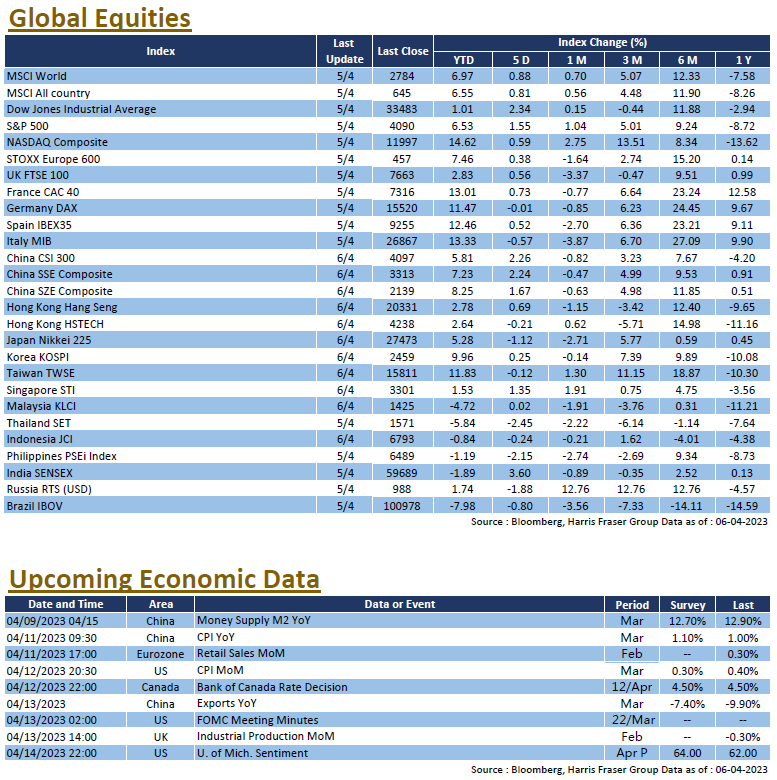

While earlier concerns over the confidence crisis in the banking sector seems to have ebbed out, ne worries have kindled with the weaker economic data as of late. Major equity indices in the US had a mixed week, with the S&P 500 and the Dow gaining 0.98-1.90% over the past 4 days ending Wednesday, while the NASDAQ edged 0.14% lower. Cleveland Fed President Loretta Mester reemphasised that controlling inflation remains a key focus of the Fed, and suggested that rates should stay above 5% and hold. However, markets remained on the fence regarding whether the Fed will hike rates in the May meeting, and futures are pricing in around 3 rate cuts before the end of the year. Longer end treasury yields have fallen further amidst concerns over recession, with the 2Y yield falling to the 3.75% level, and the 10Y yield as low as 3.3%. Amidst the concerns on the economic health, OPEC announced a surprise production cut in response to the falling crude demand, WTI futures jumped to the $80 level, and this raises concerns over inflation possibly going higher.

As for the economy, both ISM PMIs in the US were weaker than expected, ISM manufacturing PMI was 46.3 in March, missing expectations and hit the lowest level since May 2020, ISM non-manufacturing index was 51.2 in March, missing market expectations of 54.5 by a far margin. JOLTs job openings in February was 9.931M, which fell below 10M for the first time, and was the lowest since June 2021. ADP employment change in March was 145K, missing expectations of 200K, both data points are now seemingly hinting at easing of the labour market. Next week, all eyes will be on the March CPI data releases, the US will also release the University of Michigan Sentiment for April, as well as March data on NFIB business optimism, industrial production, and retail sales data. The usual labour market data on the latest initial and continuing jobless claims will also be released, and the Fed will publish their FOMC meeting minutes for the March meeting.

Europe

Europe

Trading week on European markets were cut short due to the Easter holidays, indices were mixed, with the German DAX slipping 0.01% lower over the past 4 days ending Wednesday, while the UK FTSE and French CAC gained 0.56-0.73% over the same period. More ECB officials have commented on the monetary policy outlook, with a majority of them agreeing that the majority of rate hikes are completed and further hikes might be limited. As for the economy, both German factory orders and industrial production grew MoM in February, surpassing market expectations. Eurozone Services were slightly revised downwards from 55.6 to 55.0 in March, but is still at the highest level since May 2022, manufacturing PMI was revised higher to 47.3, but remains in the contraction zone. Next week, there will only sparse economic data releases in Europe, Eurozone will release the retail sales and industrial production data for February, Germany and France will release the final CPI for March, and the UK will publish the industrial production data for February.

China

China

Hong Kong markets had a really short trading week due to Ching Ming and Easter, markets reassess the current situation of the Chinese economy after mixed data releases. Over the past 4 days ending Thursday, the CSI 300 gained 1.13%, while the Hang Seng Index lost 0.34%. Regarding geopolitical tensions, Taiwan President Tsai Ing-wen had an unprecedented meeting with US House Speaker in the US. On the other hand, French President Emmanuel Macron and European Commission President Ursula von der Leyen were in China on a state visit, China’s blueprint for the Ukraine conflict resolution will likely be a key discussion topic. As for the economy, Caixin Manufacturing PMI was 50.0 in March, lower than the market expected 51.7, Caixin Services PMI on the other hand was 57.8 in March, which is the highest since November 2020. Next week, China will be releasing more data on the March CPI and PPI, as well as exports data and new home prices for March. Financial conditions data on Money supply M2, new loans, and aggregate financing data is also scheduled to be released in the week.