Weekly Insight February 11

US

US

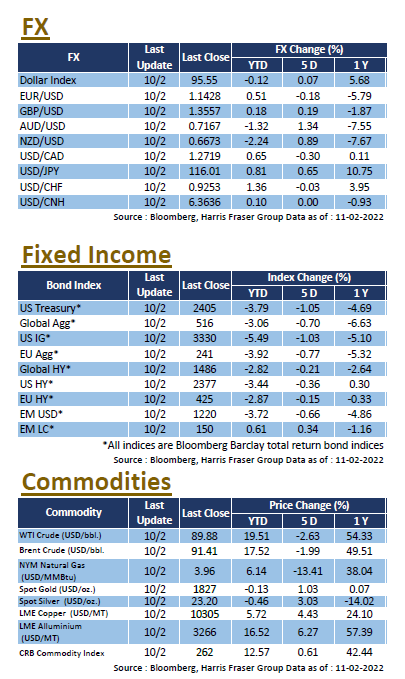

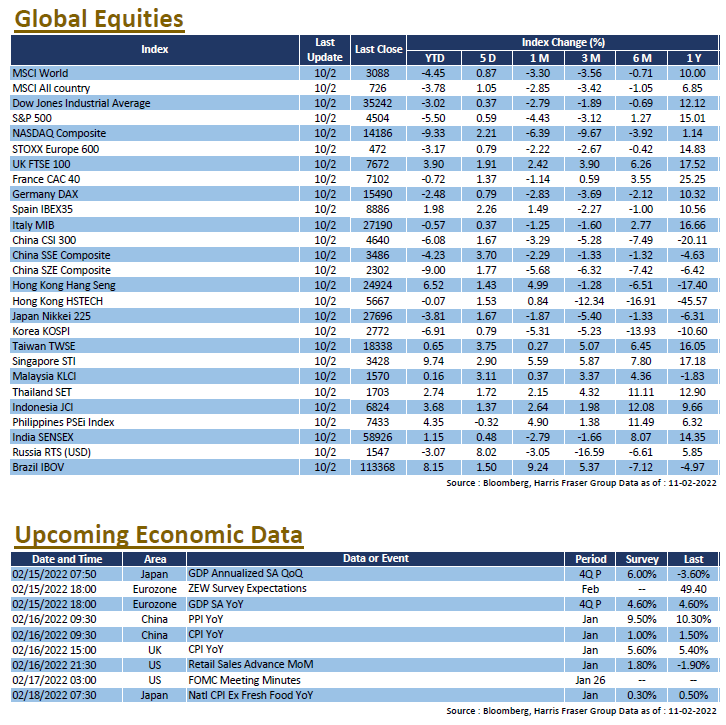

US inflation hit a 40-year high, leading to worries that the Fed will raise interest rates at a faster pace, nearly wiping out all equity gains over the week. The Dow and S&P the 500 narrowed their gains to 0.37% and 0.59% over the past 5 days ending Thursday. The US Consumer Price Index (CPI) rose 7.5% YoY in January, above the market estimate of 7.3%. The core CPI, which excludes energy and food prices, rose 6.0% YoY, which was also higher than the estimate of 5.9%, both hitting a 40-year high. Interest rate futures data show that the probability of a 50-bps rate hike in March rose to nearly 100%, and the full-year rate hikes may total over 150 basis points.

As for corporate earnings, among the 356 reporting S&P 500 constituents, almost 77% of them reported market beats, of which 87.5% of the tech sector beat estimates, including heavyweights such as Apple and Amazon. In addition, to avoid a government shutdown after 18th February, the House of Representatives has passed a three-week stopgap spending bill, which has been submitted to the Senate for a vote. Next week, the US will release the minutes of the January interest rate meeting on 17th February, and the market will be watching out for more details on tapering. In addition, US retail sales data for January will also be released.

Europe

Europe

High inflation and interest rate hikes were also on the agenda in Europe, but over the past 5 days ending Thursday, European equities were still able to record gains, with UK, French, and German equities rising between 0.79% and 1.91% over the period; Eurozone CPI rose 5.1% YoY in January and core CPI rose 2.3%, both higher than market expectations. Later, ECB President Christine Lagarde admitted that inflation was a problem after the interest rate meeting and did not rule out rate hikes this year, leading to market speculation that the ECB might raise interest rates later on. Interest rate futures market indicates that the ECB may raise interest rates by 0.1% in June, and would raise interest rates by a total of 0.5% for the year. Next week, the Eurozone will announce the revised GDP for 2021 Q4.

China

China

The negative news of certain drug companies being included in the US commerce department’s ‘unverified’ list for exporters pressured the Hong Kong biotechnology index, but the news of the government related funds’ market activity boosted both China and Hong Kong stock markets, with the CSI 300 and the Hang Seng index posting gains for the week. China's total foreign exchange reserves fell slightly to 3.221 trillion yuan in January, but with further relaxation of the capital market, aggregate financing and new RMB loans both rose sharply in January, to 6.17 trillion yuan and 3.98 trillion yuan respectively; money supply M2 also rose to 9.8% YoY in the same period, compared to previous 9.0% YoY figure.

27 January 2022

27 January 2022  16:30 - 18:30

16:30 - 18:30 Zoom 線上會議

Zoom 線上會議

{kind=link}

{kind=link}