Weekly Insight 06/01

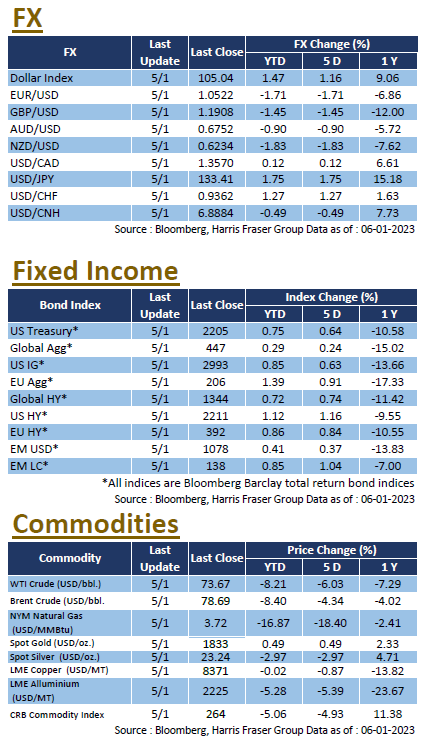

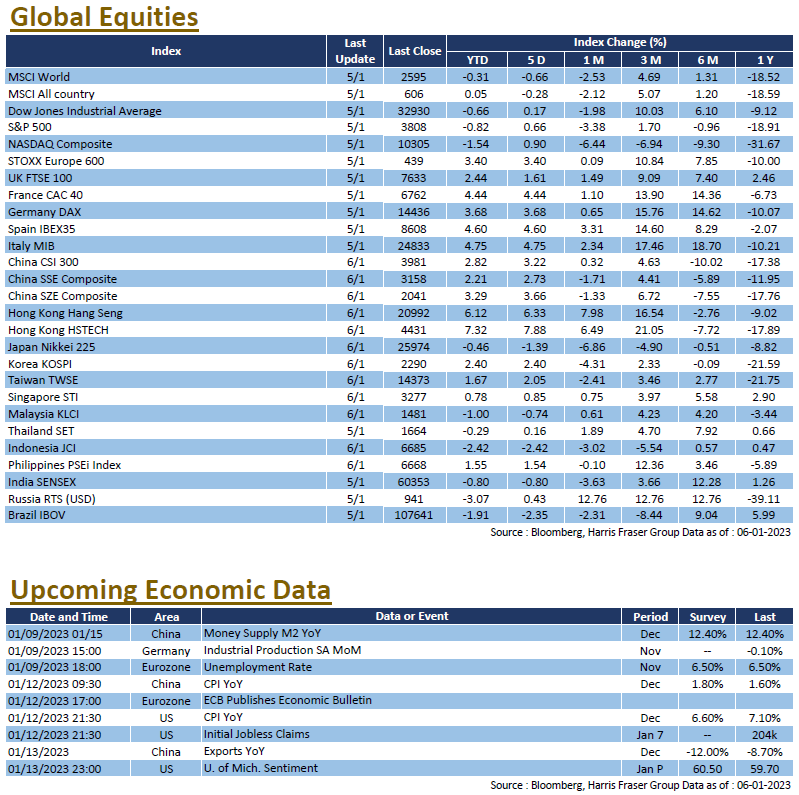

US markets got off to a relatively poor start to the year of 2023, as the 3 major indices lost 0.88-1.65% over the past 4 days ending Thursday. The US Fed released the December FOMC meeting minutes during the week, minutes reflected a clear message from Fed members, that inflation remains a concern, and dissented market’s monetary policy expectations. Fed members also spoke out during the week, St. Louis Fed President James Bullard struck a dovish tone, suggesting that rates are close to sufficiently restrictive. However, other members remained hawkish, Atlanta Fed President Raphael Bostic said that the Fed has more work to do, Kansas City Fed President Esther George suggested that interest rates should rise above 5% and stay at the level throughout 2023, Minneapolis Fed President Neel Kashkari even proposed that rates to rise as high as 5.4%. At the time of writing, markets still expect Fed Fund Rates to hit 5% in May, and rate cuts to take place in 2H 2023.

As for economic data, ISM manufacturing PMI in December was 48.4, which missed market expectations of 48.5, and was the second month of contraction in a row. Labour market data surprisingly tightened, both initial and continuing jobless claims came in lower than market estimates, ADP nonfarm employment change in December was 235K, which was significantly higher than the expected 150K, the data reignited worries over the labour market. In other news, the House Speaker election surpassed 10 rounds of voting without a result, which is the highest record since 1859. Next week, the US will be releasing more data including CPI figures and NFIB small business optimism index for December, University of Michigan Sentiment Index for January, as well as the latest labour market data on initial and continuing jobless claims.

Contrary to the US markets, European equities performed better off in the New Year, the French CAC and German DAX gained 2.59-2.86% over the past 5 days ending Thursday, while the UK FTSE also edged 1.61% higher over the past 4 days ending Thursday. Putin offered a 36 hour ceasefire for Orthodox Christmas, but the Ukrainian side offered no responses. On the other hand, the US and Germany have announced that they are sending additional armaments to Ukraine, including armored vehicles and Patriot missile systems. It remains to be seen if the conflict would extend throughout 2023. On the economy, final European PMIs in December were revised higher, while French and German CPIs both came in lower than markets expected. Next week, Eurozone will release the unemployment rates for November, both the UK and Germany will release their industrial production data for November, and the ECB will publish the latest Economic Bulletin.

China

China

The reopening continued in China, sentiment was lifted by the improvement in the economic prospects. Over the week, the CSI 300 Index gained 2.82%, while the Hang Seng Index surged 6.27%. It was reported that China is considering to reduce the huge investments on homegrown chips, while the PBOC reiterated that monetary will stay targeted this year to the economy, while maintaining economic stability and limiting price pressures. On the other hand, it was rumored that China might ease the ‘Three Red Lines’, and there are plans to ease liquidity stress for ‘systematically important’ developers, this was a dramatic shift in policy. As for the economy, Caixin Manufacturing PMI was 49 in December, which was higher than market expected, but was lower than the previous value. Caixin Services PMI on the other hand was 48 in December, which has improved from the 46.7 in November. Next week, China will be releasing December data on aggregate financing, new Yuan loans, and money supply M2, as well as CPI data and exports figures.