Weekly Insight 17/02

US

US

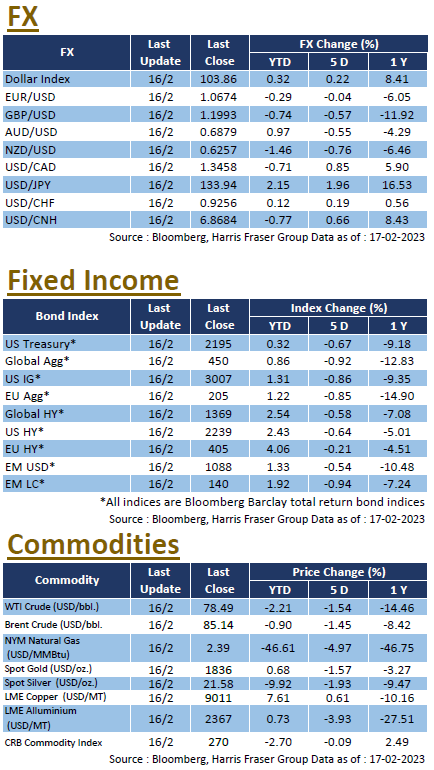

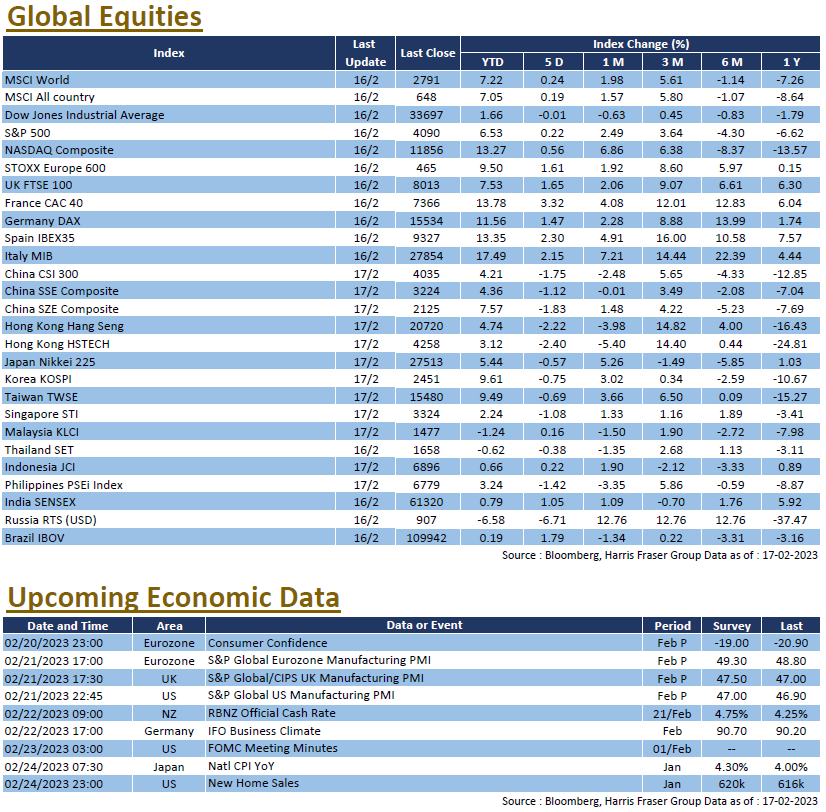

US equities continued to move sideways, markets gave up nearly all gains after the higher PPI came out on Thursday. Over the past 5 days ending Thursday, the Dow posted a slight loss of 0.01%, while the S&P 500 and NASDAQ edged 0.22-0.56% higher. PPI was 0.7% MoM in January, much higher than the market expected 0.4%. Fed hawks suggested that rate hikes could continue further after the data came out, Cleveland Fed President Loretta Mester said she supported a 50 bps hike back in the February meeting, and said the Fed still have more work to do. St. Louis Fed President James Bullard stated that he also opted for a 50 bps hike last meeting, and sees a case for a 50 bps hike in the March meeting. According to Bloomberg, interest rate futures shifted higher, markets has priced in some possibility for a larger hike in March, and expects Fed fund rates to hit the 5-5.25% range by May.

The earnings seasons nears its end, with 404 out of 500 S&P 500 index reporting at the time of writing, 71% of reporting constituents reported sales growth, with overall growth averaging at 5.4%. Earnings on the other hand was worse, with over 36% of members reporting an earnings contraction, and overall earnings came in at a 2.73% contraction on average. As for the economy, apart from the PPI surprise, the January CPI also came in higher than expected. Retail sales grew 3.0% MoM in January, higher than the expected 1.8%. Labour market remains mixed, continuing claims were higher than expected, while initial claims came in lower. Next week, the US will release the latest Markit PMIs for February, PCE data for January, alongside housing market data on new and existing home sales in January, as well as the usual labour market data on initial and continuing jobless claims. The Federal Reserve will also publish the FOMC meeting minutes for the February meeting.

Europe

Europe

European equities performance varied, but the rally continued. Over the past 5 days ending Thursday, the UK, French, and German equity indices gained 0.07-2.47%. The first economic bulletin for the year was released earlier, projecting that the Eurozone economy will grow by 0.9% in 2023, while inflation will be at 5.6%, the report also suggests that the economy might be more resilient than earlier estimates. ECB chief economist Philip Lane suggest that the effects of tightening have yet to hit the economy, and he estimates that the tightening has lowered Eurozone inflation by 1.2% for the year. As for the economy, the preliminary Q4 Eurozone GDP grew 0.1% QoQ. The UK CPI was 10.1% YoY in January, which was lower than market estimates of 10.3% and the previous month figure of 10.5%. UK retail sales in January also grew 0.5% MoM, beating estimates of a 0.3% contraction. Next week, the Eurozone and the UK will release the latest PMI figures for February, the European Commission will release the latest consumer confidence data for February, and Germany will publish the IFO business Climate in February.

China

China

With a lack of positive news, China and Hong Kong markets fell over the week, led by selloff in the tech sector. The CSI 300 index lost 1.75%, while the Hang Seng Index was down 2.22%. Ever since the balloon incident, Sino-US tensions has remained elevated, but US have showed the intention to mend relations, it was reported that US Secretary of State Anthony Blinken is planning to meet China State Councilor Wang Yi in Munich, US President Biden also indicated that he would like to speak to President Xi over the matter. In other news, it was reported that current Chairman of China Securities Regulatory Commission (CSRC) Yi Huiman will take over the role of the chairman of the China Banking and Insurance Regulatory Commission (CBIRC), while current Vice Mayor of Shanghai Wu Qing will be the new Chairman of the CSRC. Next week will be another one light week on Chinese economic data, the latest 1Y and 5Y Loan Prime Rate (LPR) will be announced, and the market expects rates to remain unchanged.