Weekly Insight 24/02

US

US

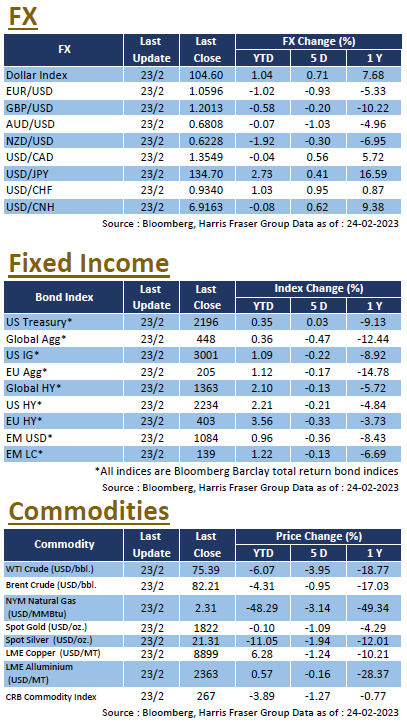

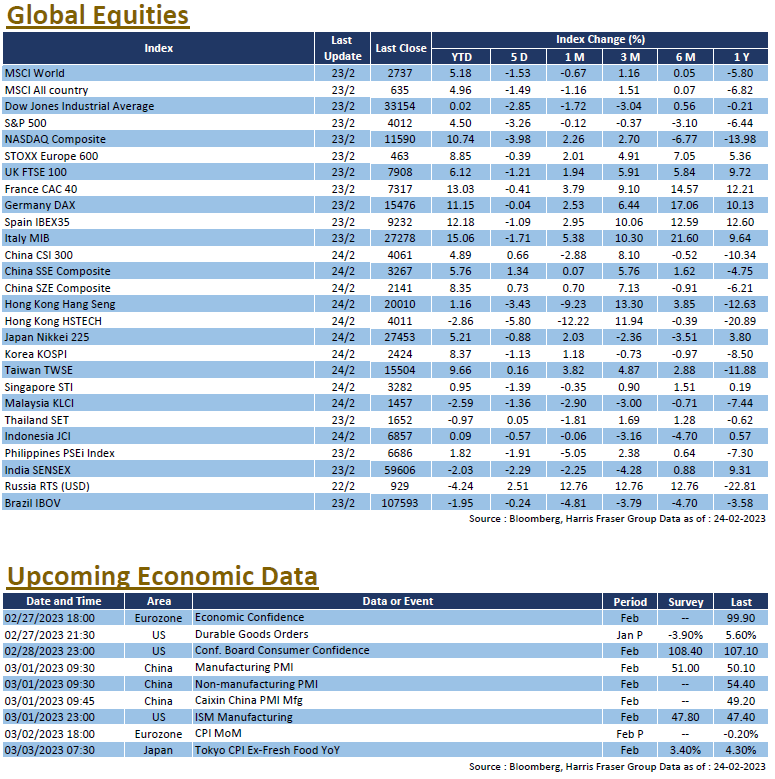

US markets had a shorter trading week due to holiday, but continued see further correction as concerns over the stronger than expected economy and the Fed’s monetary pathway weighted on markets. Over the past 4 days ending Thursday, the 3 major indices lost 1.61-2.24%. The US Fed published the February FOMC meeting minutes over the week, although most officials agreed to the 25 bps hike, a few members favoured a larger 50 bps hike. Minutes also showed that officials anticipate more rate hikes ahead to bring down inflation, the terminal rate could end up higher than earlier indications. At the time of writing, interest rate futures showed that markets expect 3 more hikes in the year, and rates will peak at 5.25-5.5% around July.

On the economy front, both the Markit PMIs in February have surprised to the upside. Markit services in particular surpassed the 50 mark, surpassing market expectations and the January figure, and was the first expansion since June last year. Labour market data echoed the positive business sentiment, with both initial and continuing jobless claims coming in lower than both market estimates and the previous figure. With the labour market still red hot, concerns over inflation and further monetary tightening will likely linger. Next week, the US will be releasing ISM manufacturing and services indices for February, Conference Board Consumer Confidence index for February, as well as durable goods orders for January. The usual high frequency labour market data on initial and continuing claims will also be published.

Europe

Europe

European equities also followed global markets and fell over the week on weaker market sentiment. Over the past 5 days ending Thursday, the UK, French, and German indices lost 0.37-1.31%. The final core CPI in Eurozone has been revised higher to a new historic high, markets are now pricing in close to 5 more rate hikes from the ECB for the year. However, Bank of France Governor Francois Villeroy de Galhau pushed back on the notion that ECB is committed to raising interest rates, suggesting that interest rates in Europe are already at a restrictive level. On the economy, Germany IFO business Climate in February was 91.1, which was slightly lower than market expected. Eurozone consumer confidence was -19, in line with market expectations. Eurozone PMI on the other hand was mixed, services PMI in February was 53, much better than the expected 51, manufacturing PMI on the other hand came in lower than expected and remained in the contraction zone. Next week, the Eurozone and member countries will be releasing the CPI data for February, while the European Commission will also publish the economic confidence for February.

China

China

Hong Kong and China equities had a mixed week, the CSI 300 index posted a slight gain of 0.66%, while the Hang Seng Index lost 3.43%. Chinese recovery seems to be on track, as traffic congestion index hits a new high since the start of 2022. President Xi also reiterated the goals to support economic growth, and the China Securities Regulatory Commission announced a pilot scheme that PE funds can invest in property projects, in bids to further improve liquidity in the still struggling property sector. On foreign affairs, China State Councilor Wang Yi visited Moscow and met Russia President Vladimir Putin, while earlier talks between Wang and US Secretary of State Anthony Blinken in Munich turned sour, with the US warns China against providing lethal aid to Russia. Next week, China will release the latest NBS manufacturing and non-manufacturing PMIs, alongside the Caixin manufacturing and services PMIs.