Weekly Insight 17/03

US

US

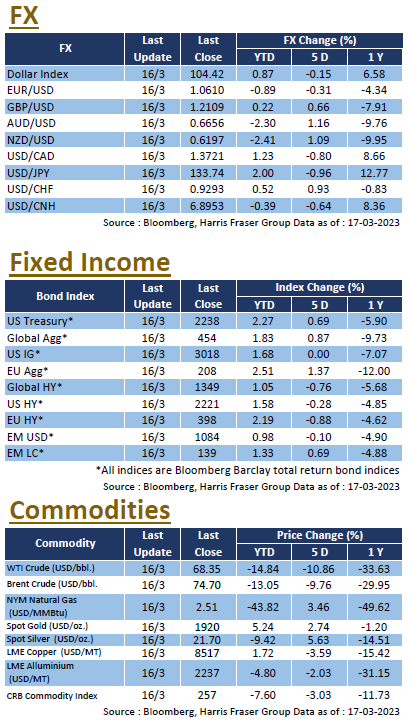

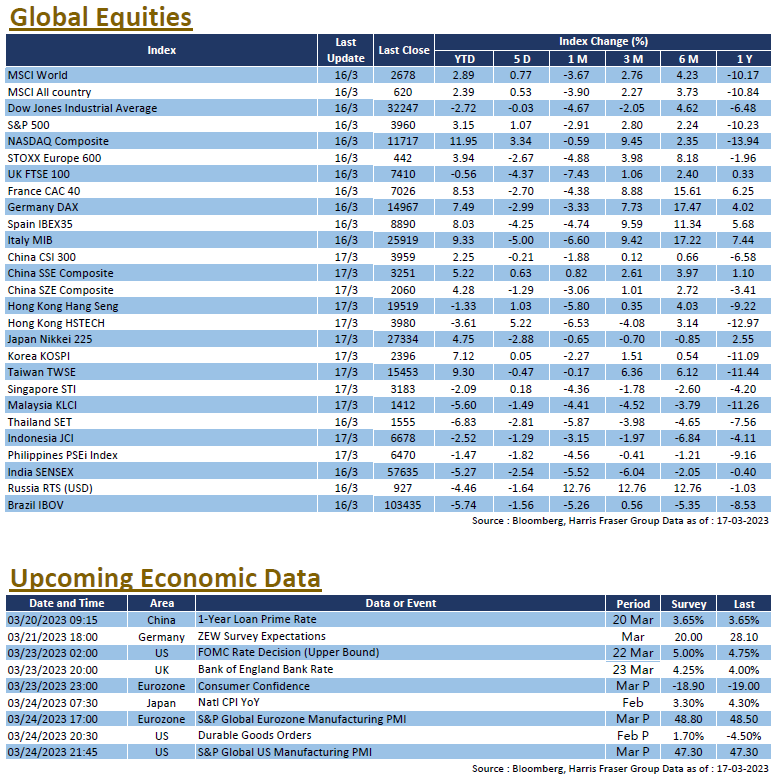

Market confidence faltered at the start of the week, but later regained as the Treasury and Fed provided guarantee and support to markets. Over the past 5 days ending Thursday, the Dow dipped 0.03%, while the S&P 500 and NASDAQ gained 1.07% and 3.34% respectively. The Silicon Valley Bank fell into FDIC receivership after a bank run, raising concerns that other regional banks might meet the same fate. Later in the week, it was reported that First Republic will receive funding from the large banks to relieve the liquidity stress, potentially bringing an end to the biggest financial confidence crisis in the US since 2008. The failure of SVB also raised speculation on the Fed’s monetary path for the year, market had diverged opinion on the monetary implications, interest rate futures showed that markets are on the fence over whether the Fed will hike 25 bps in the March meeting, and futures are now pricing in the possibility of rate cuts before the end of the year.

As for the economy, the important CPI data fell largely in line with market expectations, headline CPI in February was 6.0% YoY, core CPI was 5.5% YoY; the core CPI MoM figure was 0.5%, which is slightly higher than the market expected 0.4%. NFIB business optimism improved to 90.9 in February, though retail sales fell 0.4% MoM, which was a larger contraction than the expected 0.3% fall, after the upward revision of the January figure from 3.0% to 3.2%. As for the labour market, both initial and continuing jobless claims came in lower than market expectations, suggesting that the complete easing of the labour market is still not here yet. Next week, the US will be releasing the March data on Markit manufacturing and services PMIs, durable goods orders for February, alongside February housing market data on new and existing homes sales. The usual labour market data on initial and continuing jobless claims will also be a market focus. The US Fed will also hold their March FOMC meeting.

Europe

Europe

Concerns over risk contagion in the banking sector spread to Europe, European equities came under pressure and investing sentiment deteriorated. Over the past 5 days ending Thursday, the UK, French, and German equity indices lost 3.97-5.96%. Concerns over Credit Suisse grew later in the week, CDS and bond spreads for Credit Suisse widened to default levels, and despite the open support from Swiss National Bank and regulator that CS will receive liquidity support if needed, prices remain depressed. Markets will continue be lookout for contagion risk in the market. Despite the turmoil in the markets, the ECB also went ahead with their earlier promise of a 50 bps hike in the March meeting, citing that inflation is ‘projected to remain too high for too long’. ECB President Christine Lagarde stated that the Bank has the tools to contain the situation in the banking sector, and showed their continued determination to fight inflation. However, the Bank did not offer forward guidance, citing that future decisions will depends on upcoming economic data. Next week, Eurozone will be releasing the Markit PMIs for March, as well as the Consumer Confidence data for March, Germany will release the latest ZEW survey expectations and sentiment. The Bank of England will also announce the latest monetary decision.

China

China

Hong Kong and China equities had a relatively flat week, although the global bank rout hurt market sentiment. Over the week, the CSI 300 index was down 0.21%, while the Hang Seng Index was 1.03% higher. On geopolitics, US national security adviser Jake Sullivan mentioned that US President Joe Biden is expected to talk to President Xi, while Xi will visit Russia on a State visit over 20-22 March. China and Ukraine Foreign ministers talked over the phone, and Xi will also speak with Ukraine President Zelensky after the Russia trip. As for the economy, fixed asset investment grew 5.5% YoY in February, beating market expectations, retail sales 3.5% higher YoY in the month were in line with estimates, while industrial production growth of 2.4% YoY fell short of the market expected 2.6%, home prices also posted a gain for the first time in 18 months. Next week will once again be a quiet week for Chinese data, with the latest 1 and 5 year Loan Prime Rates (LPR) to be announced, markets expect the rates to remain unchanged.