Weekly Insight February 5

U.S.

U.S.

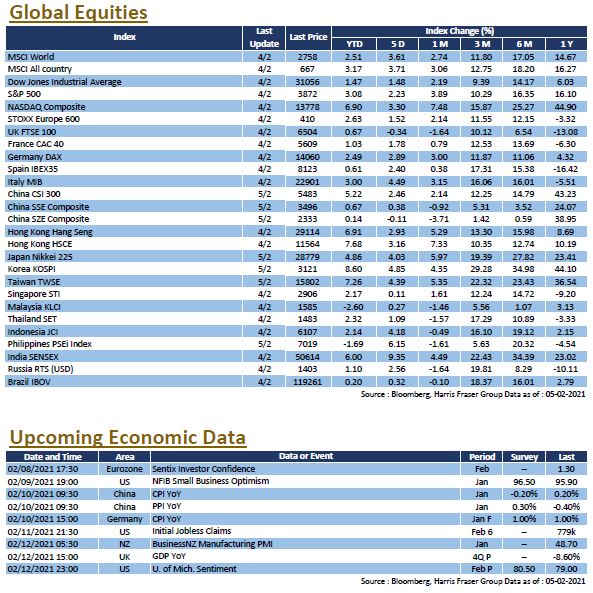

The US stock market continued to improve on the back of positive economic data and corporate earnings, the three major equity indexes rose 1.48% - 3.30% over the past five days ending Thursday. The January Markit Manufacturing PMI was 59.2, which was the highest on record, while the ISM Services Index also rose to 58.7 in January, which itself was a two-year high. The latest corporate earnings reports were also encouraging, with over 80% of the 283 reporting companies beating market expectations, including Amazon's fourth quarter results, which saw revenues top US$100 billion, after which Bezos announced his resignation as Group Chief Executive. The silver and GameStop stocks, which had been the focus of retail investors, fell across the board, with interest shifting to other stocks such as small cap pharmaceuticals. Next week, the US will release the NFIB Small Business Confidence Index for January and the preliminary University of Michigan Market Sentiment for February.

Europe

Europe

Rumours that former ECB chief Mario Draghi may become Italy's new prime minister have fuelled speculation that a new Italian government will be set up soon, clearing up political uncertainties and boosting European equities. Italian, German, and French equity indexes were up 4.49%, 2.89% and 1.78% respectively over the past 5 days ending Thursday, whereas UK equities edged down 0.34%. The Bank of England kept monetary policy unchanged, and expressed optimism over the economic outlook, noting that the vaccine programme should drive a rapid rebound in the economy, the Bank further added that it would be prepared for negative interest rates, but the radical policy would not be implemented in the next six months. Next week, the Eurozone will release the Sentix Investor Confidence Index for February.

China

China

Hong Kong stocks were volatile this week, but still posted a decent gain. Recent IPOs such as Kuaishou sparked a frenzy in the market, but the slowing down of Southbound capital pressured parts of the stock market. Pressure on capital markets eased in the China A-share market, with the overnight SHIBOR falling from over 3%, and the market expects liquidity to remain accommodative before and after the Chinese New Year, the CSI 300 Index rose 2.46% for the week. Kuaishou was listed on Friday and opened at HK$338, representing a 194% gain. However, it should be noted that from February 9 onwards, southbound trading via Hong Kong Stock Connect will be suspended, meaning there will be no Southbound capital. As for corporate earnings, Alibaba shares rebounded after Alibaba's Q3 revenue beat expectations and its 33%-owned Ant Group reached an agreement with regulators, suggesting a green light for its future IPO. Next week, China will release CPI and PPI data for January.