Weekly Insight July 2

US

US

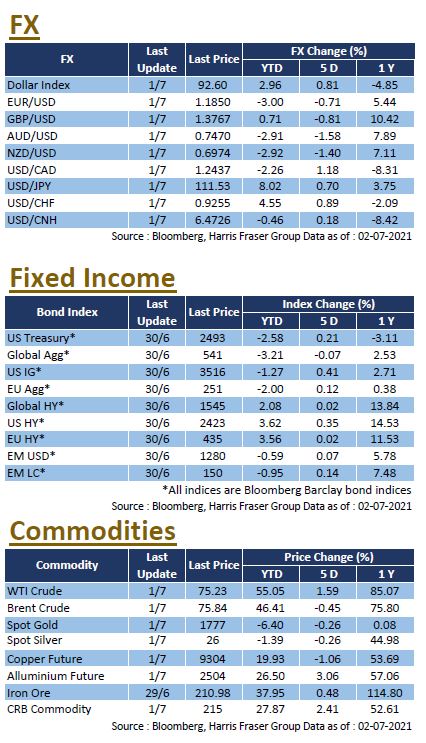

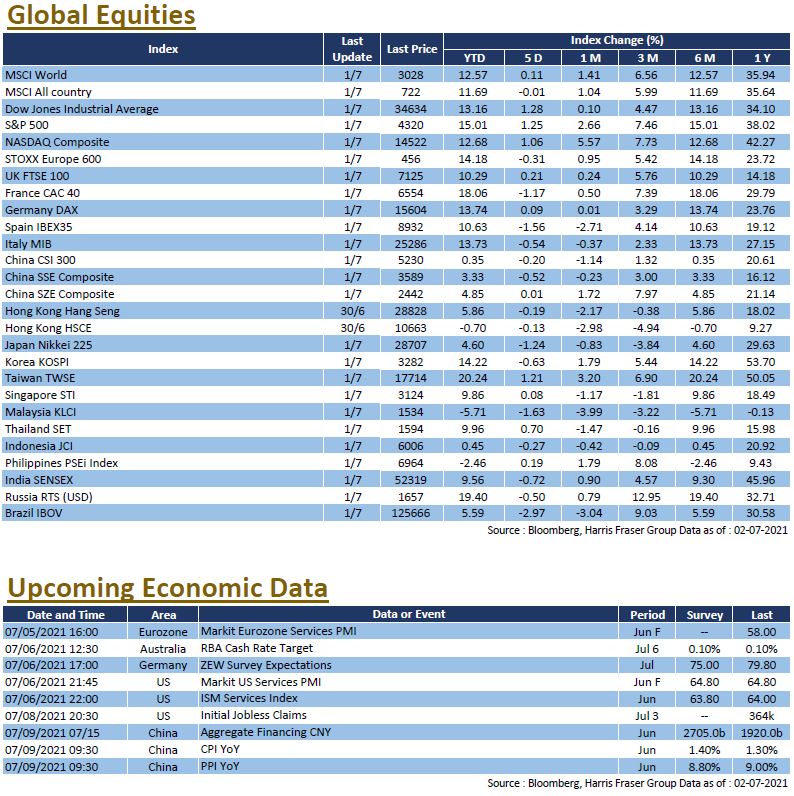

US equities stayed in strong form, as concerns over the risk of rate hikes and tapering has temporarily faded, positive economic data further supported markets. Over the past 5 days ending Thursday, US markets went higher, the 3 major equity indices gained 1.06 – 1.28%, the S&P 500 Index in particular set new historic highs for 6 days in a row. Policy wise, the bipartisan infrastructure bill has hit another obstacle, as Republican senators warned that they could withdraw their support for the bipartisan deal if it was bundled with another Democratic bill. Economic data were great, initial jobless claims went below 400k again, hitting a new low since the start of the epidemic. ISM manufacturing PMI fell slightly short of market expectations, but remains in the expansionary zone, consumer confidence also hit a recent high, both highlighting the strength of the current economy. As for monetary policies, Philadelphia Fed Chairman Patrick Harker said the reduction in asset purchases should start within this year, joining in with the growing hawkish sentiment in the Fed. Next week, services PMI from both ISM and Markit will be released, investors might also want to keep an eye out for the latest employment data, while the Fed will release the June FOMC meeting minutes.

Europe

Europe

European equities had mixed performance amidst decent economic data, the UK and German equity indices gained 0.09 - 0.21% over the past 5 days ending Thursday, while French equities lost 1.17% over the same period. Although vaccinations programmes continued, COVID infections in the UK due to the Delta variant are on the rise, which could risk spreading it across the continent with the ongoing UEFA EURO 2020, potentially jeopardising the whole reopening process. Apart from the risk arising from the epidemic, Europe fundamentals remained on the bright side, with various employment, sentiment, and more importantly inflationary data staying on the positive side. The latest figure on inflation came in at 1.9%, which is slightly lower than the previous figure of 2.0%, relieving markets over inflation concerns, and indirectly guaranteeing that the current easy monetary policy can be extended. Next week, Europe will release a range of key economic data, including services PMIs and retails sales figures, while Germany will have further data on ZEW Survey Expectations and industrial production.

China

China

With a larger correction on Friday, Chinese equity markets underperformed, the CSI 300 index lost 3.03% over the week; Hong Kong markets also felt the impact, falling 1.98% over the past 5 trading days ending Friday. As for fundamentals, economic data in China was less positive than markets had hoped, with both the official PMIs and the Caixin manufacturing PMI lower than the previous reading. The Chinese Communist Party celebrated its 100th anniversary, marking the end of the first centenary, and moving on to the second centenary, which aims to transform China into a modern world power. Markets continued to pay attention to the offshore corporate bond markets, with the recently downgraded Evergrande and Huarong in focus. Next week, China will release more economic data, including Caixin services PMI, CPI, and PPI figures for June.