Weekly Insight August 6

US

US

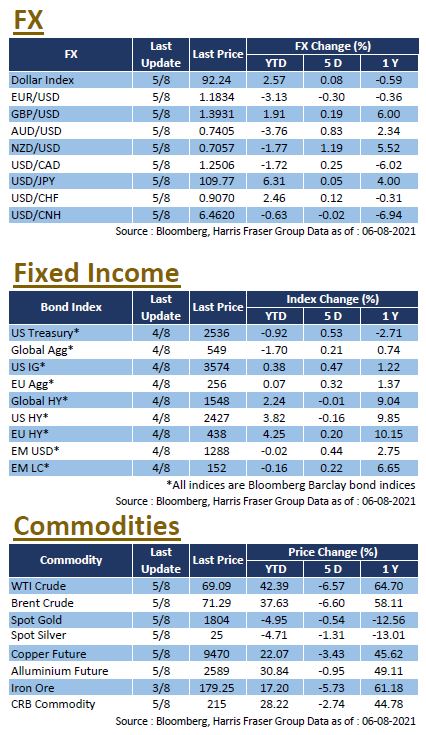

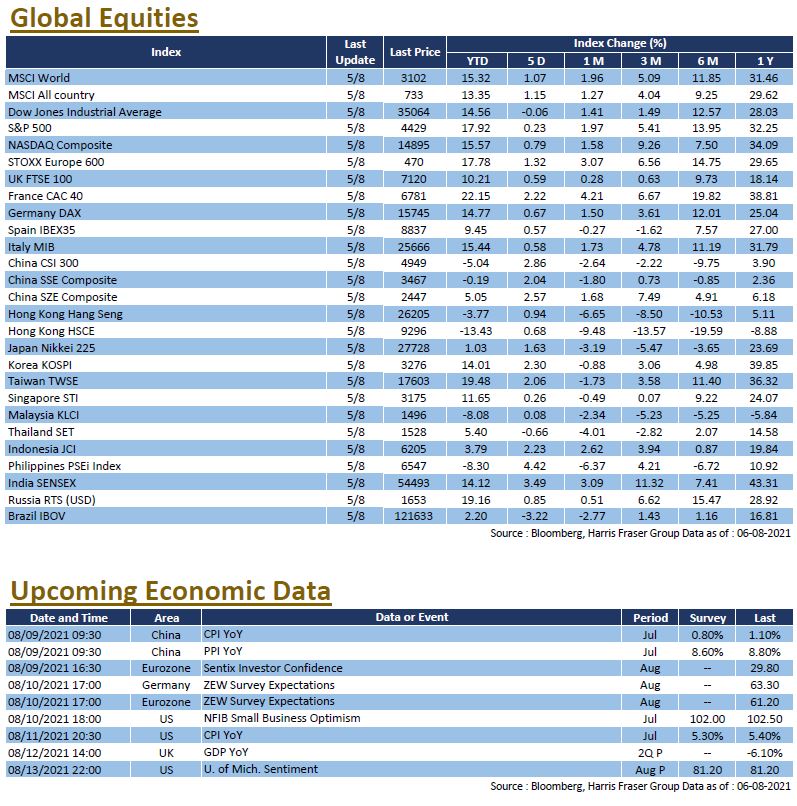

The Delta variant continues to rage across the globe, threatening the recovery outlook, but strong US earnings have negated worries over the outbreak, with the S&P 500 and Nasdaq up 0.23% and 0.79% respectively over the past five days ending Thursday, both reaching new record highs, while the Dow was down a modest 0.06%. Thus far, about 85.6% of the 439 reporting S&P 500 companies have reported market beats, reflecting a strong overall business conditions. Economic data has been slightly disappointing, the ISM Manufacturing Index slowed in July, mainly due to supply bottlenecks which limited output.

While the spread of the Delta variant posed a potential concern over slowing economic growth, global central bank monetary policies are leaning towards the hawkish side. US Federal Reserve Governor Christopher Waller said he was optimistic about the economic outlook and expects the Fed to scale back its monetary easing earlier. Vice-Chairman Richard Clarida also suggested that a tapering of bond purchases would be announced at a later date, followed by an interest rate hike for the first time in 2023. Incidentally, Brazil's central bank has already announced the largest rates hike since 2003. Next week, the US will release data on July CPI and University of Michigan market sentiment for August.

Europe

Europe

A strong recovery in the Eurozone boosted European markets, with UK, French, and German indices rising between 1.25% and 2.55% over the past five days ending Thursday. 2021 Q2 Eurozone GDP rose by 2.0% QoQ, well above market projections of 1.5%, while the final Eurozone manufacturing PMI for July was 62.8, also above expectations of 62.6. While the Bank of England kept interest rates and policy unchanged after the interest rate meeting, the Bank stated that it would start tapering when the bank rate reaches 0.5%. Next week, the Eurozone will release its ZEW survey expectations and Sentix investor confidence data for August.

China

China

A strong recovery in the Eurozone boosted European markets, with UK, French, and German indices rising between 1.25% and 2.55% over the past five days ending Thursday. 2021 Q2 Eurozone GDP rose by 2.0% QoQ, well above market projections of 1.5%, while the final Eurozone manufacturing PMI for July was 62.8, also above expectations of 62.6. While the Bank of England kept interest rates and policy unchanged after the interest rate meeting, the Bank stated that it would start tapering when the bank rate reaches 0.5%. Next week, the Eurozone will release its ZEW survey expectations and Sentix investor confidence data for August.