Weekly Insight September 9

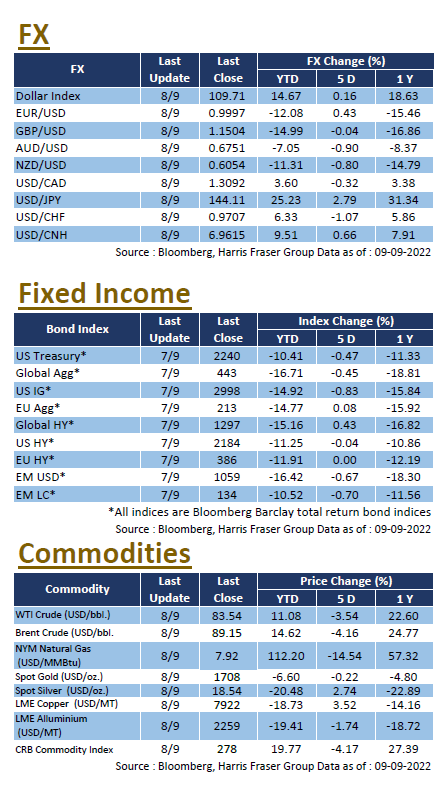

Economic data diverged, market volatility continued over the week, but US equities did somewhat stabilise after the recent drawdown. Over the past 5 days ending Thursday, the 3 major indices were 0.39-1.29% higher. US Fed president Jerome Powell reiterated the Fed’s determination to act against inflation, citing the experience of persistent inflation in the 70s and 80s showed the need for Fed action, Powell also mentioned the tight labour market as another point of concern. Many firms are now predicting a 75 bps rate hike in the September interest rate meeting, which is echoed by the market, as Bloomberg interest rate futures currently imply roughly 80% chance for a 75 bps hike at the time of writing.

According to the latest economic Beige Book released by the Fed this week, the labour market stays very tight, wages are rising, and price levels remains elevated, although most aspects have showed some degree of easing, the report also noted weakness in the residential real estate market. In other news, OPEC+ held a meeting on 5th September, announcing a cut of 100,000 barrels per day in October, citing concerns over China demand and the Iran deal. For economic fundamentals, the final Markit Services PMI for August was further revised downwards to 43.7 from the preliminary figure of 44.3, while the final ISM Services PMI in August was revised up to 56.9 from 55.1, reflecting further divergences amongst corporations. Next week, the US will release the CPI, PPI, and retail sales figures for August, as well as the University of Michigan Sentiment Index for September.

Following the earlier correction, European markets slightly rebounded, with the UK, French, and German indices gaining 1.52-2.17% over the past 5 days ending Thursday. The European Central Bank (ECB) held its interest rate meeting on Thursday, announcing a rate hike of 75bps, which was the largest single rate hike since the formation of the Bank. After the meeting, ECB president Christine Largarde suggested that more rate hikes are on the way, but reassured that the 75 bps hike will not be the norm. In the UK, Queen Elizabeth II has passed away on Thursday at the age of 96, after appointing Liz Truss as the new Prime Minister on Tuesday. Nord Stream 1 have yet to resume operations after Russia announced maintenance earlier, energy security in the region remains as a main concern for investors. As for economic fundamentals, the final services PMI in the Eurozone was revised down to 49.8, missing market expectations and entering contraction zone for the first time since March 2021. Next week, the Bank of England will hold its interest rate meeting, the UK will release its August retail sales data, while Eurozone will publish the ZEW survey expectations for September.

China

China

Over the week, the Hang Seng Index fell by 0.31% while the CSI 300 Index rose by 1.74%, the overall market sentiment remains under pressure. The Chinese government is actively providing impetus to the economy. During the State Council meeting on Wednesday, Premier Li Keqiang announced policies to support employment and entrepreneurship, as well as supporting the platform economy. However, markets remain on the side-lines before solid economic data is observed. On the economic front, Chinese CPI and PPI both came in lower than expected, August exports saw a mere 7.1% growth YoY, which was much lower than the market expected 12.8% and the previous month’s figure of 18.0%. In particular, Chinese exports to the US recorded the first YoY contraction since August 2020; though Caixin Services index for August came in at 55.0, which was better than market expected. Next week, China will be releasing the August data on fixed asset investment, industrial production, and retail sales.