Weekly Insight September 16

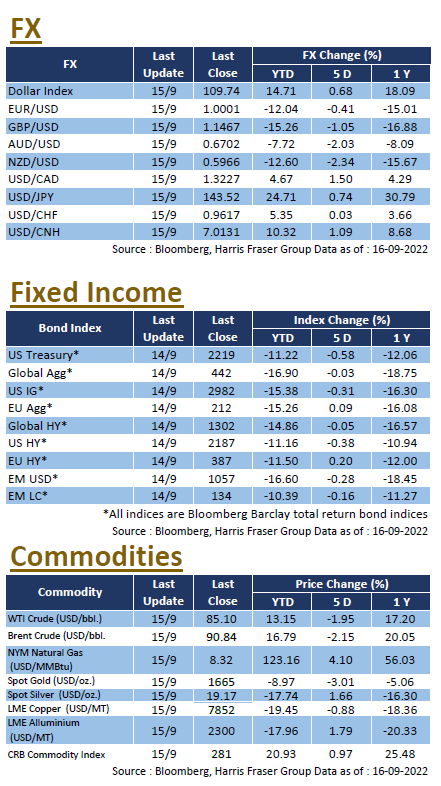

The much anticipated inflation print came out stronger than expected, reinforcing expectations of a larger rate hike in the next Fed interest rate meeting, sending US equities lower for the week. Over the past 5 days ending Thursday, the 3 major indices were 2.56-2.62% lower. The World Bank warned on Thursday that the global economy is heading towards a recession, as global central banks ‘simultaneously hike interest rates’ due to inflation. However, the Bank suggested that even at the current trajectory of rate hikes, it would be insufficient to bring the global core inflation back to the targeted level, suggesting that central banks might have to raise interest rates by another 2% to achieve their goal.

On the economic front, August CPI came in at 8.3% YoY, higher than the market expected 8.1%, and also logged a 0.1% gain MoM, surpassing expectations of a 0.1% contraction. The PPI in August on the other hand was 8.7%, which was both below the market expected 8.8% and July’s 9.8%. The Core PPI though was 0.4% MoM, suggesting that inflation is still not out of the window yet. Retail sales were also strong, with a 0.3% MoM growth in August, beating both market expectations and the previous month figure. More importantly, the labour market remains tight, with both initial jobless claims and continuing jobless claims lower than expected. It remains to be seen whether there will be continued easing in prices. Next week, the US will release the Markit manufacturing and services PMI, while the Fed will also hold the September interest rate meeting.

European equities retreated later in the week as the prospect of further monetary tightening emerged. Over the past 5 days ending Thursday, the UK, French, and German indices only edged 0.28-0.52%. ECB board member Isabel Schnabel reiterated that the Bank will be further raising interest rates to ensure inflation returns to the medium term target level of 2% in a timely manner. ECB Vice-President Luis de Guindos acknowledged that the European economy is slowing, but emphasised that monetary policy must be focused on price stability, and the Bank is determined to keep inflation expectations anchored. The European Commission proposed an emergency intervention to control electricity prices, but left out price caps on nautral gas, Dutch TTF Gas Futures remain in the 200 Euro range. On the Economic front, German ZEW economic sentiment fell to -61.9, missing expectations of -60 and the previous month figure of -55.3. The UK August CPI came in at 9.9% YoY, surprisingly lower than market consensus of 10.2% and the July figure of 10.1%. Next week, the Eurozone manufacturing and services PMIs will be released. The Bank of England will also hold its September interest rate meeting on 22nd September after delaying it due to Queen Elizabeth II’s death.

China

China

Although August economic data have showed some signs of life, both China and Hong Kong equities remained under pressure over the week, with the CSI 300 Index down by 2.60%, and the Hang Seng Index losing 0.49%. Due to COVID restrictions, domestic tourism was hit over the Mid-Autumn Festival, tourism revenue is 22.8% lower. As for the FX, the US Dollar to Chinese Yuan broke through the 7 mark for the first time in over 2 years. President Xi Jinping made his first state visit in more than 2 years, and attended the Shanghai Cooperation Organisation Summit, meeting Russian President Vladimir Putin there. In other news, SEC Chairman Gary Gensler mentioned that inspectors from the Public Company Accounting Oversight board will fly to Hong Kong, and start the review on Chinese companies listed in the US on Monday onwards. Chinese economic data released this week were decent, with fixed investment, industrial production, and retail sales all better than markets expected. Next week, China will release the latest 1-Year Loan Prime Rate.