Weekly Insight January 15

U.S.

U.S.

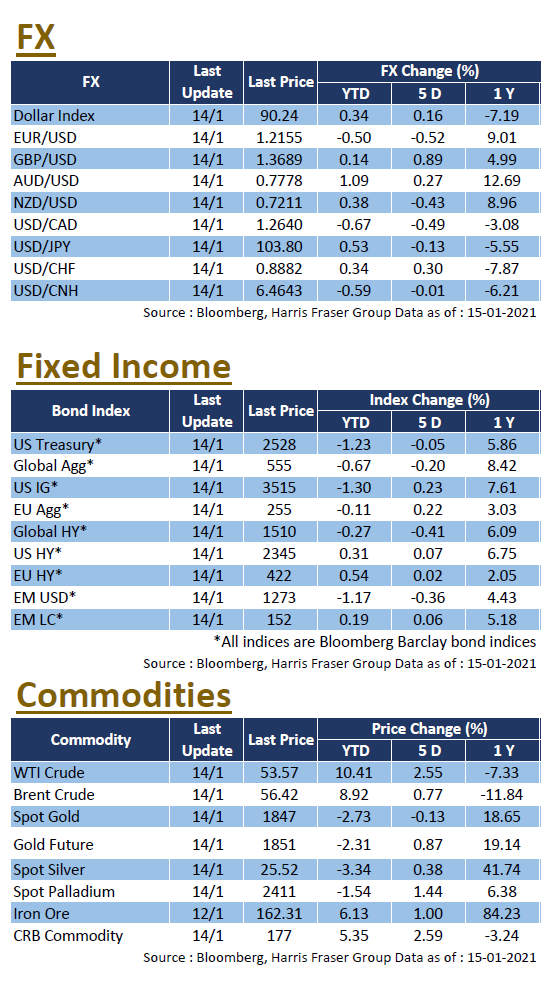

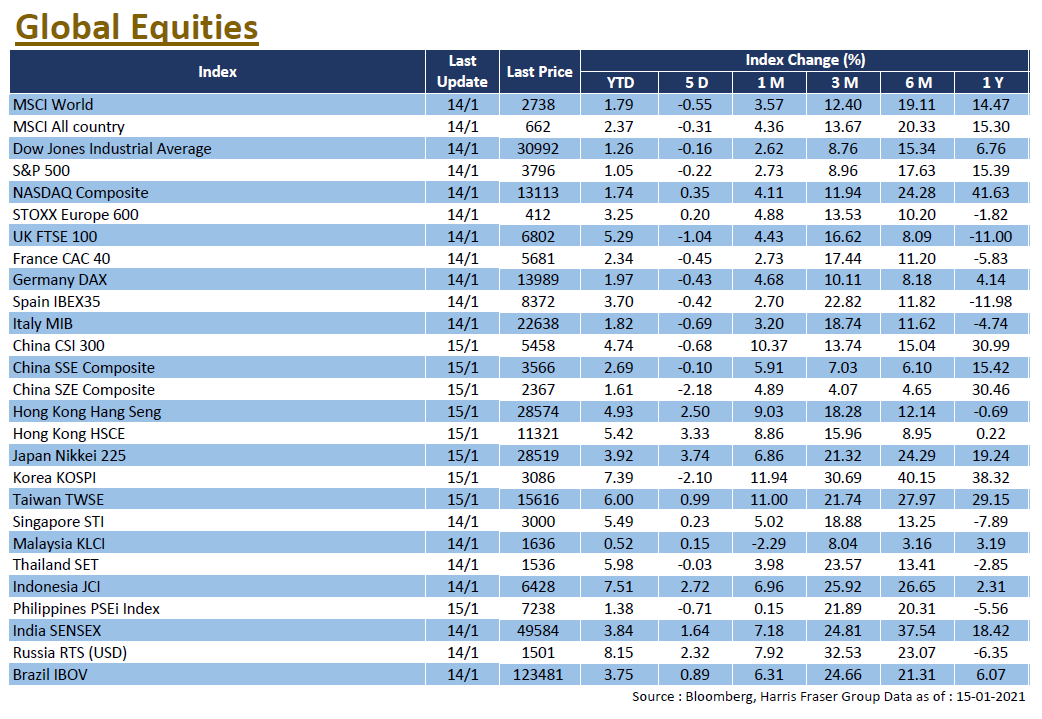

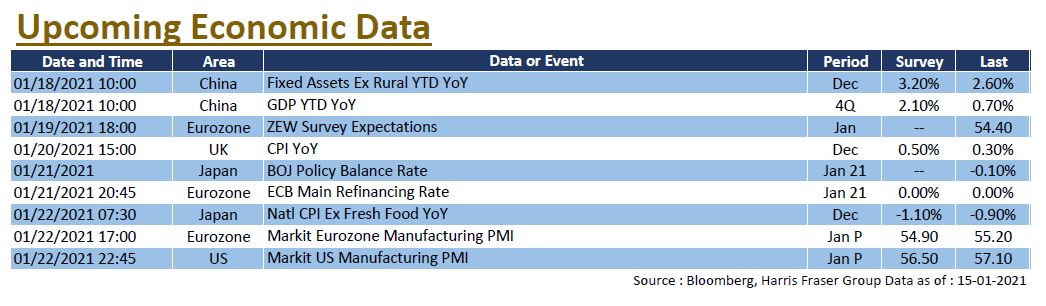

US stocks have not seen major movements over the past week, the three major equity indices ranged from -0.16% to +0.35% over the past five days ending Thursday. The news that caught the market's attention was the impeachment against Trump, which was reportedly supported by Senate Republican Leader Mitch McConnell. If the motion proceeds to the Senate, it would be the first time in history that an impeachment trial would extend beyond the presidency. In other news, US President-elect Joe Biden unveiled a US$1.9 trillion economic relief package, which should be followed by a package focusing on longer-term goals such as infrastructure and climate change. On the monetary policy front, Fed Chairman Jerome Powell said it is not time for an exit from easing, adding that interest rates will remain low for a longer period; the news put pressure on the US dollar. Next week, the US will release the Markit manufacturing and services figures for January.

Europe

Europe

European stocks were on a weak trend, with the UK, France, and Germany posting losses between 0.43% - 1.04% over the past 5 days ending Thursday. The epidemic remains serious in Europe, with Germany's total cases topping 2 million as of Thursday. Chancellor Angela Merkel wants to tighten measures to fight the epidemic, but German companies are closing down due to the epidemic, the country's economy has shrunk by 5% YoY in 2020. The minutes of last month's European Central Bank (ECB) interest rate meeting showed that members were divided over the monetary policy direction, and the market was wondering if the ECB would be able to implement an effective long term policy. On the other hand, Italy faces another political crisis, as former Prime Minister Renzi's withdrawal from the ruling coalition rattled the market and put the ruling coalition at risk of collapse. Next week, the ECB will hold its interest rate meeting, while the Eurozone will release its manufacturing PMI and ZEW economic forecast data.

China

China

Hong Kong stocks had a strong week, with the Hang Seng Index rising 2.5% over the period and 4.93% year-to-date. As for the China A-share market, the CSI 300 Index fell slightly by 0.68% over the week, but still managed to maintain a year-to-date gain of 4.74%. The US Department of Defence added 9 more Chinese companies to the list of military-related companies. Xiaomi, one of the companies on the list, saw its share price plunge by over 10% in a single day, while Alibaba and Tencent, both of which suffered from rumours earlier, managed to get away and rebounded. China's economic data showed improvement, with the PPI slowing in December and the CPI reversing the contraction seen last month. Next week, China is set to release its Q4 GDP and December's fixed investment, manufacturing and retail data.