Weekly Insight June 2

US

US

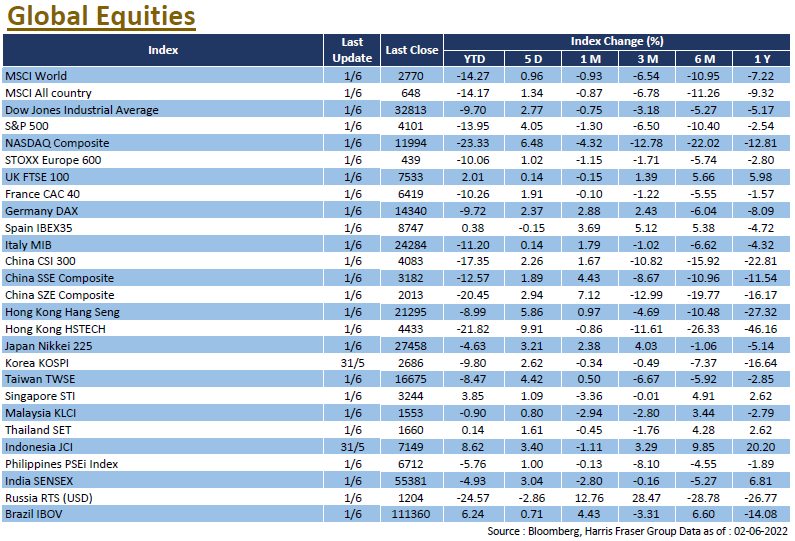

After the biggest weekly gain in a year and a half, US stocks fell in the last two days till Wednesday, mainly due to renewed concerns about the US economic outlook following the release of weak consumer confidence data. The US consumer confidence index fell further to a three-month low of 106.4 in May, with the market putting the blame on the ongoing high inflationary environment. The latest Federal Reserve Economic Beige Book showed a slowdown in the US economic growth momentum in the short term due to negative factors such as rising interest rates and inflation.

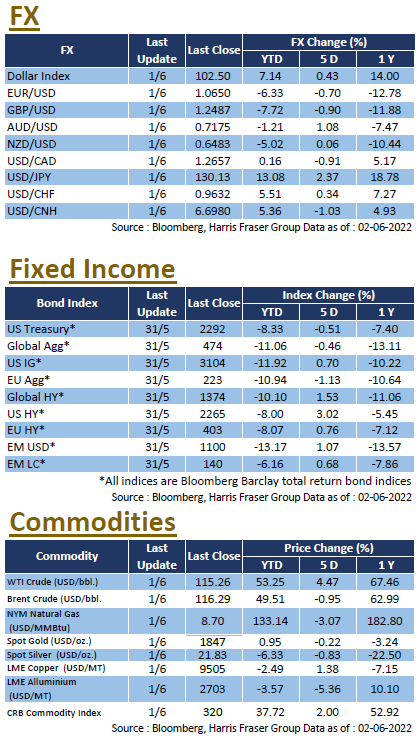

The economy and inflation figures will influence the US mid-term elections held at the end of this year. In a meeting between President Joe Biden and Fed Chairman Jerome Powell, Biden said that fighting inflation was the Fed's primary responsibility, but that the Fed's autonomy would be respected. Earlier, Treasury Secretary Janet Yellen also admitted that she had made a mistake in last year’s prediction that inflation would not be persistent. It was also reported that Biden's economic advisor indicated that the White House is considering lowering tariffs to help curb inflation, and the market will be pay attention to whether such a move will boost market sentiment. Next week, the US will release CPI for May and the University of Michigan Market Sentiment Index for June.

Europe

Europe

Compared to the US, the rebound in European equities was significantly weaker, with the UK, French, and German equities gaining no more than 1% over the past 5 days ending Wednesday. Europe is currently facing strong inflationary pressures, with the German CPI rising by a record 7.9% YoY in May, while Spanish inflation also accelerated unexpectedly. The surprising inflation data drove up market expectations of the ECB's rate hikes, and according to Bloomberg interest rate futures data, a rate hike in July is now a foregone conclusion. The ECB will hold an interest rate meeting on 9th June, but rate hikes are not expected at that meeting for now.

China

China

With the announcement of the full lifting of the Shanghai lockdown, the introduction of economic stabilisation measures, improved economic data and the rebound in external markets, both Hong Kong and China stocks rallied, with the Hang Seng Index rising by 4.8% over the past 5 days ending Thursday, whilst the Hang Seng Technology Index was up by 9.02% and the CSI 300 Index by 2.42% over the same period. The market was optimistic about the recovery, after Shanghai lifted COVID restrictions, with China's epidemic easing and new cases falling to double digits, together with supportive policies such as a cut in car purchase tax and an increase in policy bank credit lines. Although the official manufacturing index for May was 49.6, still slightly below the 50 mark, it was a notable improvement over the previous month's 46.0, and the market will be watching the trend closely. Next week, China will release May CPI and PPI data, as well as import and export data for May.