Weekly Insight August 12

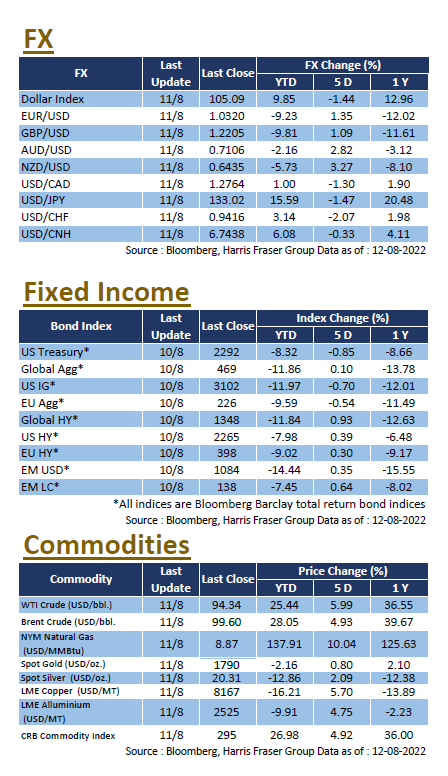

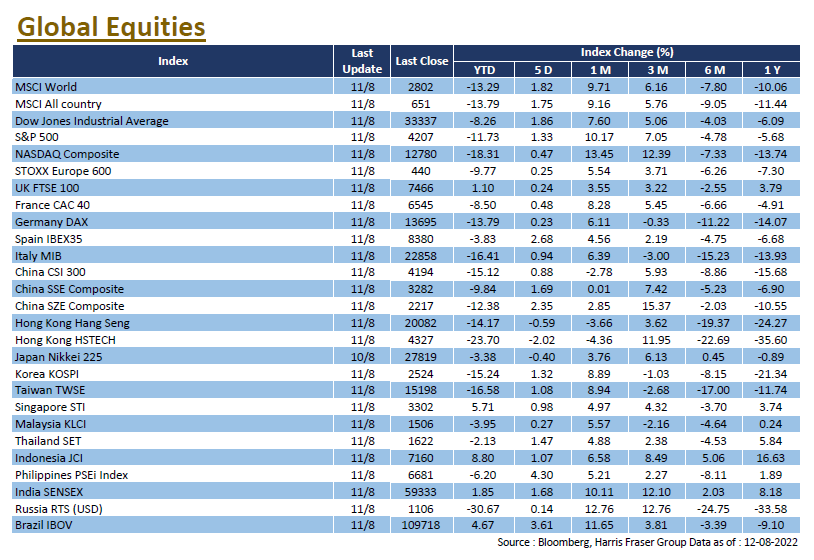

US markets remained resilient over the week, with the 3 major indices gaining 0.47-1.86% over the past 5 days ending Thursday. The CPI figure was the market’s key focus during the week, core CPI for July came in at 5.9% YoY, below the expected 6.1%; headline CPI for July also retreated to 8.5% YoY from 9.1% in June, and was lower than the market consensus of 8.7%. The milder than expected inflation figures was positive for markets and equities rose on Wednesday, as expectations for a milder pace of rate hike grew, improving the odds of a ‘soft landing’ for the economy.

However, contrary to market expectations, Fed members have been sending out more hawkish signals. Chicago Fed President Charles Evans said while inflation did slow down, it remains far too high and supported further tightening. San Francisco Fed President Mary Daly said it is too early to claim victory over inflation, mentioning that a 75bps hike is still on the table for the September meeting. Minneapolis Fed President Neel Kashkari mentioned that he still thinks a further 150 bps hike before the end of the year would be appropriate, and inflation would need to return to the 2% level even if it means recession. Next week, the US will release data on retail sales and industrial production, as well as the July FOMC meeting minutes.

European equities were relatively stable over the week, the UK, French, and German equities edged 0.23-0.48% higher over the past 5 days ending Thursday. UK’s Q2 GDP contracted by 0.1% QoQ, which could be the beginning of the anticipated year-long recession. Deputy governor of the Bank of England Dave Ramsden said the Bank would probably have to further raise rates with inflation in the UK expected to peak at 13% in October. On the data front, Sentix Investor Confidence was -25.2 for August, slightly improving from July’s figure of -26.4 but missed market expectations of -24.7. Next week, the German ZEW economic sentiment for August, UK CPI for July and unemployment for June will be released, the Eurozone will also publish their prelim Q2 GDP figures.

China

China

After the earlier tensions over the Taiwan Strait, both Hong Kong equities and China A-shares recovered this week, with the CSI 300 Index up 0.82%, while the Hang Seng Index is slightly down 0.13%. Troubles continue to emerge from the Chinese property sector, with Longfor Properties rumoured to have missed payments on commercial paper, which the company later denied. Economic data wise, inflation has slightly eased. CPI was 2.7% YoY in July, compared to the expected 2.9%; July PPI was 4.2% YoY, also lower than markets expected figure of 4.8%. Next week, figures on fixed asset investment, industrial production and retail sales are expected to be released.