Weekly Insight 10/02

US

US

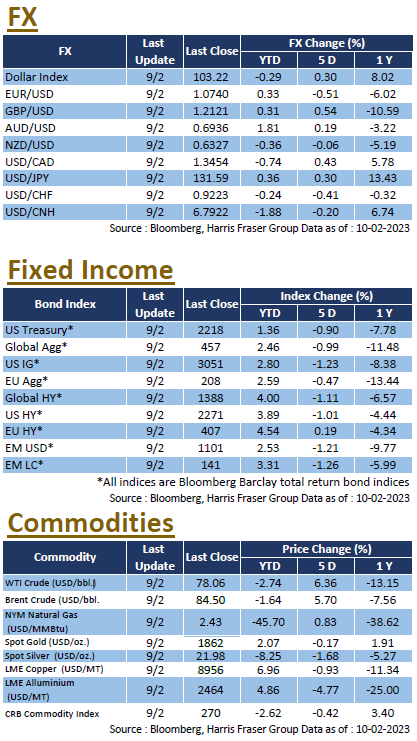

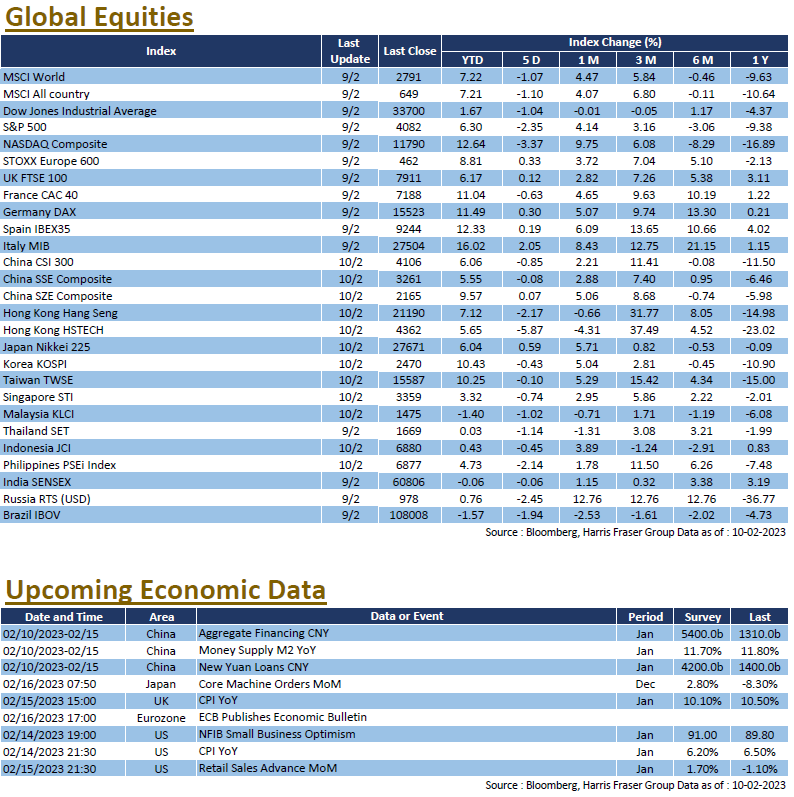

US equities faltered after hitting the highest level in the previous week, the 3 major equity indices lost 1.04-3.37% over the past 5 days ending Thursday. Concerns over the economy after the strong jobs data affected risk taking sentiment, the US 2 Year yields have risen to 4.5%, the highest level in more than 2 months, the inverted 10Y-2Y yield spread also widened to the highest level since the 80s. Fed President Jerome Powell agreed that the disinflationary process has begun, but suggested that more rate hikes could be needed than markets expect, and rates would be held restrictive for longer; Powell’s stance is further echoed by other Fed members throughout the week. At the time of writing however, Bloomberg interest rate futures data showed that markets are pricing in Fed Fund Rates to peak at 5-5.25% in Q2, and still expects rate cuts to take place within the year.

On the other hand, the earnings season continued with 343 of S&P 500 constituents reporting at the time of writing, only around 70% have posted earnings beat, and overall earnings growth was -2.68%, with over 35% of companies reporting lower earnings YoY. As for economic data, labour market data showed a slight change in direction, where initial and continuing jobless claims came in higher than market expected, and were both higher than the prior reading. Next week, the US will continue its release of economic data, including CPI and PPI data for January, NFIB small business optimism index, as well as sectorial data for January including housing starts, retails sales advance, and industrial production data. The usual labour market data on initial and continuing jobless claims will also be released.

Europe

Europe

European equities outperformed the global markets this week, the UK, French, and German equity indices were 0.09-1.16% higher over the past 5 days ending Thursday. ECB members continued to speak out during the week, with most of them calling for more rate hikes to keep monetary policy restrictive. At the time of writing however, interest rate futures have remained largely unchanged, pricing a higher probability of a 50 bps hike in the March meeting, and a 25 bps one in the May meeting. For the economy, Eurozone retail sales in December fell 2.8% YoY, which was lower than both the expected 2.7% fall and November’s 2.5% contraction. German industrial production in December also fell 3.1% MoM, significantly lower than the expected 0.7% contraction, while the German CPI in January was 8.7% higher YoY, lower than the market estimates of 8.9%, likely helped by the governmental subsidies. UK released their prelim Q4 GDP, which was flat in the last quarter, narrowly avoiding a technical recession. Next week, the ECB will publish the first Economic Bulletin for the year, the Eurozone will release the preliminary Q4 GDP figures, while the UK will publish the CPI and retail sales figures for January.

China

China

China and Hong Kong markets had a softer week as markets take a breather after the steep rally back in January. Over the week, the CSI 300 index was 0.85% lower, while the Hang Seng Index also lost 2.17%. Overnight funding costs in China were eased as the PBOC injected 1 trillion Yuan from 8th till 10th. On the geopolitics front, the balloon incident could possibly cause further strain to Sino-US relations, US Secretary of State Antony Blinken has cancelled his planned China trip, and the US House voted to condemn China over the incident. As for the economy, Chinese CPI was 2.1% YoY in January, which was still lower than the market expected 2.2%; the PPI on the other hand contracted 0.8% YoY in January, which was also lower than the market expected contraction of 0.5%. Both figures raise the expectations on the PBOC to further loosen monetary policy in the year. Next week, China will be releasing new Yuan loans, money supply M2, and aggregate financing data for January, as well as the 1 year Medium-Term Lending Facility (MLF) Rate.