Weekly Insight September 17

US

US

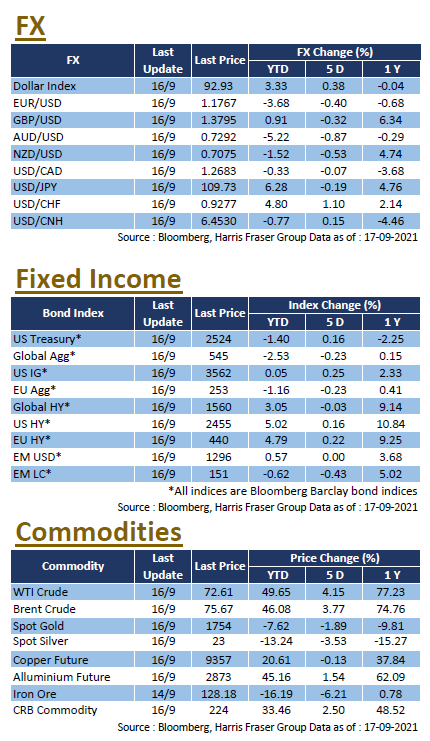

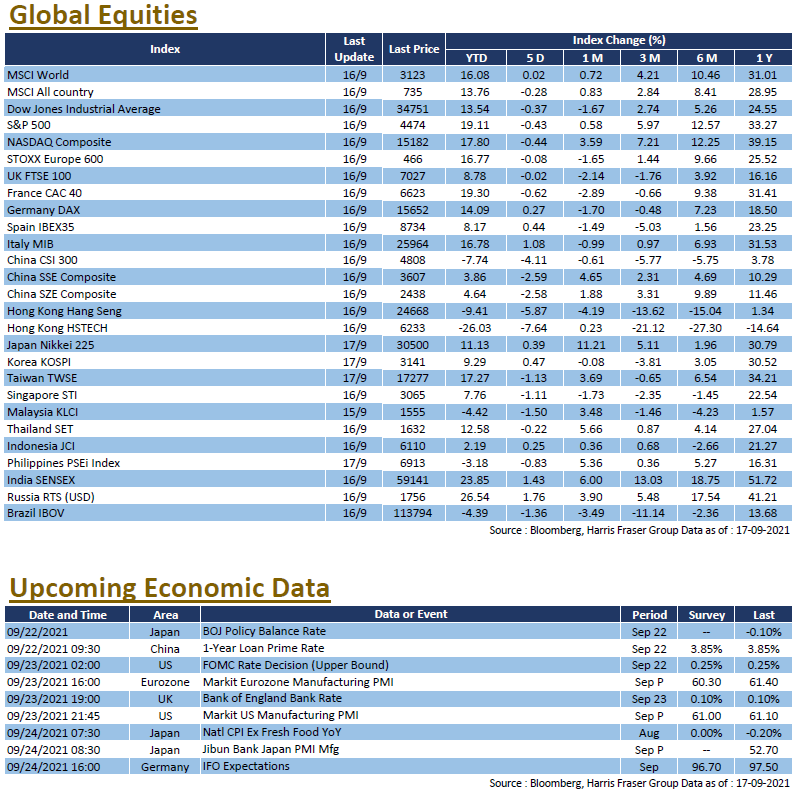

Retail sales rose unexpectedly MoM, reflecting a healthy consumption market. However, with the US debt ceiling crisis still in play, market sentiment weakened and US stocks softened, with the three major equity indices retreating between 0.37% and 0.44% over the past five days ending Thursday. August retail sales in the US rose 0.7% MoM, versus expectations of a 0.7% contraction, while CPI rose 0.3% MoM, the lowest increase in seven months and also fell below expectations, easing inflationary pressures and calmed market fears of persistently high inflation.

The US debt ceiling issue is on the horizon, but Senate Republicans are adamantly opposed to raising the ceiling; Treasury Secretary Janet Yellen has reached out to Senate Minority Leader Mitch McConnell for support, but has been turned down. J.P. Morgan said a technical default in the US could have a negative impact on the market. It is also reported that US House Democrats are drafting an increase in corporate taxes from 21% to 26.5%, which would be slightly lower than the 28% proposed by Biden earlier this year. Next week, the US Federal Reserve will hold a meeting on interest rates, whether Chairman Powell will announce the launch of the tapering of bond-purchases at the meeting or notwill be the focus of the market

Europe

Europe

European stocks have had mixed performance over the past five days ending Thursday. German equities were up 0.27%, French equities were down 0.62%, and UK equities were flat. The UK reported a 3.0% YoY rise in the August Consumer Price Index, the biggest increase in nine years, and the market is concerned about whether there will be any new policy announcements at the next Bank of England interest rate meeting. In addition, there are changes in the UK Cabinet, with Trade Secretary Liz Truss promoted to foreign secretary and Dominic Raab, former foreign secretary, was made justice minister, after drawing criticism over the withdrawal of troops from Afghanistan. Next week, the Eurozone will release its manufacturing and services PMI for September, while Germany will release its Septenber Ifo business sentiment index.

China

China

Under the impact of the Evergrande fallout and the latest developments in Macau's gaming sector, Hong Kong and China equities markets continued their slide, with the CSI 300 Index down 3.14% for the week, the HSI 4.9% lower, and the Hang Seng Technology Index losing 4.39%. The Southbound Bond Connect will be launched on 24 September with an annual quota of RMB500 billion and a daily quota of RMB20 billion. Evergrande's debt crisis intensifies as it is reported that China's Ministry of Housing and Construction informed relevant banks that Evergrande would not pay the upcoming interest due. S&P has also downgraded its rating to 'CC' with a negative outlook. Evergrande still has US$669 million in interest on its bonds outstanding this year. The regulatory action have reached the gaming industry in Macau, causing a sharp fall in all gambling stocks, the market is still assessing the impact of the policies on the industry. Next week, China will announce the latest Loan Prime Rate (LPR).