Weekly Insight May 13

US

US

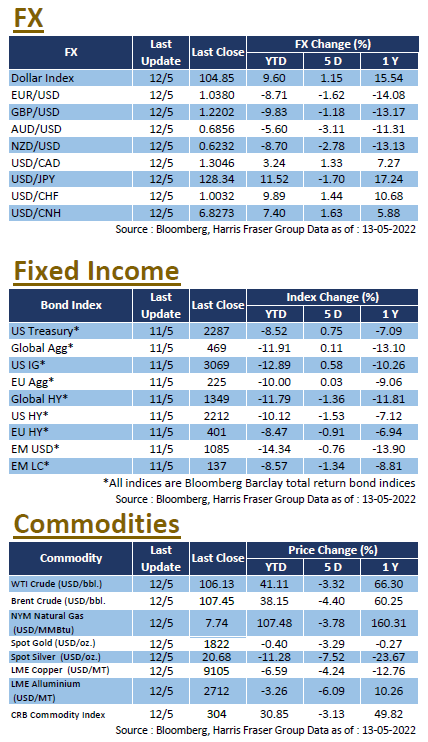

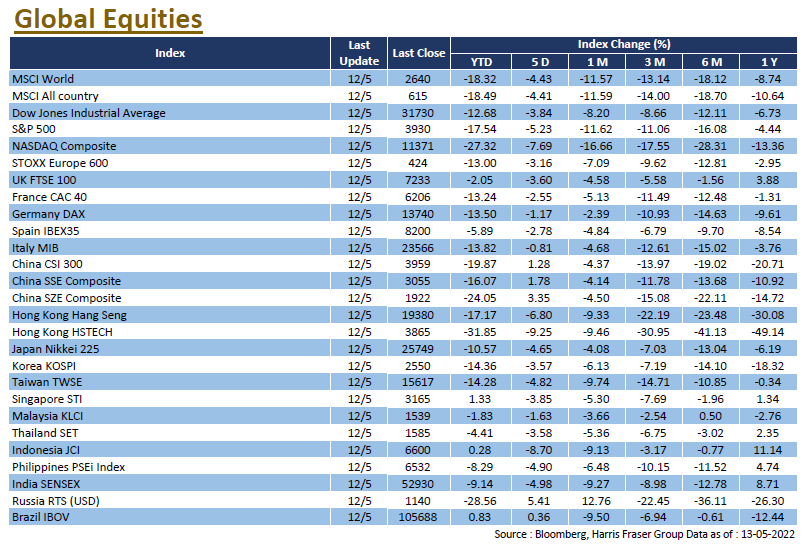

As US inflation remains high and the market is concerned about further tightening by the Federal Reserve, US stocks have continued the slide, with technology stocks posting greater losses; the Dow and S&P 500 fell 3.84% and 5.23% over the past five days ending Thursday, while the tech heavy NASDAQ was down 7.69%. The US Consumer Price Index (CPI) rose by a higher than expected 8.3% YoY in April, with Biden calling inflation too high, and blamed it on the epidemic and the Russo-Ukrainian war. The Atlanta Fed President said he would support more action on interest rates if inflation remained high, while former New York Fed President Willliam Dudley even suggested the Fed should raise rates to 5% or higher.

Later, Fed Chairman Jerome Powell, who has just been confirmed for a second term by the US Senate, reiterated that he would raise interest rates by 50 basis points at each of the next two policy meetings, but added that he might be prepared to take more action if the data moved in the wrong direction. Earlier, in its semi-annual Financial Stability Report, the Fed noted that liquidity conditions in major financial markets are now showing signs of deterioration due to increased risks from the Russo-Ukrainian war, monetary tightening, and high inflation. Next week, the US will release data on retail sales in April and the leading index for May.

Europe

Europe

European stocks followed the US markets lower, but the decline was more moderate due to the lower share of tech stocks. In the past five days ending Thursday, the UK, French, and German indices were down between 1.17% and 3.60%. The European region is facing inflation and tightening issues, with Bank of England deputy governor Dave Ramsden saying that the inflation crisis may take longer to fully resolve and that the central bank must raise interest rates further to deal with the problem. Deutsche Bundesbank President Joachim Nagel also said he would support the ECB's first rate hike in years in the July meeting, if the inflation outlook for next month remains high. Next week, the Eurozone will release its consumer confidence index for May.

China

China

The Hong Kong and Chinese stock markets had a relatively stable week, with the CSI 300 Index rising 2.04% over the week, while the Hang Seng Index also outperformed external markets over the same period. On the economic front, China's Consumer Price Index (CPI) rose by 2.1% YoY in April to a five-month high, while the Industrial Producer Price Index (PPI) rose by 8.0% over the same period, easing from its previous value. On the other hand, the Hong Kong dollar hit the lower bound of the currency peg, before the HKMA bought another HK$2.847 billion from the market on Friday, for a total of HK$6.947 billion over two days. Next week, China will release key data on fixed investment, industrial production, and retail sales for April.