Weekly Insight May 20

US

US

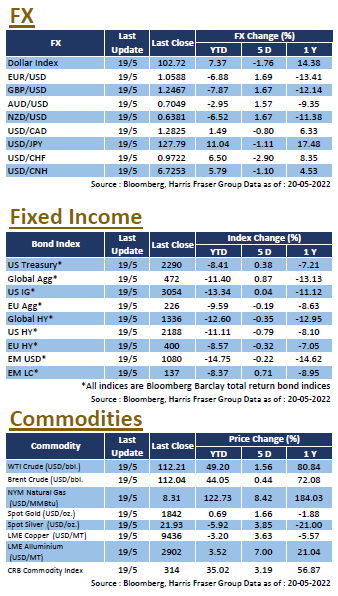

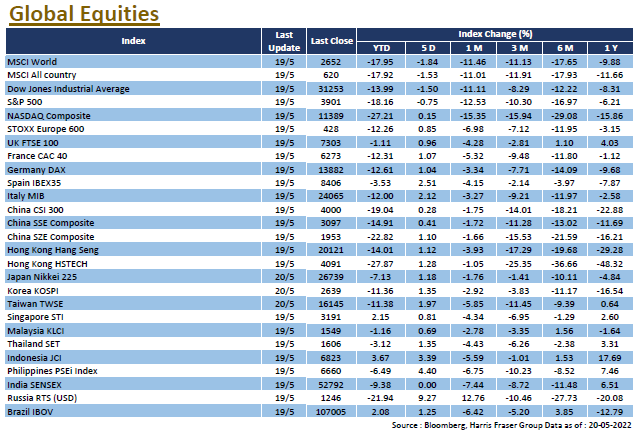

The high inflation in the US has triggered fears of tighter monetary policy and recession, with the S&P 500 index posting its biggest single-day loss in two years on Wednesday and the NASDAQ also fell more than 5% on the same day. Fed Chairman Jerome Powell said he would not hesitate to raise interest rates above the neutral level if needed for curbing high inflation. James Bullard, the most hawkish official in the Fed, avoided the topic on a 75 basis point hike, saying that a 50 basis point hike was a good idea. On the inflation target, US Treasurer Yellen refuted the idea that the Fed should raise its 2% inflation target, stating that stabilising price expectations is of paramount importance.

On the economic front, US retail sales rose by 0.9% MoM in April, slowing from a revised 1.4% in the previous month and slightly below market expectations of 1.0%. The number of initial jobless claims rose unexpectedly to a record high of 218,000 since January, suggesting that labour market conditions remain unsatisfactory. In addition, the US Leading Index fell by 0.3% MoM in April, lower than both the previous month’s 0.3% rise and market expectations of a flat reading. Strategists at major Wall Street firms such as Goldman Sachs and JP Morgan believe that fears of a US recession are premature, although some expect this to be the beginning of the correction in global risk assets. Next week, the US will release data on manufacturing PMI and core PCE, and the Fed will also release minutes of its May meeting.

Europe

Europe

European stocks followed the decline in the US market, with UK, German and French stocks falling by 1.56%, 1.41% and 1.04% respectively in the five days to Thursday. The minutes of last month's ECB interest rate meeting revealed that some officials felt that the current accommodative monetary policy stance was no longer consistent with the region's inflation outlook. Officials expressed general concern about the prolonged inflation and supported the process of policy normalisation. ECB Governing Council member Madis Muller said he would support a 25 basis point increase in interest rates in July. Next week, the Eurozone will release its manufacturing PMI for May and Germany will release its IFO economic confidence index for May.

China

China

The People's Bank of China announced a 15 bps cut in the 5 year Loan Prime Rate (LPR), the largest single cut since the LPR reform, which lifted both Hong Kong and Chinese equities, with the CSI 300 Index rising 1.95% on Friday, ending the week with a 2.23% gain, and the Shanghai Composite Index regaining its 3,100 level. The Hang Seng Index rose by nearly 600 points on Friday, extending the week's gain to 4.11%. Premier Li Keqiang said that policies already in place should be implemented as soon as possible to ensure that the economy stays within a reasonable range in the first half of the year as well as the full year. Vice Premier Liu He also expressed his support for the platform economy and enterprises, supporting the performance of related technology stocks in the short term. Next week, China will release the industrial profits data for April.