Weekly Insight June 11

US

US

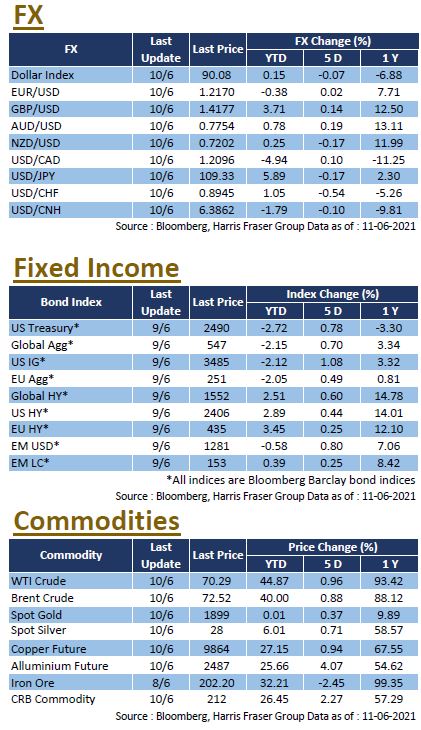

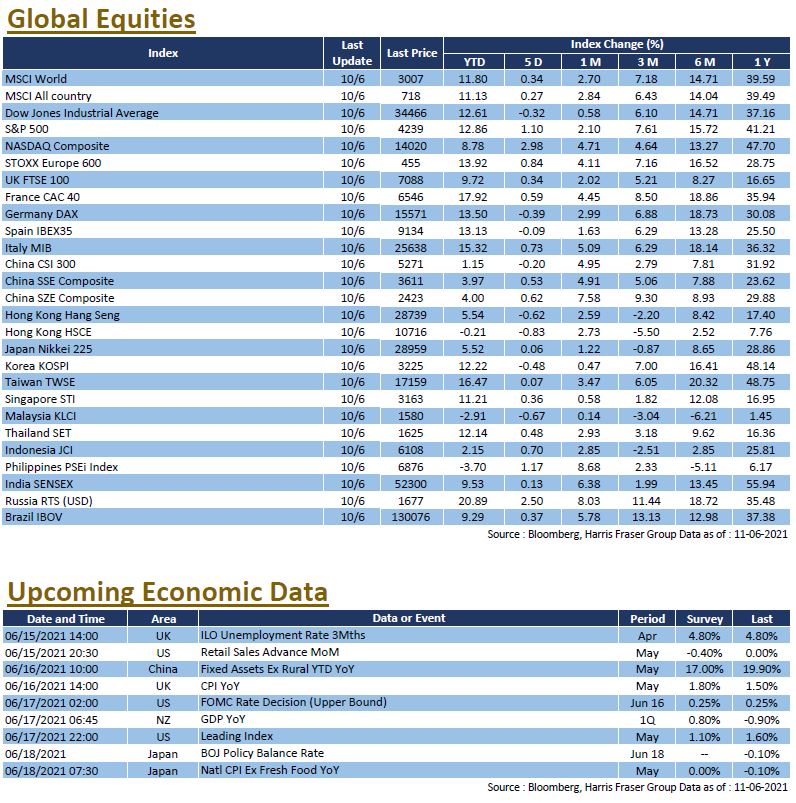

While the economic data doesn’t seem to be too supportive of the market, statements from Fed officials continued to reassure the market, market participants reacted positively. The tech sector in particular bounced further, the NASDAQ index gained 2.98% over the past 5 days ending Thursday, and the S&P 500 index was up 1.10% over the same period, while the Dow was down by 0.32%. The latest CPI figure released on Thursday came in as 5% YoY, which was one of the largest figures in recent years, and exceeded both market expectations and the previous figure. Even if we disregard peripheral data, core CPI was still up by 3.8% YoY, which was the largest figure since 1992.

As the economy is still in the early stages of economy reopening, market expects the Fed to reiterate that the current spike as merely a transitory phenomenon, and any signs of change in monetary policy is expected to be revealed at the Jackson Hole meeting in August. Believing that the risk of a short term monetary tightening has decreased, bond yields flattened on Thursday, while rate sensitive growth stocks rebounded. Next week, the US will release figures on retail sales, while the Fed will also hold an interest rate meeting. Market expects the Fed to maintain the transitory inflation rhetoric unchanged.

Europe

Europe

European markets were softer over the week with the mixed economic data released over the week. Over the past 5 days ending Thursday, the UK and French equity indexes gained 0.34% and 0.59%, while the German DAX lost 0.39%. Fundamentally, 2021 Q1 GDP for the Eurozone was slightly better than market expectations yet remained in contraction, while industrial production figures missed market expectations, as well as the ZEW economic sentiment. On the monetary side, European Central Bank (ECB) President Christine Lagarde rejected the notion that the European inflation could be sustained, stating that inflation is expected to stay below the longer term target over the projection, downplaying the possibility of an early tapering coming from the ECB. The Bank also revised the GDP projections for the Eurozone up to 4.6% in 2021 and 4.7% in 2022. Next week, the UK will release their unemployment figures and CPI data, Eurozone countries will also release their final CPI figures for May.

China

China

Chinese equity markets slightly faltered over the week, tightening liquidity conditions continued to pose as an obstacle to equity performance. The CSI 300 and Shanghai composite were both down again over the week, the Hong Kong HSI also underperformed, falling 0.26% over the week. The latest CPI figures in China were lower than market expectations, the mild figure was reassuring for markets, but the spike in PPI to 9.0% YoY is the highest number since 2008. The latest total aggregate financing figure fell short of market expectations, but still gained MoM, reflecting the liquidity in the onshore market. Next week, China will release figures for fixed assets investment, retail sales, and industrial production.