Weekly Insight March 12

US

US

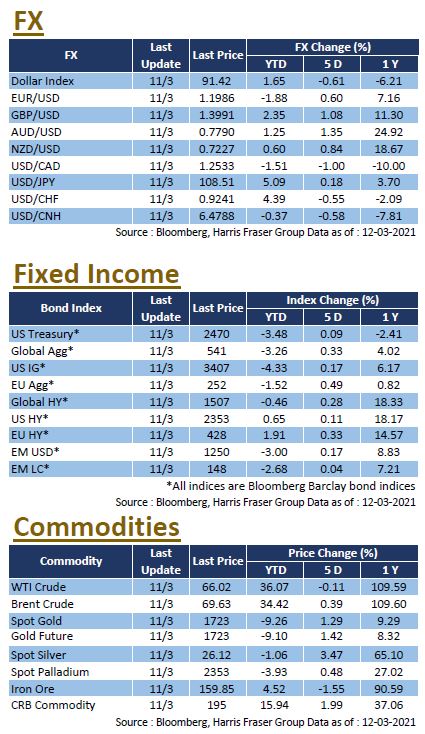

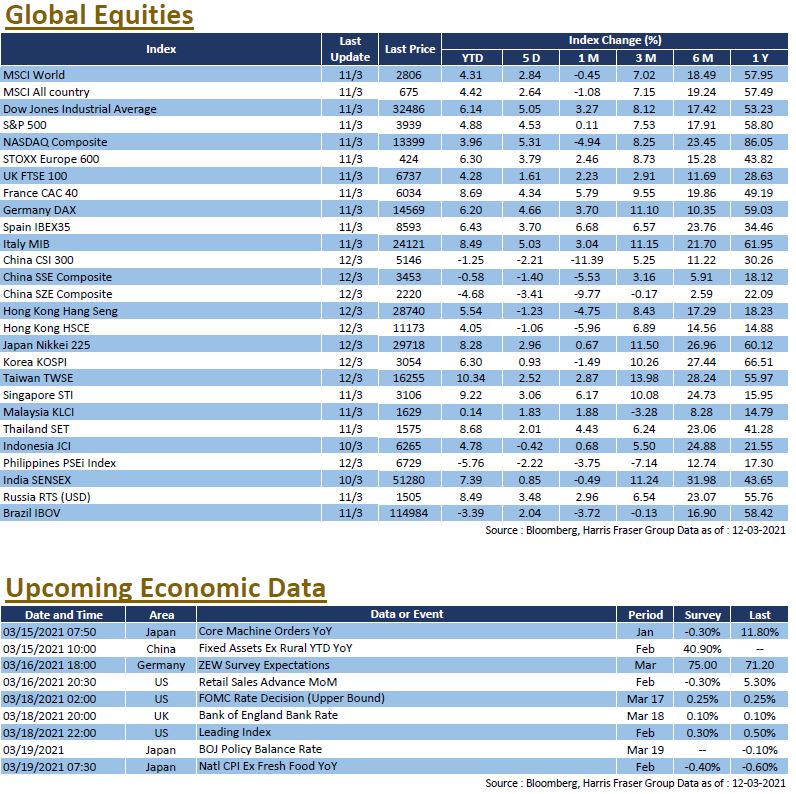

US President Joe Biden signed the US$1.9 trillion stimulus bill on Thursday, pushing the S&P 500 to a new record high in the footsteps of the Dow, and fund flows lifted technology stocks higher, as the three major equity indexes rose between 4.53% and 5.31% over the past 5 days ending Thursday. Earlier, the OECD forecasted that the global economic output would grow by 5.6% YoY, with the US growth rate doubling from the previous forecast to 6.5%. Indeed, recent economic data is encouraging, with the number of initial jobless claims in the US at its lowest level since November 2020, while the core CPI rose at a lower YoY and MoM rate than expected in February, easing concerns about faster inflation and sending US stocks further up after the stimulus package was passed by Congress. Next week, retail sales data and the Conference Board Leading Economic Index will be released, and the Fed will hold the March interest rate meeting, where policy rates are expected to remain unchanged.

Europe

Europe

Stocks in the UK, France, and Germany rose further as the ECB pledged to accelerate asset purchases, which sent the three major European Indexes up between 1.29% and 3.65% over the past 5 days ending Thursday. The ECB announced that it would keep its main refinancing rate unchanged at zero and the overall size of the PEPP unchanged at €1.85 trillion, but pledged to accelerate the pace of bond purchases in the coming months to curb the rise in bond yields, which was positive for market sentiment. In addition, the ECB expects Eurozone GDP to grow by 4% this year, which is higher than the forecast made in December last year, and expects the average inflation rate to rise to 1.5% this year, which is also higher than earlier estimates. Next week, the Bank of England will hold a meeting on interest rates, while Germany will release its ZEW survey expectations.

China

China

China's national ‘Two sessions’ concluded with Premier Li Keqiang announcing that the growth target for this year was set at over 6%, with the intention of avoiding major swings in the economy. Despite a rebound in the market during the last two days of the National People's Congress, the CSI 300 Index fell by 2.9% throughout the two sessions, posting a loss of 2.21% for the week. As the US dollar strengthened, both the onshore and offshore RMB shed their YTD gains. Hong Kong stocks weakened on Friday, dragging the Hang Seng Index down 1.23% for the week, as it was reported that Tencent was facing a widespread regulatory overhaul on fintech and trading in China. The focus of the market was on Baidu, which is in the process of IPO, and BiliBili, which is likely to be the next in line. Next week, China will release a series of data on fixed investment, industrial production, and retail sales.