Weekly Insight October 15

US

US

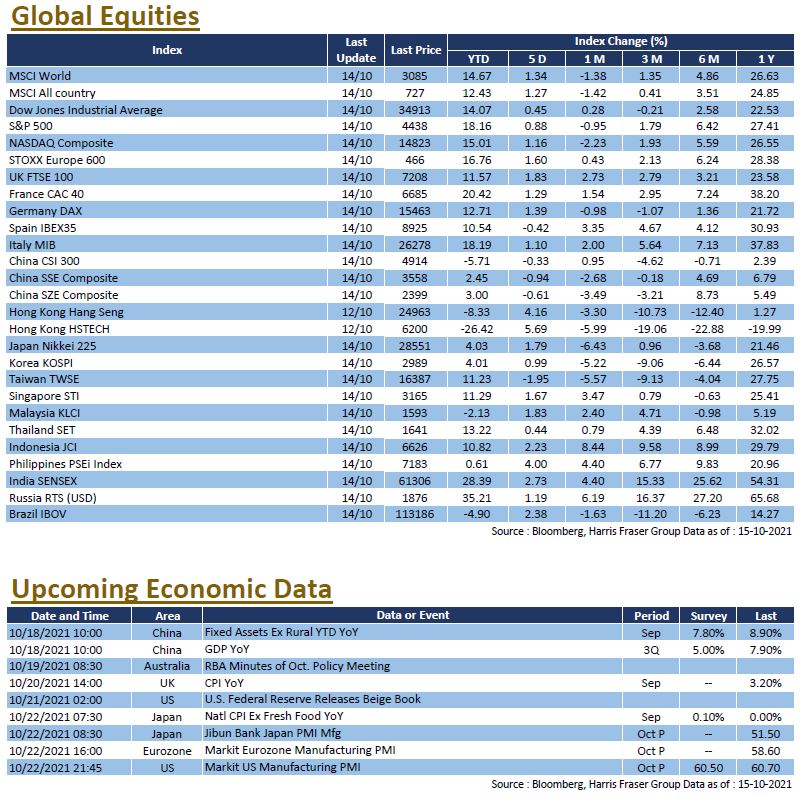

High energy prices continued to raise concerns about rising inflation, but the US financial sector Q3 results were promising, easing fears of an economic slowdown, the three major US stock indices rose 1.56% to 1.73% on Thursday alone, reversing the weakness over the past five days. As the US entered the new earnings season, 77% of the latest 35 S&P companies reported market beats, of which 89% of the 9 financial institutions managed to beat the market.

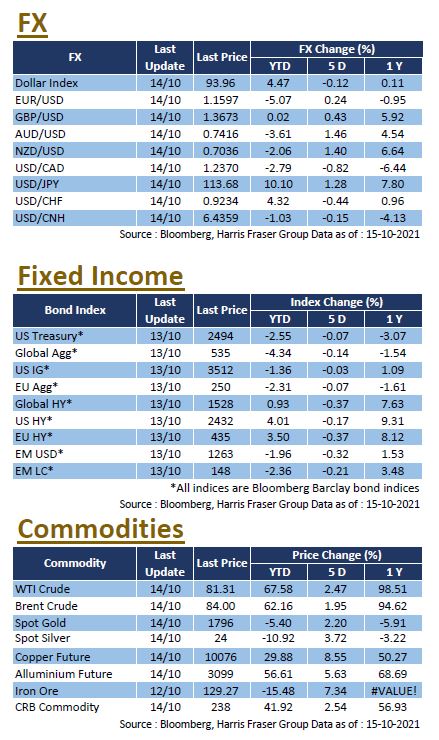

The global energy crisis continued with a surge in energy prices, with WTI futures rising again to US$82.1 per barrel at the time of writing and New York natural gas prices rising again to US$5.77 per MMBtu. In addition to energy, some base metals prices also recovered, with the LME aluminium price rising to US$3,099 per tonne and hitting a 13-year high, the LME metals index also reached a new record high. The Organization of the Petroleum Exporting Countries (OPEC) remained cautious in its oil demand forecasts despite the surge in international oil prices. It has been reported that the US government will meet to discuss how to deal with rising gasoline and natural gas prices.

Against the backdrop of surging energy prices, the US Consumer Price Index rose by 5.4% YoY in September, the highest level since 2008. Amid high inflation, the minutes of the US Federal Reserve's September interest rate meeting indicated that taper of bond purchases was expected to be start in mid-November or mid-December, in line with market expectations. The market will continue to monitor the US financial results, with the latest Fed economic beige book and manufacturing PMI data to be released next week.

Europe

Europe

European stock markets rebounded across the board, with the UK, French, and German indices rising between 1.58% and 1.91% over the past 5 days ending Thursday. The PEPP is scheduled to expire in March 2022, but there are divergent views among ECB officials regarding this issue; Francois Villeroy de Galhau, member of the ECB Governing Council and Governor of the Bank of France, said that the central bank should retain the purchasing flexibility of the PEPP instead of increasing the amount of bonds on a fixed basis. Klaas Knot, another member and President of De Nederlandsche Bank, said that inflation in the Eurozone might be higher than expected in the short to medium term, suggested that the ECB should end the PEPP programme in March next year. Next week, the UK will release the consumer price index, and Eurozone will release the Markit PMIs.

China

China

A-shares were stable while Hong Kong stocks had a strong rebound. The CSI 300 Index was roughly flat for the week. After a two-day trading hiatus due to typhoons and holidays, the Hang Seng Index rebounded 1.48% in a single day and hit a one-month closing high after the market resumed on Friday. Panic in the offshore bond market spreads further as yields on the Bloomberg China Dollar Bond Index rose to 20%, the market is closely watching the latest development. Next week, China will release its Q3 GDP and important data on fixed investment, production and retail sales for September.