Weekly Insight September 2

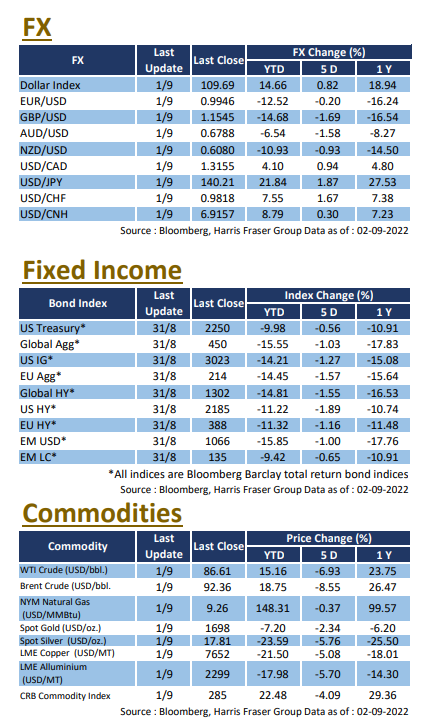

The decline in US stocks continued after the Jackson Hole meeting as the market became more wary of the risk of interest rate hikes, with the three major indices falling between 4.91% and 6.76% over the past 5 days ending Thursday. Neel Kashkari, the Fed's most hawkish official, was "pleased" with the fall in US equities, saying that it reflected the market's recognition of the Fed's resolve to tackle inflation. However, there were widespread concerns over the US economy in the face of expectations of interest rates remaining high. US Senate Republican Leader Mitch McConnell believes that interest rate hikes could lead to a recession and that the Republicans will keep Mr Joe Biden in check. According to UBS, the US credit market has grossly underestimated the risk of recession, with the bank estimating a 55% chance of recession. Morgan Stanley also predicted that the S&P 500 would fall further this year.

Economic data was mixed, with the ISM manufacturing index coming in at 52.8 in August, higher than the expected 51.9; the US ADP Nonfarm employment change was only 132,000 in August, lower than the expected 300,000. Next week, the US will release the ISM Services Index and other data for August, as well as the economic Beige Book.

European equity markets continued the slide this week, with the UK, French, and German equity indices losing 4.32-5.44% over the past 5 days ending Thursday. Over the week, more ECB members commented on the outlook ahead of the monetary meeting on 8th September. ECB board member Isabel Schnabel and Bank of France Governor François Villeroy de Galhau called for larger rate hikes in the coming meeting, Bundesbank President Joachim Nagel also echoed them, arguing that a larger frontloaded hike could help anchor inflation expectations. ECB chief economist Philip Lane however stood behind ‘steady pace’ of rate hikes, so as to allow more adjustments on the fly. European gas prices slightly retreated this week, as the European Commission announced that they are looking at an emergency intervention on the electricity market. On the economic front, Eurozone CPI hit a new record high of 9.1% YoY in August, surpassing the expected 9.0%. Labour market however stays tight, with the unemployment rate in July at 6.6%, remaining at the historic low. Next week, Eurozone retail sales and German factory orders for July will be released, the ECB will also hold the interest rate meeting on 8th September.

China

China

Markets are watching the latest developments at the 20th National Congress of the Chinese Communist Party (CCP) closely, but both China A-shares and Hong Kong equities remain under pressure due to expected rate hikes from the US, with the CSI 300 Index falling by 1.55% and the Hang Seng Index by 2.84% over the past 5 days ending Thursday. At an earlier session of the Central Political Bureau, it was proposed that the 20th National Congress of the CCP should be held on 16th October. A new Central Committee and a Central Disciplinary Committee will be elected at the Congress. The Vice-Chairman of the China Securities Regulatory Commission (CSRC), Mr Fang Xinghai, announces three new initiatives to expand pragmatic cooperation between the Chinese and Hong Kong capital markets, including expanding the range of stocks available through the Stock Connect, supporting the launch of a Renminbi stock trading desk in Hong Kong, and supporting the launch of Chinese government bond futures in Hong Kong. The market will be watching the developments at the G20 meeting and the Fed's rate hikes. Next week, China will release the PPI and CPI for August, as well as the Caixin China Services PMI and export data.