Weekly Insight July 8

US

US

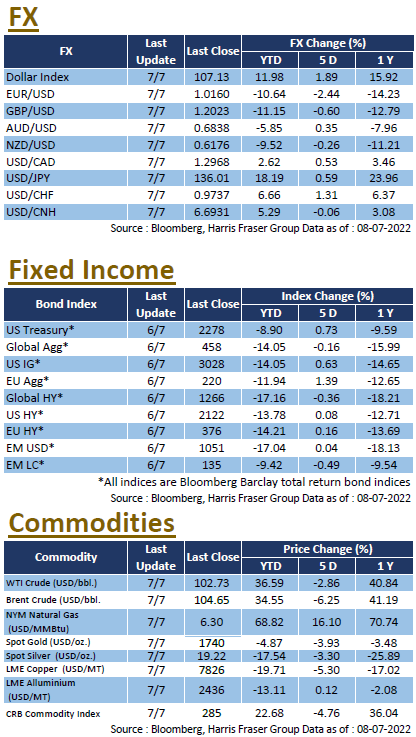

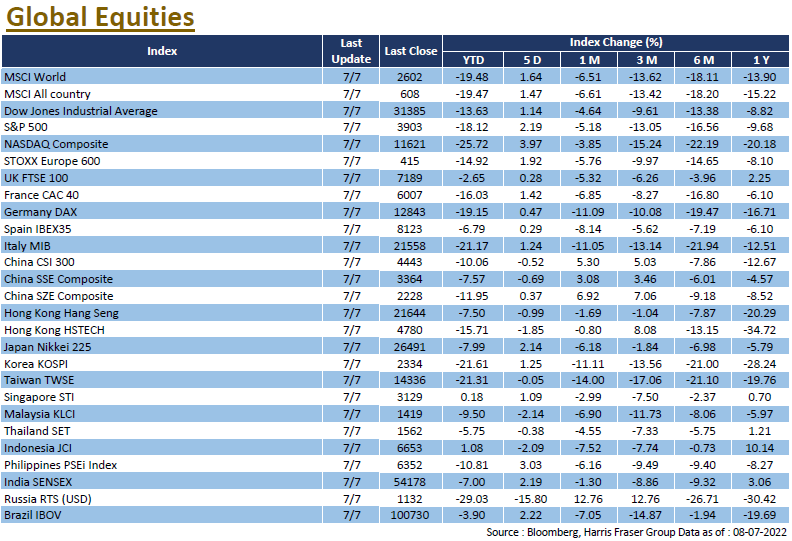

Despite weak economic data and hawkish signals from the Fed minutes, US stocks have managed to rebound over the past few days, with the Dow, S&P and NASDAQ rising between 1.14% and 3.97% in the last five trading days ending Thursday. In the June Fed minutes just released, officials made no mention of a possible recession, instead suggesting that interest rates may be raised to a more restrictive level if inflation remains high. Later, Fed Governor Christopher Waller and St. Louis Fed President James Bullard both expressed support for a 75 basis point rate hike in the July meeting.

While both officials expressed optimism over a soft landing for the US economy, other market participants expressed concerns over the possibility of a recession, for instance Nomura estimates that some major economies will slip into recession in the next year. Economic data was also lacklustre, with the US ISM Services Index falling to 55.3 in June, the lowest level in over two years. Although the number of job openings in the US fell slightly to 11.254 million in May, it remained near record highs, reflecting the tight labour market. Next week, the US will release CPI and retail sales for June, the University of Michigan market sentiment, as well as the Fed Beige Book.

Europe

Europe

European equities edged higher, with UK, French, and German indices rebounding between 0.24% and 1.28% over the past 5 days ending Thursday. The ECB released minutes of its June meeting, which showed that officials were broadly in agreement that a gradual rate hike does not imply slow to act, and it is important to avoid limiting rate actions to 25 basis points. On the other hand, the political scene in the UK is in turmoil again, with more departures following the resignations of senior government officials including the Finance and Health Ministers, with Prime Minister Boris Johnson ultimately announcing his resignation as well. Next week, the Eurozone will release data on industrial production in May and the ZEW economic forecast for July.

China

China

The COVID situation in China was mixed, with the Yangtze Delta region being affected, including the spread of the mutated strain in Shanghai. The A-share market had soft week, with the CSI 300 index down 0.85%; Hong Kong equities were also down, with the Hang Seng index 0.61% lower over the week. Chinese Premier Li Keqiang said the economic recovery was not yet solid and urged regional governments to implement more policies to support the economy. In addition, the mainland government is considering advancing the issuance of some local special bonds amounting to RMB1.5 trillion to boost the economy. Next week, China will announce its Q2 GDP, fixed investment and exports figures for June.