Weekly Insight July 15

US

US

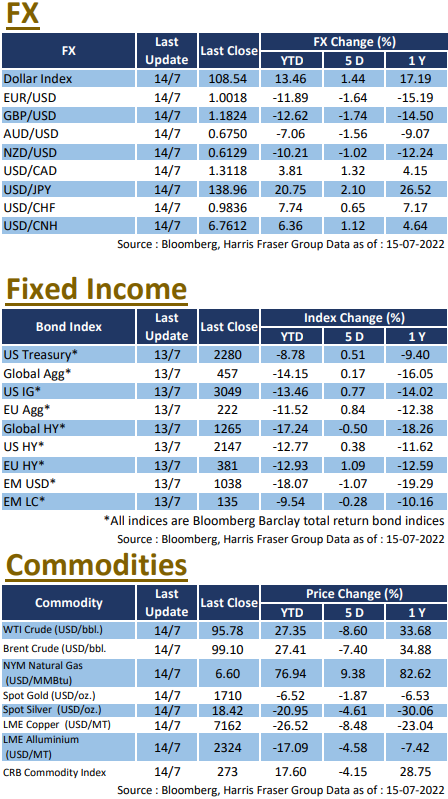

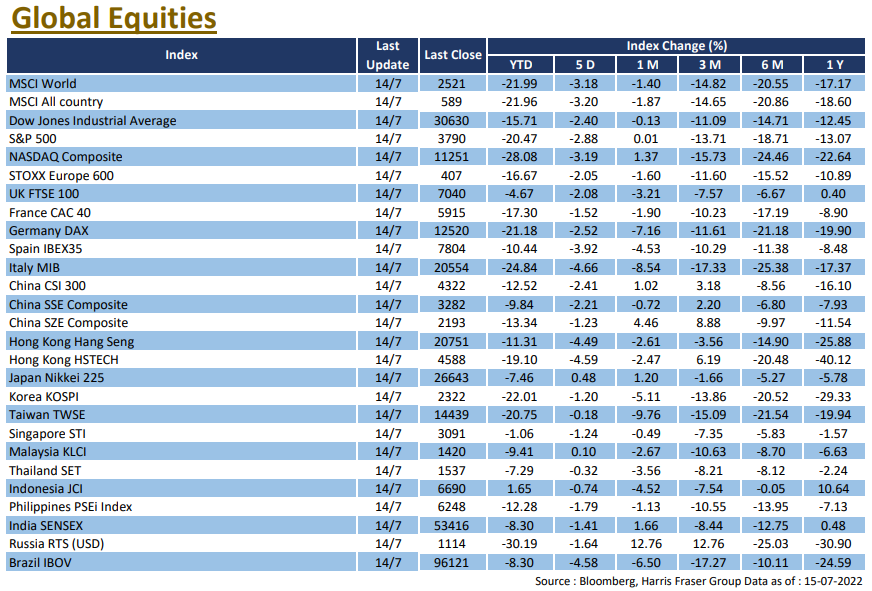

A further rise in US inflation to its highest level in more than 40 years sparked fears of a straightforward 1% interest rate hike in July, and together with the International Monetary Fund's lowered forecast for economic growth, market sentiment took a hit, with the three major US stock indices falling by 2.40% to 3.19% in the past five days to Thursday. The US Consumer Price Index (CPI) rose 9.1% year-on-year in June, a further record high since 1981 and above market expectations. US President Joe Biden said that the inflation report was out of date and did not adequately reflect the decline in gasoline prices. Nevertheless, the market raised expectations for a 100 basis point rate hike in July and the President of the Atlanta Fed hinted that a 1% rate hike in July was not out of the question. This was followed by the worst inversion in the spread between 2-year and 10-year US bond yields since 2000, suggesting that a recession may be imminent.

Indeed, the International Monetary Fund (IMF) has cut its growth forecast for the US this year and next to 2.3% from 2.9% and 1% next year from 1.7%, with the head of the IMF saying that a global debt crisis is brewing after a wave of interest rate hikes following the epidemic and war. The U.S. Federal Reserve Releases Beige Book showed that price inflation was significant in all jurisdictions, while demand showed signs of slowing and recession fears were rising. In addition, the US is entering a peak earnings period, with quarterly net profits down 28% year-on-year at Morgan Stanley and 28% year-on-year at JP Morgan Chase, and the market is concerned about the performance of US stocks this quarter. The US manufacturing PMI for July will be released.

Europe

Europe

The euro has fallen to 1:1 against the dollar for the first time in 20 years, but this has not helped European stocks to rally, with inflationary pressures leading to concerns about growth, with UK, French and German stocks down between 1.95% and 3.81% in the last five days to Thursday. In the face of the euro's decline, the ECB said it needed to be concerned about the impact of the exchange rate on imported inflation. In addition, the EU cut its economic growth forecast for the eurozone next year to 1.4%, while expecting the impact of inflation to last longer. Italian Prime Minister Mario Draghi said he would not continue to lead the government if the Five Star Movement left the ruling coalition. The Eurozone will release manufacturing PMI, the UK will release CPI and other data, and the ECB will meet in July.

China

China

Chinese equities continued the weakness seen since July, with the CSI 300 index down 4.07% and the Hang Seng index down 6.57% for the week. China's GDP fell 2.6% sequentially and narrowed to 0.4% year-on-year in the second quarter of the year due to the impact of the epidemic. Aggregate financing rose, to RMB5.17 trillion in June, while the amount of new RMB loans rose to RMB2.81 trillion over the same period. Premier Li Keqiang said the economy has stabilized and rebounded, but a new round of epidemic prevention and control may have a greater impact and consumption may recover more slowly in the second half of the year. China will announce 1-year and 5-year LPR rates.